MULTI-ASSET CLASS MONITOR HIGHLIGHTS

WEEK ENDED FEBRUARY 20, 2026

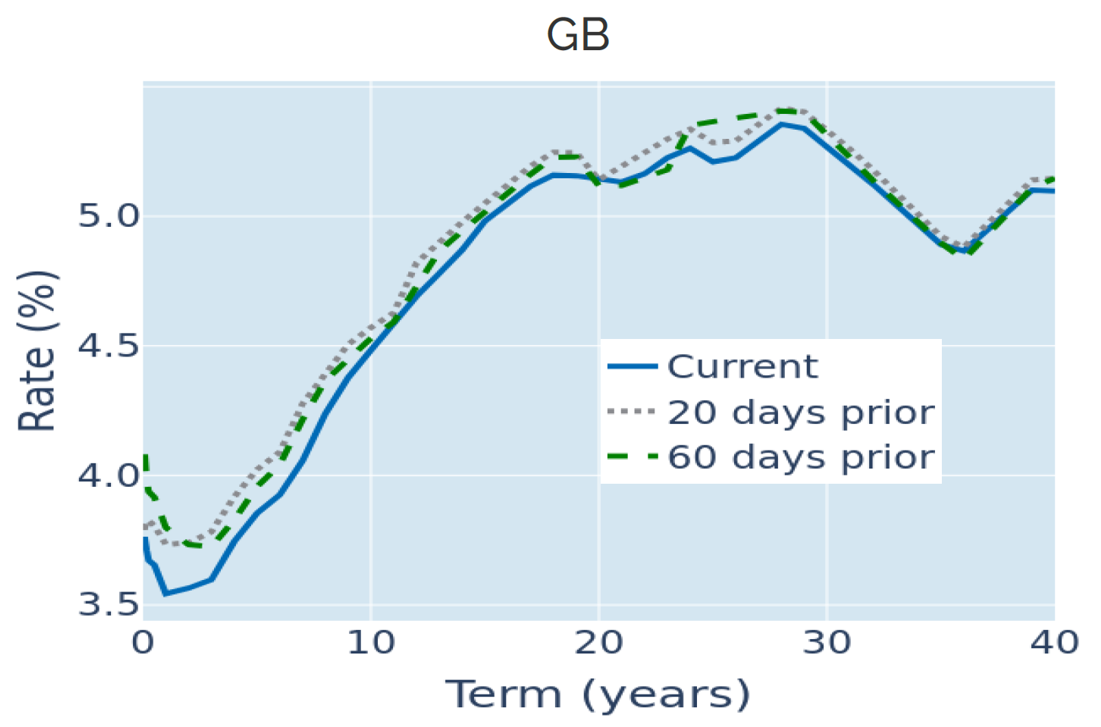

Cooling employment and inflation data depress UK borrowing costs

Cooling employment and inflation data depressed short-dated Gilt yields to their lowest levels in almost three years in the week ending February 20, 2026, as traders again upped their expectations for a Bank of England rate cut next month. The Office for National Statistics reported on Wednesday that the UK unemployment rate climbed from 5.1% in November to 5.2% in December, which marks the highest level since January 2021. Analysts had predicted no change. The case for faster monetary easing was further underpinned by Thursday’s inflation report, which showed that British consumer price growth eased to 3% in the twelve months ending January, down from 3.4% the month before.

The Bank of England expects headline CPI growth to fall even more dramatically over the coming months, taking the annual rate all the way down to the 2% target by April. Much will depend on how much prices will increase during that month itself. In April 2025, headline prices rose by 1.2% on a non-seasonally adjusted basis, as raises in taxes, national insurance contributions, and minimum wages from last year’s spring budget took effect. For comparison, the average month-over-month change in the other eleven months that make up the latest annual figure was 0.15%, which is even slightly less than the 0.16% required to reach the central bank target.

Please refer to Figure 3 of the current Multi-Asset Class Risk Monitor (dated February 20, 2026) for further details.

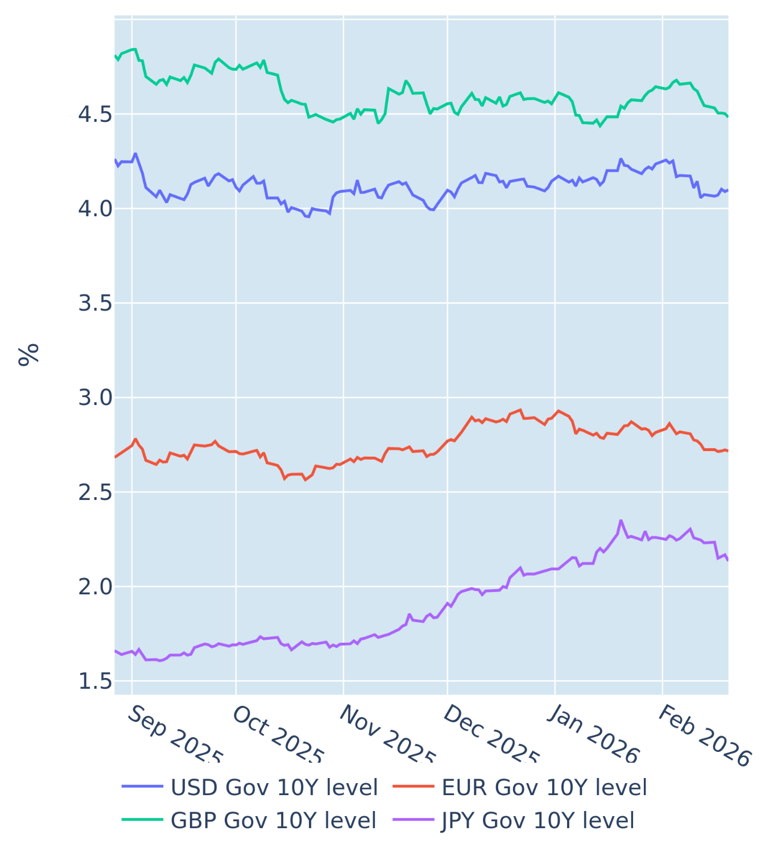

Treasury yields rise as Fed prioritizes inflation over economic growth

US Treasury yields rose across all maturities in the week ending February 20, 2026, as traders revised their monetary policy expectations upward in light of Wednesday’s Fed minutes. The notes from last month’s FOMC meeting showed that most participants perceived a “meaningful” risk of inflation running persistently above the 2% policy objective and that progress toward the target “might be slower and more uneven than generally expected.” As a result, the monetary policy-sensitive 2-year yield ended the week 8 basis points higher, as traders raised the projected federal funds rate for the end of this year from 3.03% to 3.11%. Longer-term borrowing rates also rose between 2 and 4 basis points.

Friday’s surprise drop in GDP growth to 1.4% per annum in the final three months of 2025 from 4.4% in the preceding quarter did little to stem the rise in financing costs, despite coming in at less than half the consensus forecast of 3%. Most of the gap was attributed to a sharp contraction in government spending, due to the 43-day federal shutdown in October and November—the longest in the history of the United States.

Please refer to Figure 4 of the current Multi-Asset Class Risk Monitor (dated February 20, 2026) for further details.

You may also like