EQUITY RISK MONITOR HIGHLIGHTS

WEEK ENDED JUNE 12, 2026

This week we focus on the SpaceX IPO — the largest in history — and what its imminent inclusion in the Russell 1000 means for index and sector composition, benchmark divergence, and risk models.

Benchmark choice has quietly become an active decision

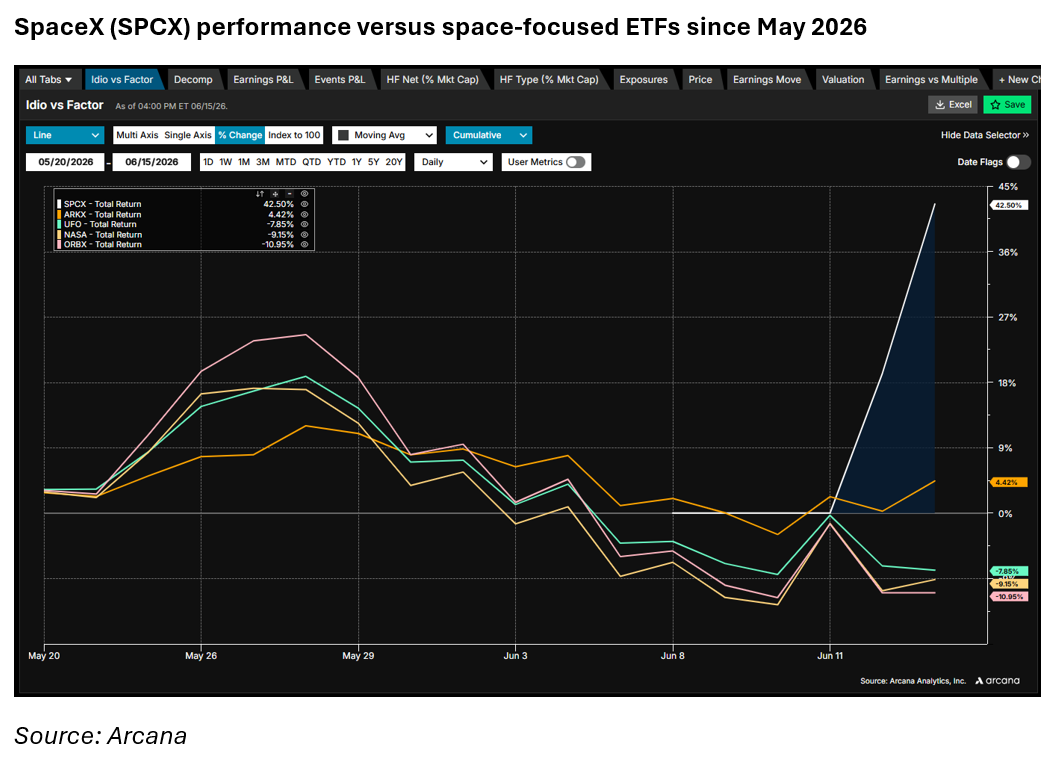

On June 12, SpaceX (ticker: SPCX) completed the largest initial public offering in stock market history, raising approximately $75 billion — roughly 2.9 times the previous record set by Saudi Aramco, a Saudi energy company that was included in the Emerging Markets indices in 2019. SPCX gained 19% on its first day of trading for a total of nearly 43% though Monday, vaulting the company to a $2.52 trillion market capitalization and making it the sixth-largest publicly traded company in the United States.

SPCX is primarily traded on the Nasdaq Global Select Market, with dual-listed access on Deutsche Börse via Xetra and Börse Frankfurt to accommodate European investors. While the company also facilitated retail allocations through the London Stock Exchange, attempts to offer tokenized derivative versions on cryptocurrency exchanges were ultimately cancelled on opening day.

Perhaps the most striking feature of the SpaceX listing is what it reveals about the growing divergence among benchmarks that investors often treat as interchangeable proxies for "US large-cap equities." FTSE Russell's recently approved fast-entry mechanism places SpaceX in the Russell 1000 effective June 26. The Nasdaq-100 is expected to follow within 15 trading days. The S&P 500, however, said “NO” — its 12-month seasoning period and GAAP profitability requirements remain in place, meaning SpaceX will not be eligible for inclusion until at least mid-2027.

FTSE Russell 1000’s new rule allows any IPO with an investable market capitalization clearing the Russell Top 500 threshold to qualify after just five trading days. SpaceX’ formal inclusion in the Russell 1000 will coincide with the date of June 2026’s index reconstitution. This coincidence was engineered: SpaceX timed the IPO for the reconstitution window, and FTSE Russell used its discretion to align the effective date with the reconstitution date (June 26), a coordinated outcome that benefits index funds, market makers, and SpaceX itself.

Historically, IPOs would have waited until a quarterly or annual review, but recent rule changes allow mega-cap listings to enter benchmark indices much earlier—bringing forward passive demand while increasing short-term market impact around inclusion dates.

Therefore the divergence in index constituents is not only structural rather than temporary, but may also potentially widen as other mega-cap private companies, including OpenAI and Anthropic, follow SpaceX through the same index-inclusion pathway over the next 12 to 18 months.

Low float, low index impact (for now)

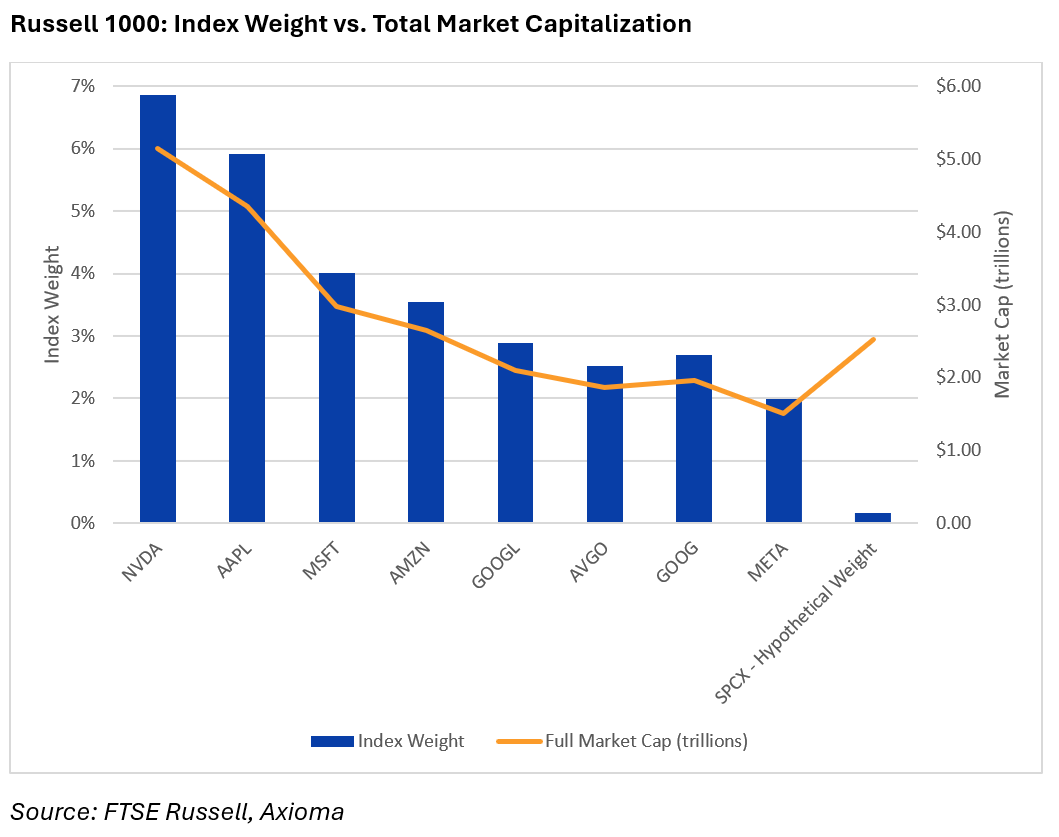

Despite being one of the largest US companies, SpaceX’s initial weight in the Russell 1000 is expected to be relatively low, at around 17 basis points based on current estimates. This is significantly lower than that of peers of similar size, reflecting its limited free float at IPO. Over time, however, as lock-up periods expire and assuming the stock appreciates, both free float and index weight are likely to increase.

What immediate inclusion in the Russell 1000 means in practice is that, by month-end, every passive fund tracking the index will be a forced buyer of a company with barely two weeks of trading history, no established record of profitability, and a public float of just 4%.

The implications for portfolio managers benchmarked to the Russell 1000 are equally immediate. Managers who do not own SpaceX will incur tracking error upon its inclusion, while those who do will assume exposure to a company with no earnings history, extreme float scarcity, and a valuation that several independent research firms have deemed substantially above fair value.

Although SpaceX’s float-adjusted weight at inclusion will be modest, it is still sufficient to trigger an estimated $20 to $27 billion in forced passive buying within weeks. This creates a feedback loop where automated buying pushes prices higher, increases the market-cap weighting, and forces funds to buy even more.

To fund these purchases, index-tracking funds must sell proportional slices of every other Russell 1000 constituent—a mechanical rebalancing that will reshape the index’s sector composition, concentration profile, and risk characteristics in ways that warrant close monitoring.

Defining SpaceX financial identity

Following SpaceX’s public SEC filings on May 20, 2026, the space segment declined. Space-focused ETFs fell between 2% and 12% from May 20 through the day preceding the IPO, potentially reflecting capital recycling as both institutional and retail investors trimmed existing positions to make room for a larger, more liquid name.

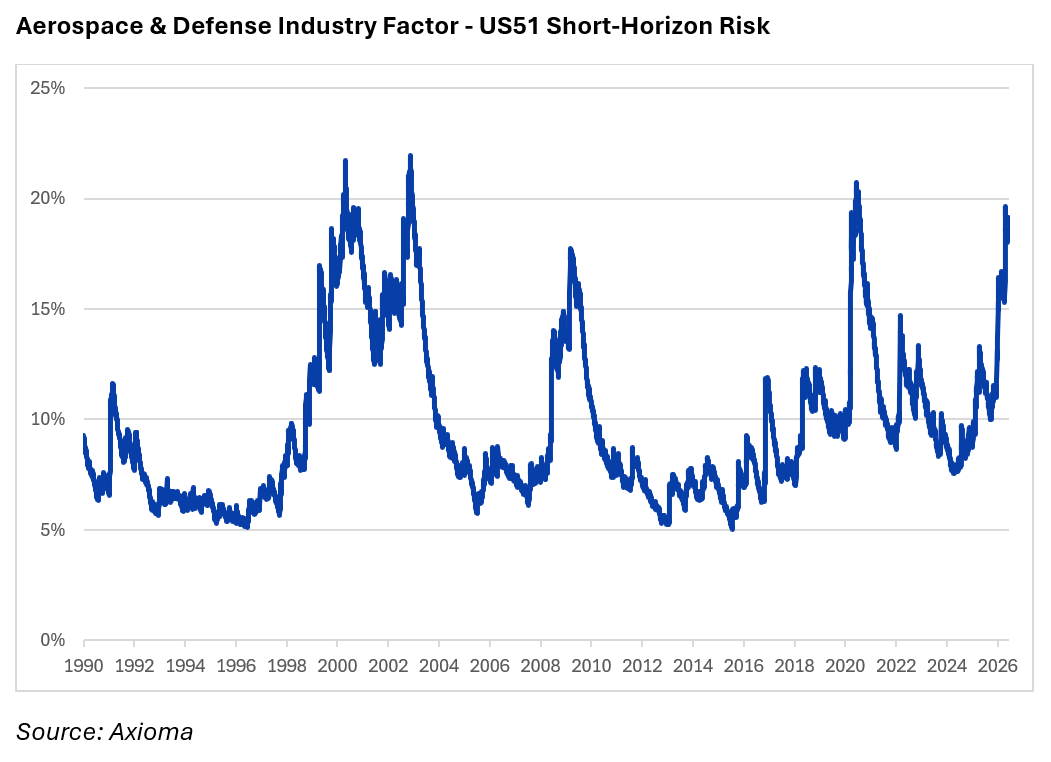

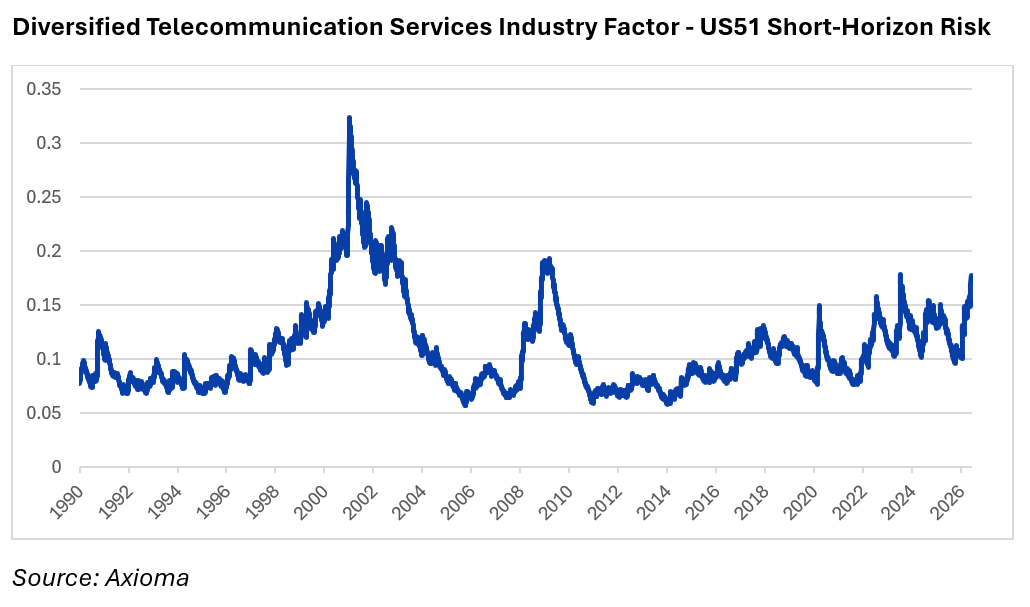

The volatility of the Aerospace & Defense industry factor in the US51 fundamental short-horizon model also spiked this year. Although risk levels have been relatively stable over the past two months, they remain above those seen during the Global Financial Crisis (GFC) and are approaching levels observed during the COVID crisis. While much of this increase is clearly tied to the evolving geopolitical landscape—particularly tensions in the Middle East—SpaceX’s emergence in public markets may have contributed as well.

Yet, SpaceX spans at least three distinct industries—aerospace launch services, satellite broadband, and artificial intelligence—raising questions about how index and risk model providers will classify it and the implications for industry-factor exposures.

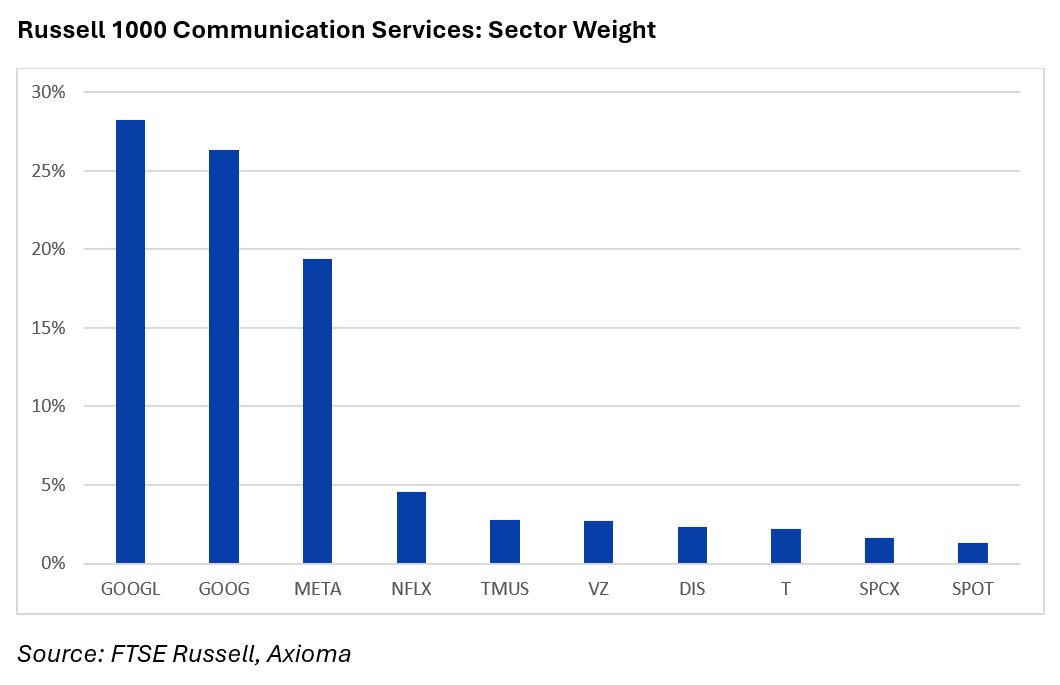

Axioma will follow the GICS classification, which is driven by the company’s dominant revenue stream, placing SPCX in the Diversified Telecommunication Services industry within the Communication Services sector (alongside Alphabet and Meta), rather than with Aerospace and Defense contractors in the Industrials sector. This reflects the fact that the majority of SpaceX’s multibillion-dollar revenue is generated by its Starlink Connectivity segment rather than traditional rocket manufacturing. The Diversified Telecommunication Services Industry Factor has also experienced a notable increase in risk, now reaching levels similar to those seen during the GFC.

With a float valued at approximately $123 billion, SpaceX would already rank among the top 10 largest companies in Russell 1000’s Communication Services, with an estimated weight of around 2%, highlighting its potential for outsized influence on the sector.

How Axioma risk models absorb a mega-cap IPO

When a company like SpaceX goes public, it does not initially have sufficient trading history for risk models to fully capture its behavior. Axioma addresses this by initially estimating the stock's risk characteristics using the average profile of similar companies in its sector and size group. Market-based factor exposures are further shrunk towards the cap-weighted mean for the sector and region. As SpaceX accumulates actual trading and fundamental data, the model gradually shifts from these model-based estimates to the company's own observed behavior.

The same approach applies to stock-specific risk. Initially, SpaceX’s idiosyncratic risk is approximated using peer characteristics, but as return data becomes available, this proxy is replaced by the company’s realized risk profile. The full transition from “new IPO” treatment to standard coverage typically takes several months to about a year, depending on the factor.

SpaceX will become eligible to enter the estimation universe of the Axioma risk models in about a month for both short-horizon and medium-horizon models, though inclusion at this time is not guaranteed.

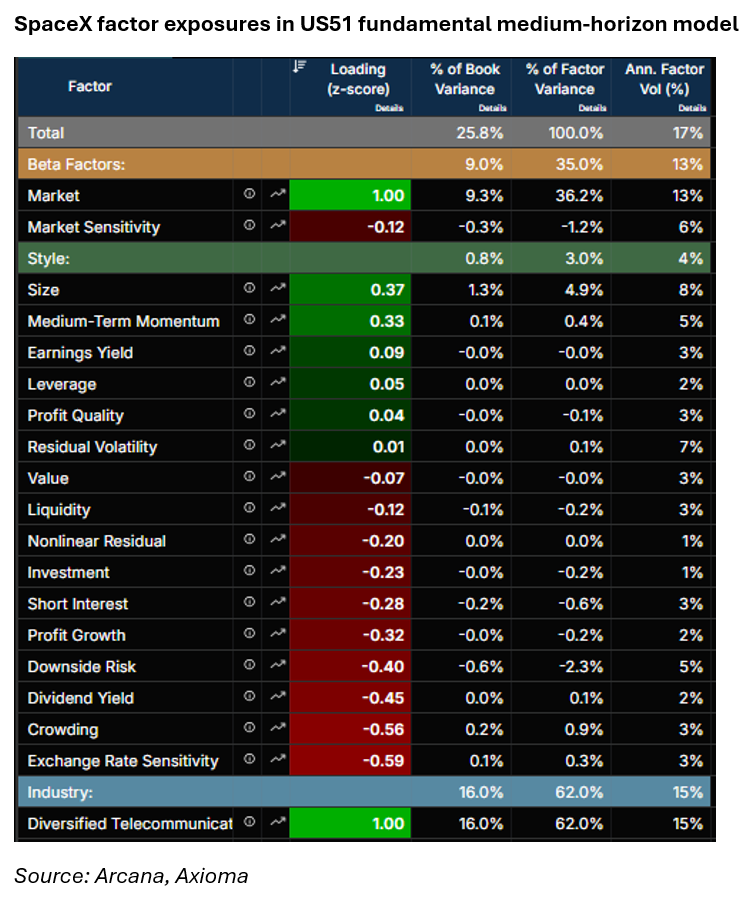

Expected Style Factor Exposures

Because SPCX data is not yet in the model, its style factor exposures debuted with proxy fundamentals, based on similar companies in terms of Size, Region, and Sector.

SpaceX is expected to exhibit a large positive Size exposure, reflecting its market capitalization (distinct from free float used in index weighting). Proxy estimates already indicate this effect in the US51 fundamental medium-horizon model.

Proxy fundamentals suggest a slightly negative Value tilt and a strongly negative Dividend Yield exposure. As the model transitions to company fundamentals, these exposures are likely to remain or become more negative, given the company’s reported net loss in FY2025, lack of dividends, and high valuation multiple.

The proxy also indicates a modest negative Investment exposure. However, if SpaceX continues to deliver strong revenue growth, this could shift to a positive investment profile over time.

Downside Risk and Market Sensitivity exposures initially default to the capitalization-weighted averages of sector peers (currently negative). However, early trading activity—including a 19% first-day gain and intraday swings of up to 30%—suggests realized volatility may exceed these averages as firm-specific data is incorporated.

Similarly, Momentum exposures would start at the sector average (currently positive) and gradually incorporate SpaceX's actual returns over the next several months to a year. The factor exposure will blend in a proportion of the fraction of actual trading days to the required number of days for the factor. In one month, it will be 1/12th proxy returns (including 1 month of real returns) and 11/12 cap-weighted sector average. Proxy returns are based on a PCA model to similar companies in terms of Size, Sector, and Region.

SpaceX’s Leverage exposure (currently slightly positive) is likely to remain moderate to high relative to large-cap peers, reflecting substantial capital expenditures.

Finally, despite its massive market cap, SpaceX's Liquidity exposure is expected to indicate lower tradability than similarly sized peers due to its relatively small free float (only ~4% of shares were offered in the IPO), creating an unusually thin float for a mega-cap name. Currently, proxy exposure is slightly negative.

This analysis is based on Axioma’s 5.1 model suite, though the general treatment will be similar for other models as well.

Axioma standard methodology for mitigating SpaceX impact:

- Robust regression (Huber M-Estimator): If SpaceX's return on a given day is an outlier relative to what the model expects given its exposures, the iteratively reweighted regression will downweight SpaceX's contribution, preventing a single extreme day from distorting all factor returns.

- Thin factor correction: If SpaceX comes to dominate its industry factor, the model inserts a dummy asset with a prior return to dilute that dominance and prevent specific return from contaminating the industry factor return.

- Exposure standardization: Style exposures are centered around the cap-weighted mean of the estimation universe. When SpaceX enters the estimation universe, its addition is likely to shift these means slightly which in turn adjusts all assets' standardized exposures. This self-correcting mechanism ensures the broad market benchmark remains approximately factor-neutral.

The broader takeaway is that the mega-IPO era is not a one-time event. For portfolio managers, the Russell 1000 will look different from the S&P 500 for the first time in a structurally meaningful way. Understanding the mechanics of that divergence—from forced passive flows to float-adjusted weighting to governance risk—is no longer optional. It is, quite literally, the price of being indexed.

You may also like