.png%3Fh%3D1200%26iar%3D0%26w%3D550&w=3840&q=75)

.png%3Fh%3D1080%26iar%3D0%26w%3D1920&w=3840&q=75)

Multiple risk models, one best practice – for all managers

Author

Diana R. Baechle, Ph.D.

Senior Principal Investment Decision Research, SimCorp

A single risk model is rarely enough. Drawing on a global active portfolio, we examine how four models (fundamental and statistical, short and medium horizon) each tell a different part of the same story and why using them together represents best practice for fundamental and quantitative managers alike.

A case study in four risk models and the case for never relying on just one.

Risk management has moved to the center of the portfolio management process. Heightened market volatility, faster information flow, and tighter risk constraints have made it increasingly important for investment managers to understand not just how much risk they are taking, but where that risk is coming from and how quickly it is changing.

Relying on a single risk model can provide an incomplete and potentially misleading picture. Instead, the disciplined use of multiple factor risk models, spanning both fundamental and statistical approaches and incorporating different forecast horizons, offers differing perspectives when conditions are uncertain. This approach can deliver a more comprehensive insight into the drivers of portfolio volatility, enable faster recognition of regime shifts and strengthen confidence in portfolio decision-making.

Case study: a global active fund through multiple risk lenses

In this case study, we analyze a large well-known global actively managed portfolio which used a fundamentally driven investment process benchmarked to the FTSE All World.1 This is a useful example of how multi-model risk analysis can benefit managers who are not explicitly quantitative, although the benefits outlined below extend to both fundamental and quantitative managers.

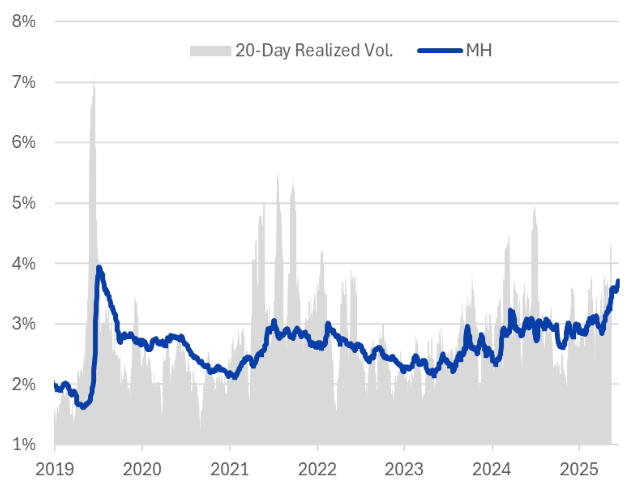

Figure 1 illustrates a time-series chart of predicted active risk and the realized forward 20-day rolling tracking error, using our test fund and the Axioma Worldwide (WW5.1) medium-horizon fundamental factor risk model — what the user of a single model might see.

During the period under observation (2020-2026), predicted risk levels changed rapidly and often dramatically, particularly during the 2020 Covid Crisis and most recent geopolitical crisis triggered by the escalation in Iran. The medium-horizon model tracks the ebbs and flows of the 20-day forward looking volatility, but the magnitude of the changes in risk is much lower.

Figure 1. Predicted Active Risk, Fundamental Medium-Horizon Model

Source: Morningstar, FTSE Russell, Axioma Worldwide Equity Factor Risk Model (WW5.1)

Fundamental versus statistical risk models

Another frequent debate centers on whether fundamental or statistical models are more accurate. In practice, the question is not which model is superior, but how each contributes to a more complete understanding of risk. Fundamental models offer a transparent and intuitive framework for decomposing risk into economically meaningful factors such as industries, styles, and countries. They are well suited for portfolio construction, risk budgeting, and performance attribution, and they generally perform well in forecasting risk under normal market conditions.

Statistical models, by contrast, do not impose predefined factor structures. Instead, factors emerge directly from the data. This flexibility allows statistical models to capture short-term or transitory sources of risk that may not be represented in a fundamental framework. As a result, statistical models often provide unbiased estimates of total risk, particularly during periods of market stress. Their main limitation is interpretability: because the factors are not explicitly defined, it can be difficult to explain what is driving changes in risk or to use the results for attribution.

Used together, these two approaches are highly complementary. Fundamental models help managers understand and communicate risk in intuitive terms, while statistical models serve as an important validation tool, signaling whether overall risk levels are consistent with expectations or whether something unusual may be occurring beneath the surface.

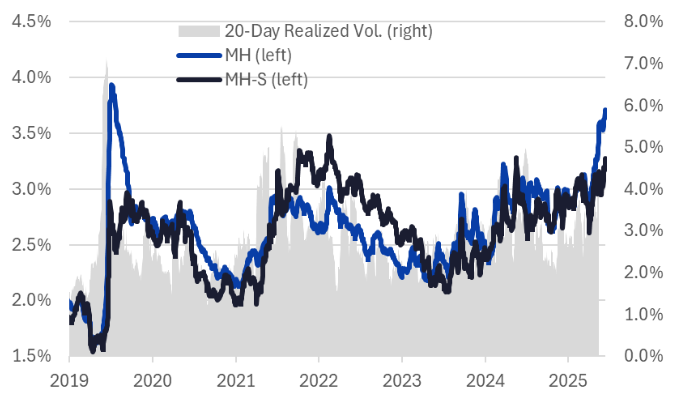

Let’s review our case study portfolio from the perspective of one additional risk model and consider how our assessment of risk levels might change if the statistical model were included in the analysis.

As shown in Figure 2, during more ‘normal’ market conditions, medium-horizon fundamental and statistical models generate nearly identical active risk estimates. But during crises or major macro regime shifts, the two begin to diverge — precisely when portfolio managers need the richest possible information.

During both the Covid shock and the most recent Middle East crisis, the statistical model failed to capture the sharp rise in risk, as the jump was driven largely by industry, country, and style factors. In these moments, the fundamental model more effectively reflected the surge in risk.

In contrast, the models displayed a prolonged divergence from 2022 through 2023. Throughout this period, the statistical model consistently projected higher risk than the fundamental model — likely a result of the interest rate regime change, when central banks began raising rates for the first time in many years. While higher rates clearly influence certain fundamental factors (for example, the Leverage style factor or Banks industry factor), they also introduce subtler effects, such as investors reallocating from equities into bonds.

Ultimately, relying on a single model during periods of divergence — whether short-lived spikes or prolonged shifts — can leave important signals unseen.

Figure 2. Predicted Active Risk Comparison, Medium-Horizon Fundamental Vs. Statistical

Source: Morningstar, FTSE Russell, Axioma Worldwide Equity Factor Risk Model (WW5.1)

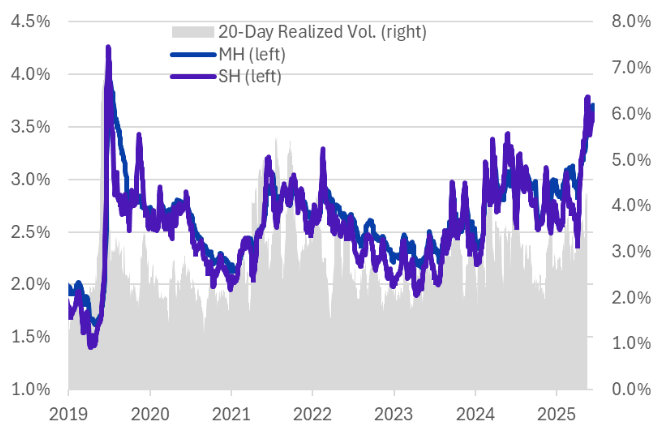

The role of the forecast horizon

The choice of forecast horizon embedded in a risk model is another critical consideration. Short-horizon models, which rely more heavily on recent data, respond quickly to changes in volatility and correlations. They are particularly useful for traders or during periods of market turmoil, when conditions can shift rapidly. Medium-horizon models, which use longer histories, tend to produce smoother estimates and are often preferred by long-term investors who can ride out short-term market disruptions.

However, relying exclusively on a medium-horizon model can be problematic when risk is changing quickly. Such models may lag both on the way up and on the way down, potentially leading to delayed or unnecessary portfolio adjustments. By contrast, short-horizon models may temporarily overstate risk during brief volatility spikes, prompting excessive trading if used in isolation. Viewing both horizons together allows managers to distinguish between transient shocks and more persistent changes in the risk environment.

As illustrated in Figure 3 and 4, the short-horizon versions of the fundamental and statistical models responded much more quickly to the sharp increase in risk in March 2020 and March 2026; in fact, the medium-horizon model never fully caught up.

Similarly, when risk subsided in 2023, the short-horizon model again adjusted more rapidly. A manager using both models may therefore have been able to avoid rebalancing a portfolio that appeared to carry excessive active risk from a medium-horizon perspective, recognizing that the short-horizon model indicated that predicted risk was likely to decline.

Figure 3. Predicted Active Risk Comparison, Medium Vs. Short Horizon, Fundamental

Source: Morningstar, FTSE Russell, Axioma Worldwide Equity Factor Risk Model (WW5.1)

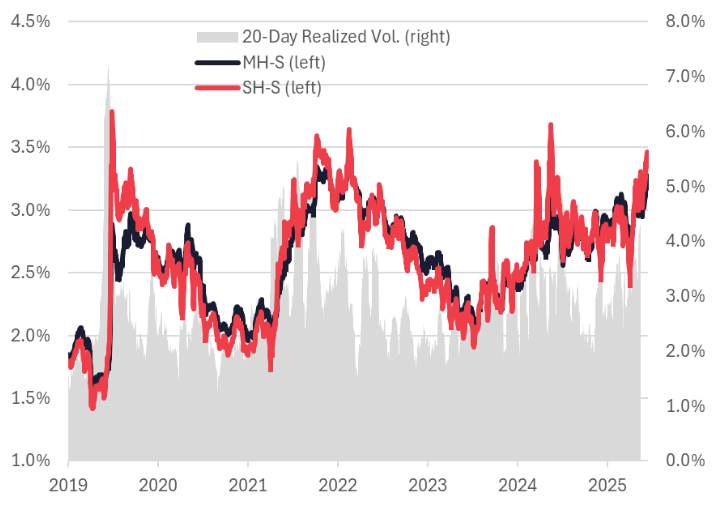

Figure 4. Predicted Active Risk Comparison, Medium Vs. Short Horizon, Statistical

Source: Morningstar, FTSE Russell, Axioma Worldwide Equity Factor Risk Model (WW5.1)

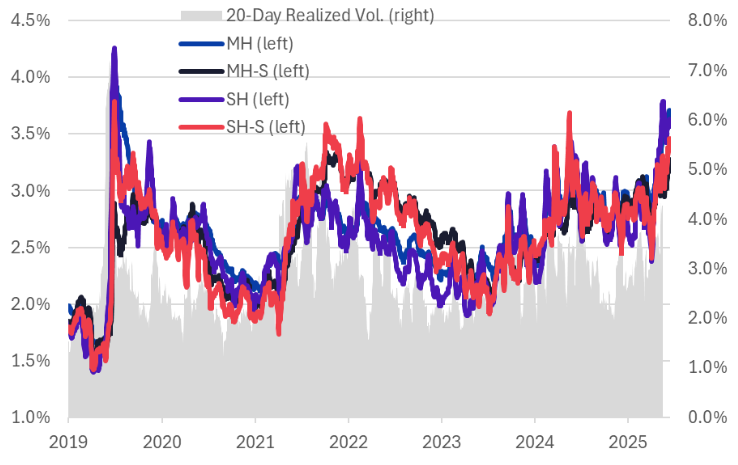

Insights from multiple factor risk models

When we examine the case study portfolio using four different Worldwide risk models —fundamental and statistical, each at short and medium horizons — a more informative picture emerges. During periods of relatively stable volatility, all models produce similar risk estimates. As volatility increases, however, the estimates begin to diverge.

Viewed together in Figure 5, the differing risk forecasts observed during the crisis ultimately converge as market conditions stabilize. Each model provides a distinct perspective, and a manager considering all four would have gained a more comprehensive understanding of the risks being assumed.

In summary, volatility spiked at the beginning of 2020, and the risk estimates across models started to diverge. With the onset of the Iran crisis in 2026, these differences also became more pronounced. The short-horizon models captured the higher volatility better than the medium-horizon models — an expected outcome given their shorter half-lives and greater reliance on recent data. In addition, the statistical models consistently estimated higher levels of risk than their fundamental counterparts during macro-economic regime changes.

Figure 5. Comparison of All Four Models

Source: Morningstar, FTSE Russell, Axioma Worldwide Equity Factor Risk Model (WW5.1)

"Relying on only one type of model means some risks will simply go unseen, particularly during periods of market stress. By contrast, using multiple, consistently constructed models enables earlier detection of risk regime shifts, clearer diagnosis of their sources, and more confident portfolio decisions."

Conclusion: the multi-model approach is not just for quants

This case study demonstrates that effective risk management increasingly requires more than a single model or a single perspective. Fundamental and statistical models each offer distinct insights, and short- and medium-horizon models respond differently to changing market conditions. Together, they form a coherent and robust framework for understanding portfolio risk.

Importantly, these differences are not contradictory; they are signals. A manager observing all four models would have been better positioned to understand both the magnitude and the nature of the risks being taken, and to judge whether observed increases were likely to persist.

For managers who already use an existing risk model, the question is not whether to replace it, but what it may not be telling you. A single model, however well-constructed, will always reflect one set of assumptions. The value of a multi-model approach lies precisely in that diversity of perspective.

Relying on only one type of model means some risks will simply go unseen, particularly during periods of market stress. By contrast, using multiple, consistently constructed models enables earlier detection of risk regime shifts, clearer diagnosis of their sources, and more confident portfolio decisions.

Importantly, these benefits are not limited to quantitative strategies. The ability to understand and manage risk effectively is a universal requirement, and a multi-model approach provides a practical and intuitive path toward that goal.

The Axioma equity risk model suite includes all four model variations used in this analysis as standard. A trading horizon model is also available for managers operating at even shorter time scales. To learn more, contact us.

References/footnotes

1 The analysis is as of March 12, using quarterly portfolio data from September 30, 2019 – December 31, 2025.

Related articles