The limits of diversification: oil, inflation and cross-asset correlations

Author

Christoph Schon

Head of Investment Decision Research, EMEA

Oil prices surged after Middle East tensions escalated, pushing inflation expectations higher, especially in Europe. Markets have largely priced out Fed rate cuts for 2026, boosting the dollar, while ECB tightening hasn't helped the euro. With stocks, bonds and currencies moving together, gold offered little safe-haven relief with oil the only asset that reduced portfolio risk.

H1 2026 MAC Review: Risk & Performance

Thanks to its inverse relationship with equities and bonds and its negligible correlation with currencies [oil] has been the only holding to actively reduce total portfolio risk.

The first half of 2026 was dominated by the conflict in the Middle East and its impact on global energy supplies and prices. As in previous energy-driven shocks, the rise in oil prices fed through into inflation expectations, which in turn drove an upward revision in monetary policy expectations on both sides of the Atlantic. Rising interest rates sent global bonds and equities into a tailspin in March, while a stronger dollar further amplified foreign losses for USD-based investors. Gold also provided little relief, despite its customary reputation as a safe haven in times of political turmoil and persistent inflation. This co-movement across asset classes and regions severely limited diversification opportunities of multi-asset investors, with oil being the only asset to reduce overall risk thanks to its inverse relationship with most other markets.

Here are the key cross-asset dynamics we tracked. The full set of corresponding slides is available to download below.

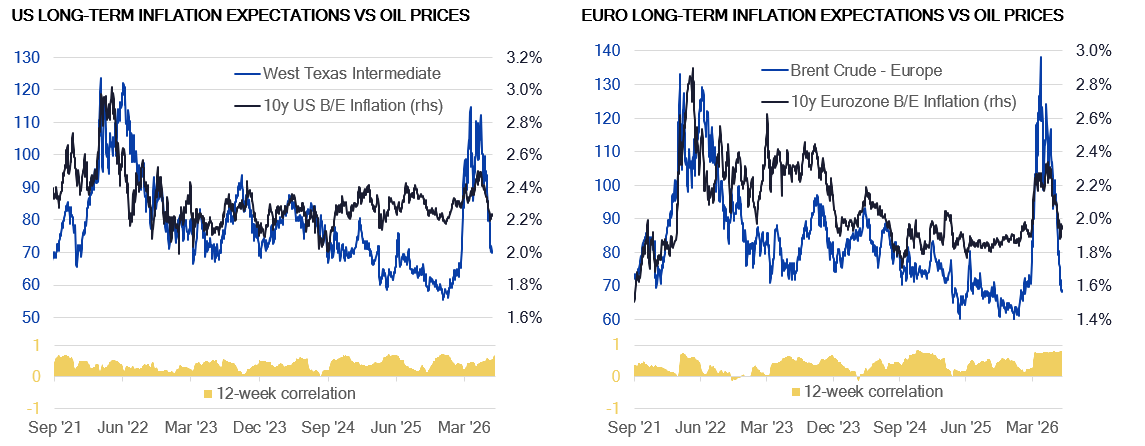

Oil prices and inflation expectations

Soaring oil prices translated into higher inflation expectations, especially in Europe, albeit to a lesser extent than in 2022.

Oil prices are strongly positively correlated with long-term breakeven inflation rate, even though the latter are based on core prices, which exclude energy and food costs. This indicates that markets are incorporating second-order effects from higher energy costs on the wider economy. Like in the wake of the Russian invasion of Ukraine in 2022, breakeven rates immediately started to rise after tensions erupted in the Middle East, although the increase was much more subdued this time. This indicates that investors expected a swifter end to the current conflict than four years ago. It is also worth noting that inflation expectations rose more in Europe than in the US in acknowledgement of the bigger impact the supply disruptions had on the former continent.

Chart 1: Soaring oil prices

Sources: U.S. Energy Information Administration via FRED®, SimCorp

Impact of inflation expectations on (real) yields

Nominal yields rise and fall with inflation expectations, except for times when flight to quality dominates.

Nominal and breakeven rates typically move in lockstep, as the latter are by definition the inflation component embedded within the former. But there are exceptions when the relationship can flip. For example, at the onset of the Ukraine war, flight to quality briefly depressed sovereign yields –even back into negative territory in Europe – despite a surge in inflation expectations. When the Fed aggressively tightened monetary conditions in the summer of 2022, US breakeven rates eased back toward 2 percent, while 10-year Treasury yields soared to 4 percent.

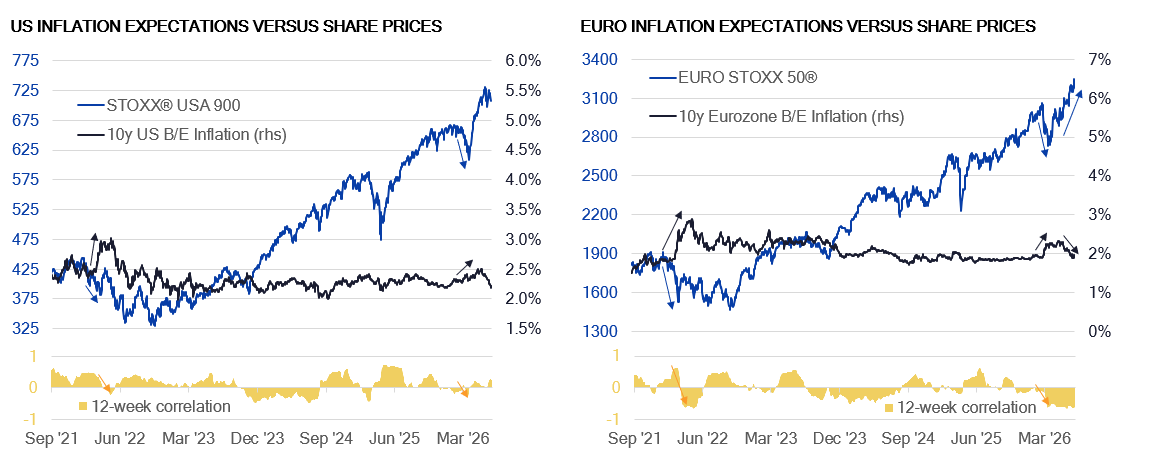

Impact of inflation expectations on share prices

Share prices tend to be positively correlated with inflation expectations most of the time, but the relationship can flip if inflation rises sharply.

After the price and rate shocks of 2022, investors may be excused for believing that higher inflation expectations are always bad for stock markets, but in reality, the relationship between the two time series is predominantly positive. That makes sense, as both are driven by the same underlying force: economic growth expectations. When the economy is doing well, firms are in a better position to raise prices and share prices rise. When economic activity is slowing down, both tend to fall together. It is only when inflation expectations rise sharply, as they did in early 2022 or March 2026, that stock markets drop as a result. The opposite dynamic also worked when inflation cooled down and equities recovered over the course of 2024.

Chart 2: Impact of inflation expectations on share prices

Sources: ISS STOXX, SimCorp

Fed monetary policy expectations and the dollar

Federal Reserve is no longer expected to cut rates this year, strengthening the dollar.

Until the end of February, markets expected the Federal Reserve to continue to ease monetary conditions by another 75 basis points over the course of this year. These cuts are not completely priced out, with federal funds futures assigning more than 80 percent probability of at least one rate hike, which could happen as early as the September 16 Federal Open Market Committee (FOMC) meeting.

The dollar has been one of the biggest beneficiaries of higher interest rates, due to its strong positive correlation with US monetary policy expectations, which has been dominating FX markets since the Fed’s first (of four) ‘jumbo’ rate hike of 75 basis points in June 2022. The only brief interruption of the relationship happened after the introduction of tariffs at the start of 2025, which triggered a capital flight from the United States while rates markets priced in tighter monetary policy in response to rising inflation expectations.

ECB monetary policy expectations and the euro

Euro appears to exhibit inverse interaction with ECB rate expectations, as relationship is driven by USD leg and Fed policy.

The European Central Bank was ahead of the Fed and was expected to have finished easing monetary policy. Following the surge in oil prices and inflation expectations, short-term interest rate markets initially anticipated up to a full percentage point of tightening, but later reduced its projection to 50 basis points. The ECB already raised its policy rates by 25 basis points at its June meeting, leaving one more hike over the remainder of the year. Unlike for the dollar, higher rates did not benefit the euro. On the contrary, the correlation was negative most of the time, though not because of any euro-specific issues, but because the relationship was almost exclusively driven by the dollar leg and Fed policy expectations.

The impact of monetary policy on share prices

Monetary policy impact on share prices depends on whether it is driven by inflation or economic concerns.

The impact of monetary policy on the stock market is less deterministic than for currencies and depends a lot on the context, in which the central bank makes its decision. A central bank that gradually raises rates in an expanding economy to prevent it from overheating is different from a central bank that aggressively tightens monetary conditions to rein in soaring consumer prices. The same is true for monetary easing. If the central bank lowers rates to engineer a ‘soft landing’, the impact on stock markets may be very different from a central bank that floods an economy and financial markets with cheap cash to prevent a meltdown.

When inflation and monetary policy expectations rose in 2022, share prices took a tumble, and the correlation between the stock market and interest rate futures – whose prices move in the opposite direction of rates – turned positive. The relationship briefly inverted again after the default of Silicon Valley Bank triggered concerns over the stability of the US banking system, but fears were quickly averted, and the focus returned to inflation and monetary policy. The weaker-than-expected labor market reports in the summer of 2024 and the introduction of the 2025 tariffs again led to a temporary inversion, but the relationship turned positive again at the onset of the Iran conflict. This indicates that markets are predominantly focused on the inflationary impact the current crisis will have.

Multi-asset class portfolio risk analysis

Investor focus on inflation and monetary policy turns cross-asset correlations positive, limiting diversification opportunities.

The current focus on inflation and monetary policy means that cross-asset correlations are predominantly positive. Stocks and bonds sell off together when inflation and interest rates rise and recover together when they ease again. The dollar strengthening and weakening with rising and falling rates further amplifies foreign gains and losses for USD-based investors, creating additional volatility and leaving little opportunity for diversification across both asset classes and regions.

The last time stocks and bonds moved in opposite directions was in April 2025, when the “Liberation Day” tariffs triggered brief flight to quality and downward revision in monetary policy expectations.

Portfolio volatility contributions as of June 26, 2026

Soaring oil prices partly offset losses in all other asset classes

The positive correlation across most asset classes and risk factors meant that the majority of securities in the portfolio added to overall predicted volatility. The only exception was oil, which due to its inverse relationship with stock and bond prices and its zero correlation with FX rates actively reduced overall portfolio risk. Gold prices, on the other hand, were positively correlated with both the stock market and exchange rates against the US dollar, making the precious metal the riskiest asset relative to its monetary weight.

Key takeaways and outlook

The Middle East conflict and the resulting surge in oil prices have pushed inflation and monetary policy back to the top of investors' minds, and that shift has materially narrowed the diversification available across a multi-asset portfolio. With stocks, bonds, and the FX rates against the dollar now all reacting to the same inflation narrative, they have moved to sell off together when rate expectations rise and recover together when they ease, rather than offsetting one another as they typically would in a situation of geopolitical turmoil.

The one consistent exception has been oil itself, which – thanks to its inverse relationship with equities and bonds and its negligible correlation with currencies – has been the only holding to actively reduce total portfolio risk. Gold, on the other hand, has instead added to overall volatility – despite its reputation as a safe haven – through its positive correlation with both equities and inverse relationship with the dollar. Until the conflict is resolved and the current inflation focus fades, cross-asset correlations are likely to remain strong and positive, leaving portfolios more exposed to a single shared risk factor and less able to rely on diversification across asset classes and regions to cushion losses.

FAQs

FAQs

Is gold still a good inflation hedge?

It depends on the context. Despite its safe-haven reputation, gold moved in step with both equities and FX rates against the dollar in H1 2026, which meant it added to overall portfolio volatility instead of offsetting it.

FAQs

Why did oil reduce portfolio risk when other assets didn't?

Oil's inverse relationship with stocks and bonds, combined with its negligible correlation with currencies meant it moved opposite to the rest of the portfolio.

FAQs

What is the difference between nominal and real bond yields?

Nominal yields are the rates quoted on a bond; real, or breakeven, yields strip out the market's inflation expectations. The two typically move together, since breakeven rates are the inflation component embedded in nominal yields although the relationship can flip during a flight to quality.

FAQs

How does Fed policy affect the US dollar?

The dollar tends to strengthen when markets expect the Fed to raise rates, or to ease by less than previously priced in, since higher US rates attract foreign capital. That relationship has dominated FX markets since the Fed's first jumbo hike in June 2022.