MULTI-ASSET CLASS MONITOR HIGHLIGHTS

WEEK ENDED FEBRUARY 27, 2026

Inflation fears after Iran attack boost US Treasury yields, the dollar, and gold prices

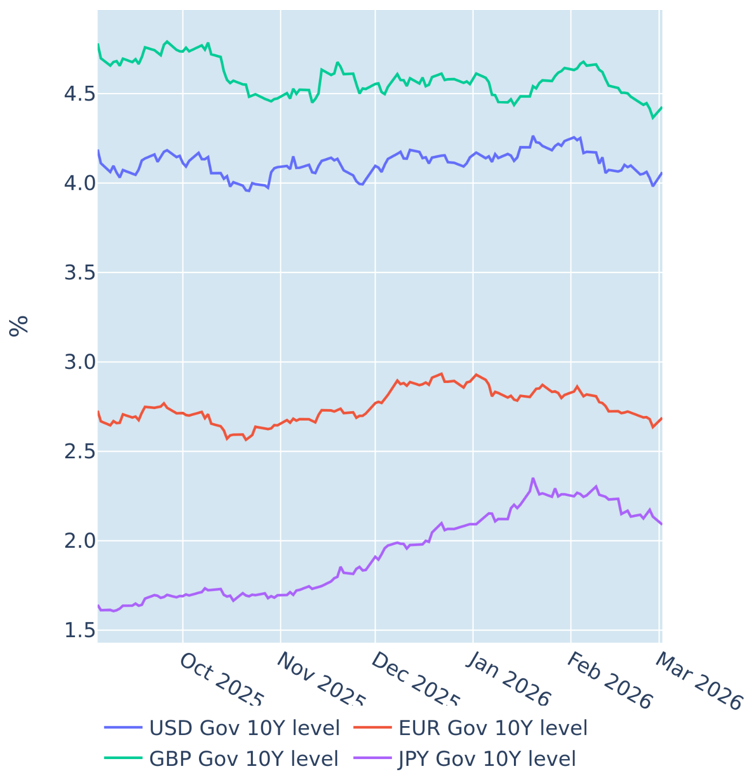

US Treasury yields soared and the dollar strengthened to a six-week high against a basket of major trading partners on Monday, March 2, 2026, following the American attack on Iran over the preceding weekend. The sharp rise in interest rates may have surprised some market participants, triggering speculation that US government debt may have lost its “safe-haven” status, with flows going into gold and USD cash instead. The greenback’s sharp appreciation certainly seemed to underpin that notion. However, there is a more likely explanation that all three were driven by a fourth underlying variable, namely changes in inflation expectations.

For example, the 10-year nominal yield climbed 8 basis points, while the same-maturity breakeven inflation rate rose by 4 basis points. This is in line with the long-term historical average of nominal borrowing rates trading at two times inflation expectations. Yield increases were even bigger at the monetary policy sensitive 2-year point (+0.09%), as traders raised their federal funds rate projection for the year end from 3.05% to 3.16%. This move is also consistent with the inference from the latest FOMC minutes that the Federal Reserve would prioritize price stability over supporting the economy.

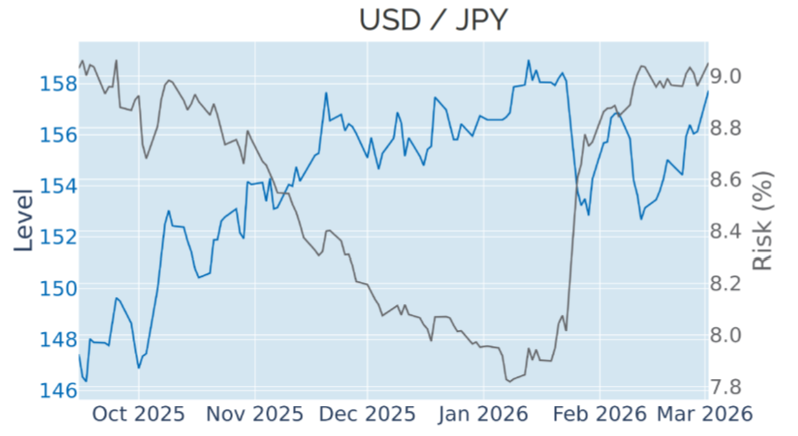

Higher interest rates were also a significant driver behind the dollar’s broad-based strengthening versus most other currencies. On average, the greenback gained around 1% against its G10 peers on Monday alone, though there was some distinction between countries that extract fossil fuels and those that import them. The Canadian dollar and the British pound exhibited the smallest depreciation of 0.5%, followed by the Norwegian krone with -0.8%. At the other end of the spectrum were the Swedish krona and the Swiss franc with -1.6% and -1.5%, respectively. The Japanese yen was right in the middle of the pack with a 1% loss, despite the fact that the country imports almost all of its oil from the Gulf region.

Please refer to Figures 4 & 6 of the current Multi-Asset Class Risk Monitor (dated March 2, 2026) for further details.

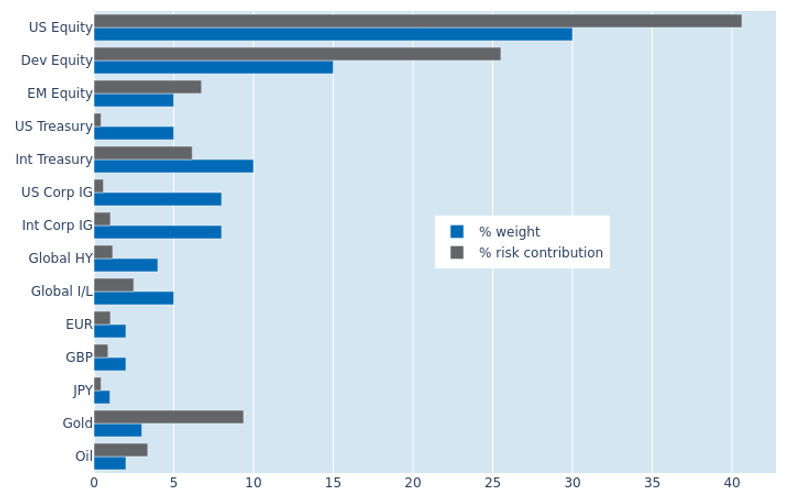

Portfolio risk decreases as FX and equities decouple

The predicted short-term risk of the Axioma global multi-asset class model portfolio fell to 6.8% as of Monday, March 2, 2026, despite the rise in geopolitical uncertainty, as share prices decoupled from exchange rates against the US dollar. As a result, non-USD government bonds saw their share of overall risk drop by a full percentage point to 6.2%, as their returns appeared less correlated with stock markets. Gold recorded a similar reduction of 1.1% in its percentage risk contribution, again driven by a weaker co-movement with share prices. Not too surprisingly, the sharp uptick in oil prices meant that the black commodity added slightly more to total portfolio risk.

Please refer to Figures 7-10 of the current Multi-Asset Class Risk Monitor (dated March 2, 2026) for further details.

You may also like