How long does it take to test dozens of research factors for alpha?

Authors

Jordan Francis, Principal Solutions Engineer

Robert D. Stock PhD, Principal Analytics Researcher

We used Snowflake to screen the Axioma Factor Library for predictive power and demonstrated the speed, ease, and flexibility of processing and analysis possible with the right data and tools.

We did it in one afternoon.

Alpha potential in risk model factors

Identifying which signals drive returns is a painstaking research process, and seasoned quants know how difficult it can be to align the data pipeline with research tools. We aimed to eliminate as much friction as possible by using an alternative, more efficient approach, and found that we could build quant strategies without wasting precious time on mundane data wrangling.

In this piece, using an array of fundamental, technical and macroeconomic factors from the Axioma Factor Library Suite, we demonstrated what's possible when we use a modern data platform. As an alpha-screening exercise, we developed a research engine in Python that computes Information Coefficients (ICs) and Information Ratios (IRs). We then tested 58 library factors already on Snowflake from the Axioma US Equity Factor Risk Model (v5.1) and the Axioma Worldwide Macroeconomic Projection Equity Factor Risk Model (v4), and generated publication-style charts for analysis. Using Snowpark for native processing within Snowflake, the whole exercise – roughly 20 years of daily data for ~3,000 assets – ran in 2–3 minutes per factor on a standard Small warehouse, with no data movement required.

How to screen Axioma factor exposures for alpha in Snowflake

Using the Snowpark library, we opened a Python session directly against the factor exposures and estimation universe returns stored in Snowflake, eliminating the need to extract or move data. For each time T, we computed forward returns at four different horizons, then calculated the cross-sectional Pearson correlation between each factor's exposure and the corresponding forward returns.

Accessing Axioma data such as the Factor Library Suite through Snowflake delivers a powerful mix of high‑quality modeling and scalable compute with the easy, efficient and trusted processing capabilities of Snowflake.

That correlation is the Information Coefficient, a measure of how well the cross-sectional levels of a factor's exposures correlate with the cross-sectional levels of forward returns, indicating the strength of potential alpha. The IR scales the mean IC by its standard deviation and reflects the stability or reliability of the signal over time.

Running this natively in Snowflake via the Snowpark library, rather than pulling data locally, vastly speeds up our research process. With Snowpark, SQL‑style data processing runs directly inside Snowflake, allowing you to leverage its cloud-native performance for efficient, large‑scale analytics that fit naturally into a quantitative workflow.

Earnings Growth, Profit Quality, and macro factors: What the IC analysis shows

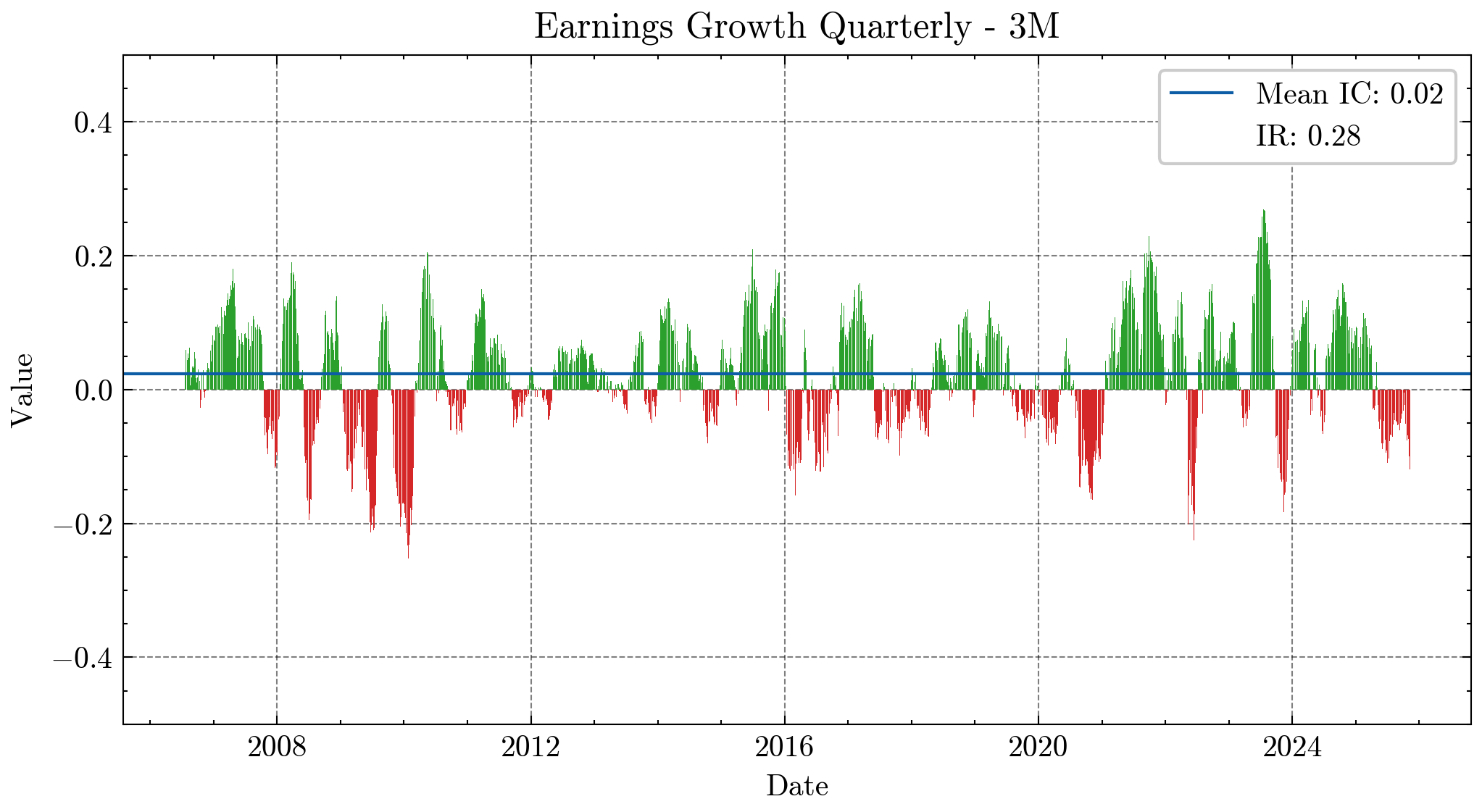

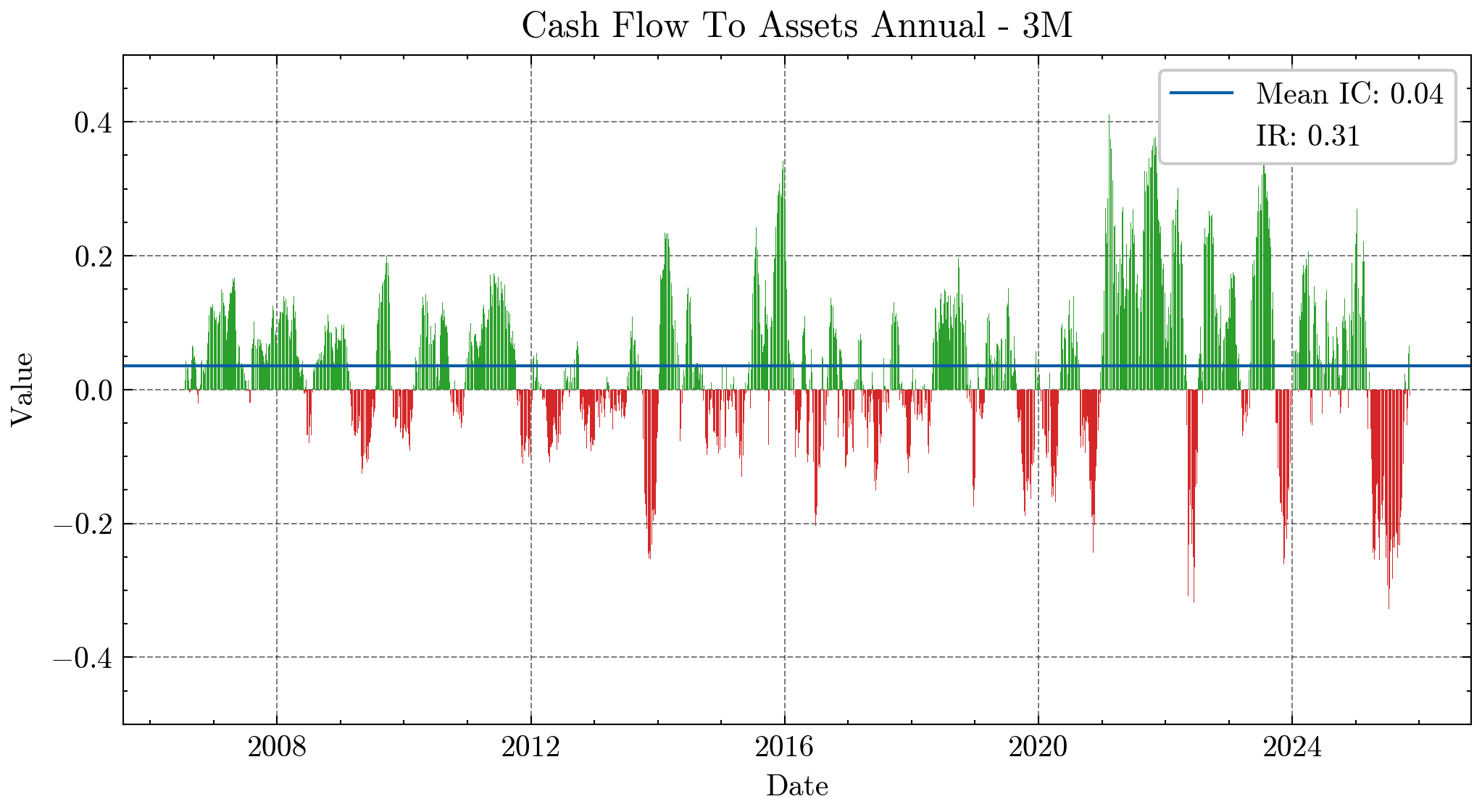

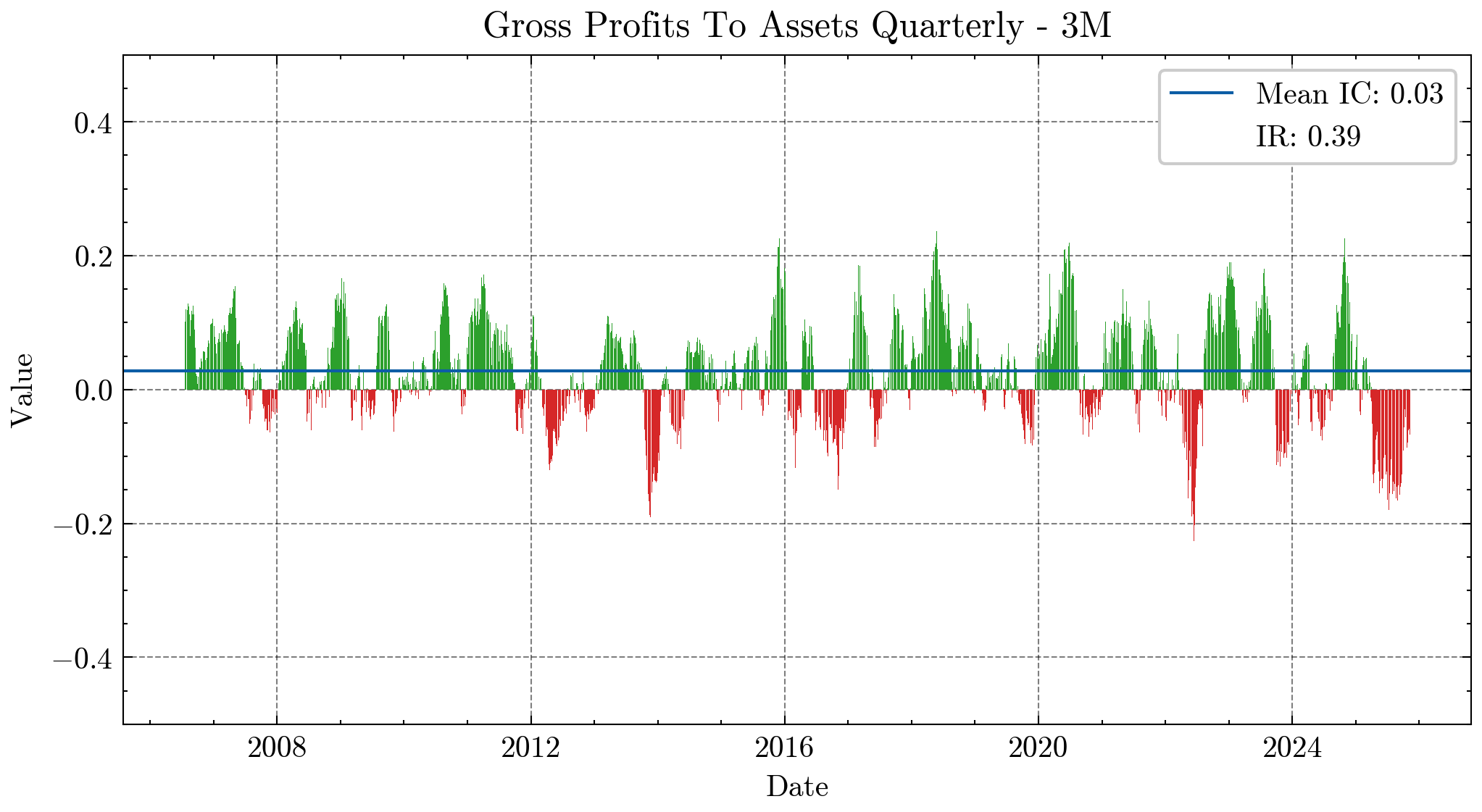

We selected the 3-month forward return horizon for our results below. Interestingly, Earnings Growth shows good predictive return ability, whereas its related factor, Profit Growth, has a very low factor return. Profit Quality-related factors like Return on Equity, Return on Assets, Cash Flow to Assets, Gross Profits to Assets, and Sales to Assets also generally show strong IRs at this horizon.

Figure 1: Time history of 3-month IC of Earnings Growth exposure, with a 0.28 IR

Figure 2: Time history of 3-month IC of Cash Flow to Assets exposure, with a 0.31 IR

Figure 3: Time history of 3-month IC of Gross Profits to Assets exposure, with a 0.39 IR

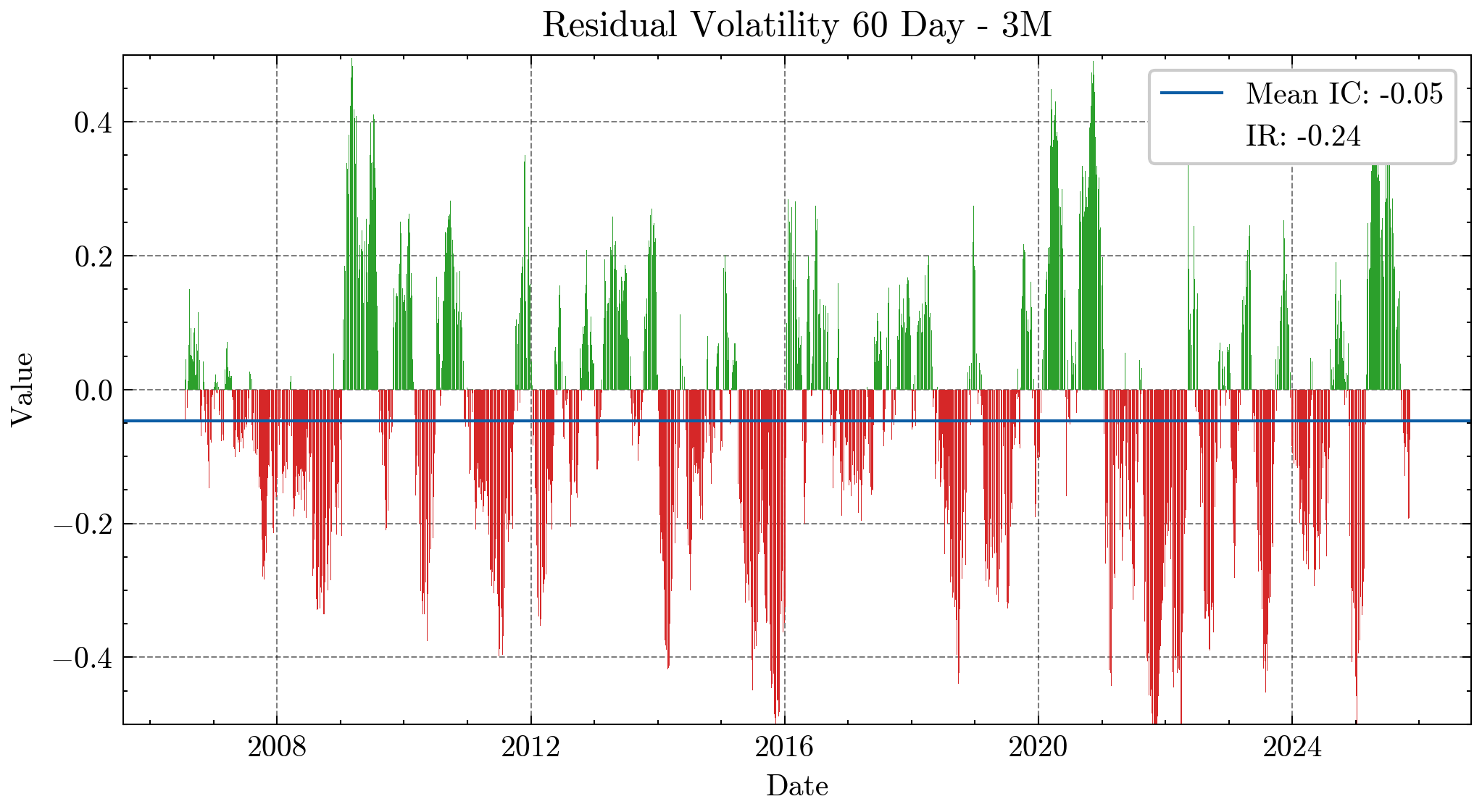

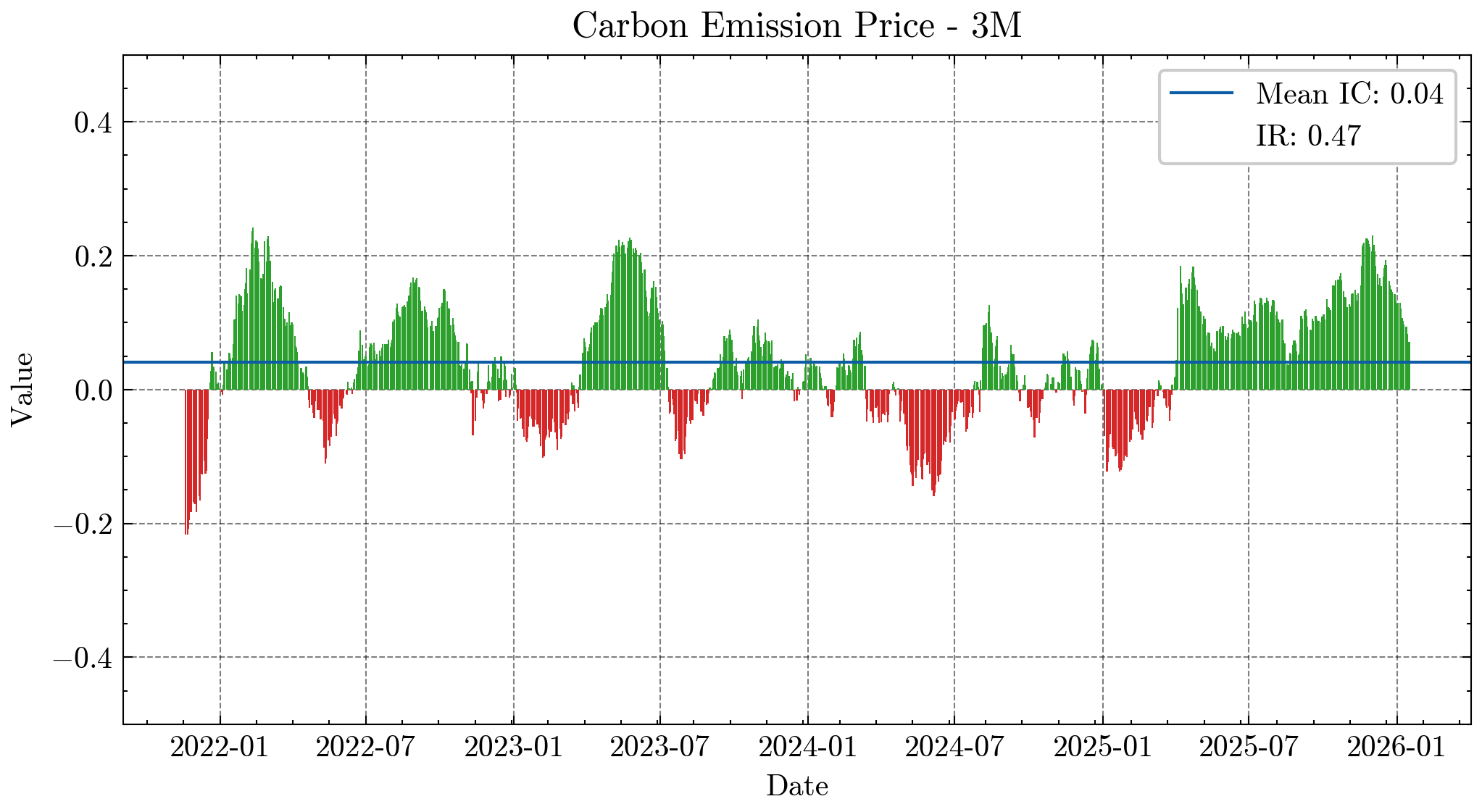

Certain risk-related technical factors such as Max Return, Downside Volatility, and Residual Volatility also perform well, predicting future underperformance. The Carbon Emission Price macro factor also showed surprising positive significance at various horizons.

Figure 4: Time history of 3-month IC of Residual Volatility 60 Day exposure, with a -0.24 IR

Figure 5: Time history of 3-month IC of Carbon Emission Price exposure, with a 0.47 IR

Factor research vs. backtesting: How to interpret these results

While this exercise is a proof of concept and not a formal backtest of an investible strategy, it demonstrates that the library contains factors with genuine signal worth investigating. Accessing Axioma data such as the Factor Library Suite through Snowflake delivers a powerful mix of high‑quality modeling and scalable compute. For quant teams looking to extend their factor universe, test new signals against a rigorous research baseline, or build custom models, the Axioma Global Factor Research Library – comprising over three dozen factors that weren’t included in the v5.1 model – is also now available.

"The Carbon Emission Price macro factor showed surprising positive significance."

You may also like