MULTI-ASSET CLASS MONITOR HIGHLIGHTS

WEEK ENDED MARCH 6, 2026

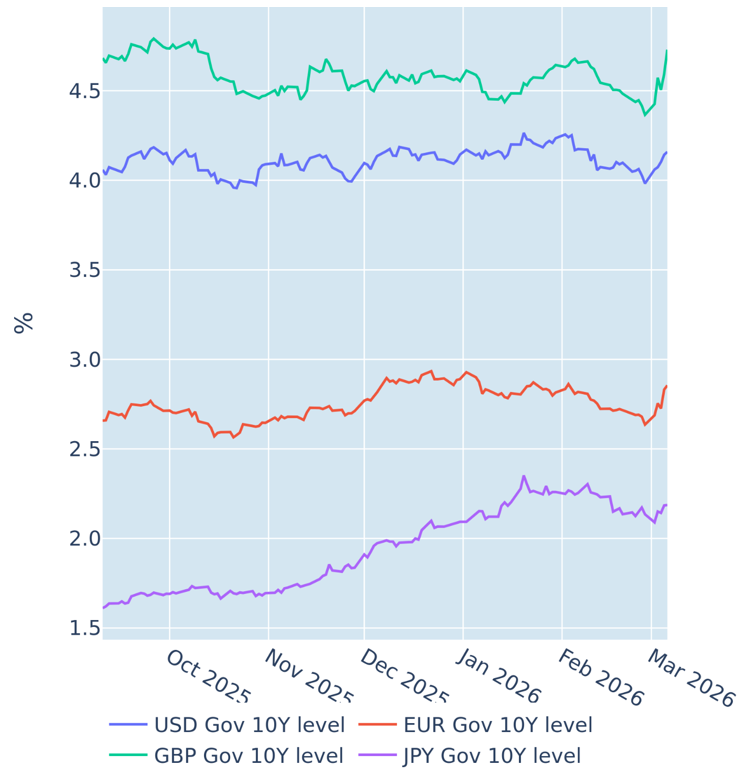

Bond markets brace for rate hikes amid resurging inflation

Global bond markets suffered one of the worst selloffs in years in the week ending March 6, 2026, as soaring oil prices pushed up inflation expectations around the world.

The 10-year US Treasury yield recorded its biggest weekly increase since last April’s Liberation Day tariffs, rising by 0.18% as the same-maturity breakeven inflation rate expanded by 8 basis points. The monetary policy-sensitive 2-year benchmark climbed by a similar amount, with traders raising their year-end projection for the federal funds rate from 3.05% to 3.24%. The increase would likely have been much higher, if it had not been for Friday’s weaker-than-expected non-farm payrolls report, which showed a loss of 92,000 jobs, while economists had predicted a gain of 59,000 new positions. But the fact that markets still priced in less monetary easing despite the dismal labor market performance shows that they continue to expect the Federal Reserve to prioritize its price stability target over its full employment mandate.

Yield increases were even more pronounced on the other side of the Atlantic, with both the European Central Bank and the Bank of England now expected to tighten monetary conditions before the end of the year. For the UK bond market, the move represented a complete reversal of monetary policy expectations in little more than a week. At the end of February, traders were still betting on a potential BoE rate cut in March, followed by another one later in the year. But both cuts have since been priced out, with short-term interest rate markets now assigning a 50% chance to a rate hike. As a result, British Gilts recorded their biggest weekly surge since the ill-fated “mini budget” in 2022. The ECB is now also expected to tighten the monetary screws by 50 basis points over the remainder of the year, as long-term inflation expectations for the Eurozone climbed above 2% for the first time in almost a year, pushing up euro bond yields across all maturities.

Please refer to Figure 4 of the current Multi-Asset Class Risk Monitor (dated March 6, 2026) for further details.

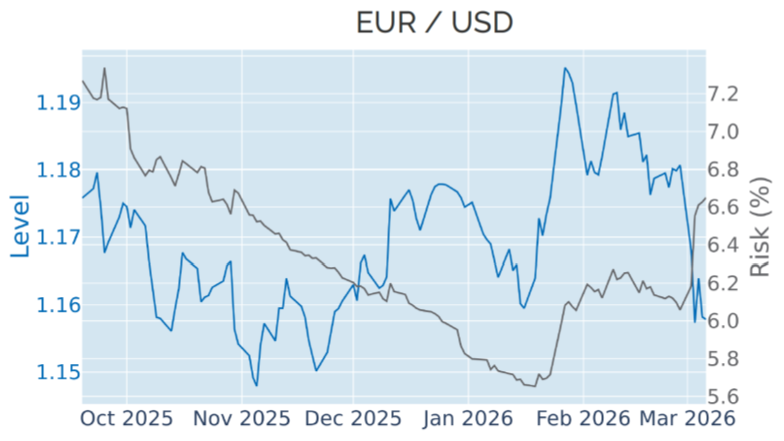

But higher rates lend no support to European currencies

The rising expectations of rate hikes in Europe did little to support the euro or the pound, as the dollar was once again the only beneficiary of higher global interest rates. The euro and the Swedish krona took the brunt of the dollar strengthening, both depreciating around 2% against their American rival, whereas the pound and the Norwegian krone lost only 0.6% and 1%, respectively, thanks to their lower dependence on fossil fuel imports on the Middle East. The Canadian dollar was even slightly up against its southern neighbor.

In an eerie reminder of the aftermath of Russia’s 2022 invasion of Ukraine and the subsequent surge in inflation and bond yields, exchange rates resumed a familiar pattern of the Dollar Index closely tracking federal funds rate projections. Back then, the positive correlation persisted for three years until it was finally broken by the introduction of tariffs in early 2025 and the ensuing capital flight from the United States. The greenback’s renewed strength amid rising interest rates can, therefore, be seen as a sign that investor focus is firmly back on inflation and the anticipated monetary policy response.

Please refer to Figure 4 of the current Multi-Asset Class Risk Monitor (dated March 6, 2026) for further details.

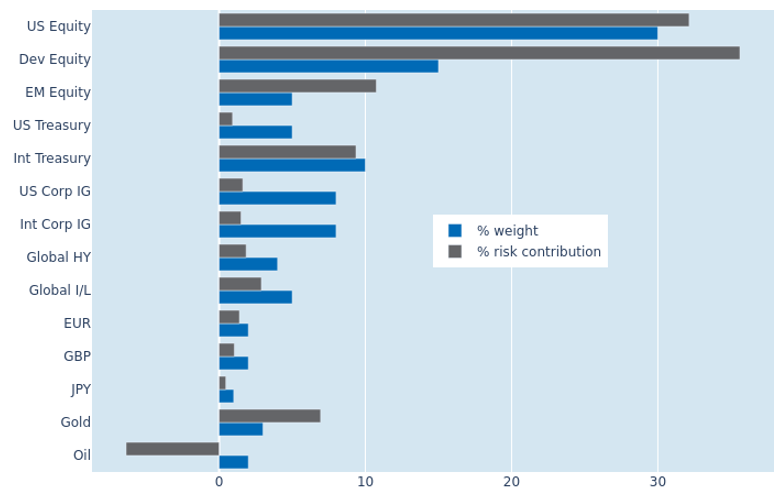

Stronger cross-asset correlations and volatilities boost portfolio risk

Last week’s combined selloff in global stocks, bonds, and foreign currencies against the dollar boosted the predicted short-term risk of the Axioma global multi-asset class model portfolio to 8.7% as of Friday, March 6, 2026, up from 6.9% the previous weekend. The effect was most notable for non-US developed equities, which saw their share of total portfolio risk soar from 24.9% to 35.7%, making them the riskiest asset class in the portfolio relative to their monetary weight of 15%. This was in stark contrast to their American counterparts, whose reduced percentage risk contribution of 32.1% was only marginally higher than their market-value weight of 30%. Thanks to the strong surge in oil prices, holding the black commodity now actively reduces overall portfolio risk despite a doubling of its standalone volatility. In fact, its strong price fluctuations combined with a negative correlation with the rest of the portfolio make it the ideal diversifier…for now.

Please refer to Figures 7-10 of the current Multi-Asset Class Risk Monitor (dated March 6, 2026) for further details.

You may also like