MULTI-ASSET CLASS MONITOR HIGHLIGHTS

WEEK ENDED MARCH 27, 2026

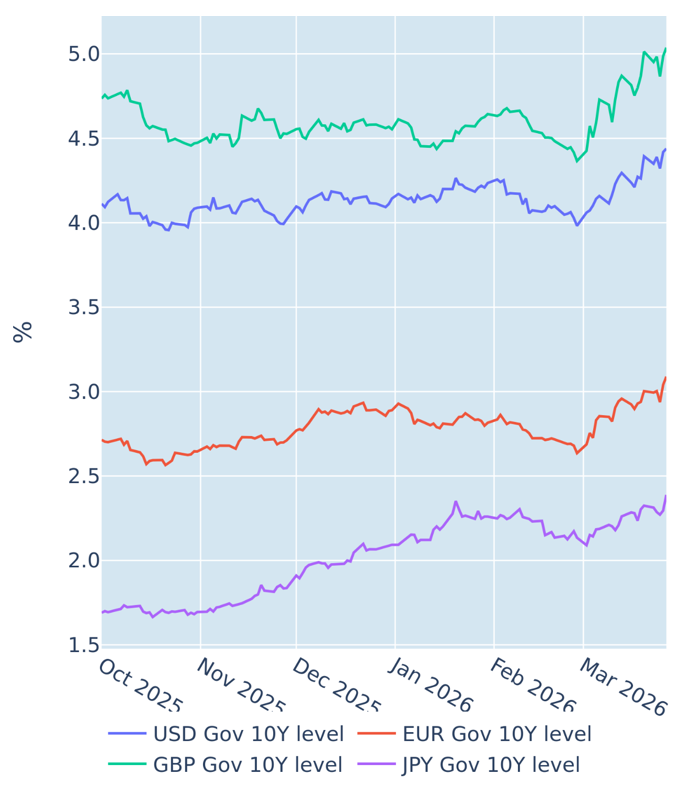

Inflation and fiscal concerns push Eurozone yields to multi-year highs

Eurozone borrowing costs continued to climb for a fourth consecutive week in the week ending March 27, 2026, putting euro area government bonds on track for their worst monthly performance since 2022. The move reflects growing concerns over the fiscal implications of the Iran war, as some administrations contemplate measures to shield households from the soaring energy costs.

Since the start of the month, the benchmark German 10-year yield has risen 45 basis points to its highest level in almost 15 years, with roughly two thirds of the increase driven by higher inflation expectations. Rate increases were even more pronounced at the short end of the curve, where the monetary policy-sensitive 2-year yield rose by nearly 0.7%, as traders priced in close to a full percentage point of monetary tightening from the European Central Bank before year-end.

Italy and Greece both saw their sovereign risk premia widen further, pushing long-term funding costs to heights last seen in 2023. That said, their current yield surcharges of around 1% over German Bunds remain less than half of the levels reached in the wake of Russia’s invasion of Ukraine in 2022.

Please refer to Figure 4 of the current Multi-Asset Class Risk Monitor (dated March 27, 2026) for further details.

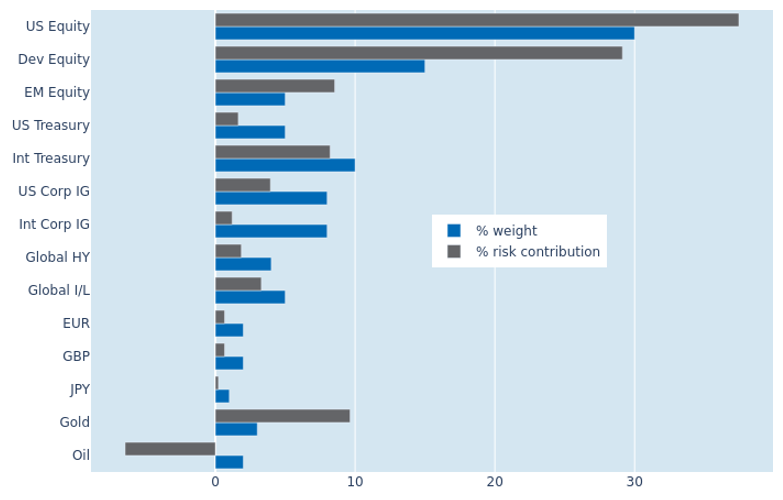

Continued cross-asset selloff raises portfolio risk

The predicted short‑term risk of the Axioma global multi‑asset model portfolio rose 0.6% to a 10-month high of 9.1% on Friday, March 27, 2026, as US equities, Treasury bonds, and gold sold off in tandem for the fourth week in a row. All three asset classes exhibited higher percentage risk contributions, driven by a combination of rising standalone return volatility and stronger cross-asset co-movement. By contrast, non-US developed stocks and fixed income securities experienced a decline in their share of total portfolio volatility, reflecting weaker correlations between local returns and currency movements against the US dollar. Oil remained the only asset in the portfolio that actively reduced overall risk.

Please refer to Figures 7-10 of the current Multi-Asset Class Risk Monitor (dated March 27, 2026) for further details.

You may also like