MULTI-ASSET CLASS MONITOR HIGHLIGHTS

WEEK ENDED APRIL 2, 2026

Global bonds recover as focus shifts from inflation to economic damage

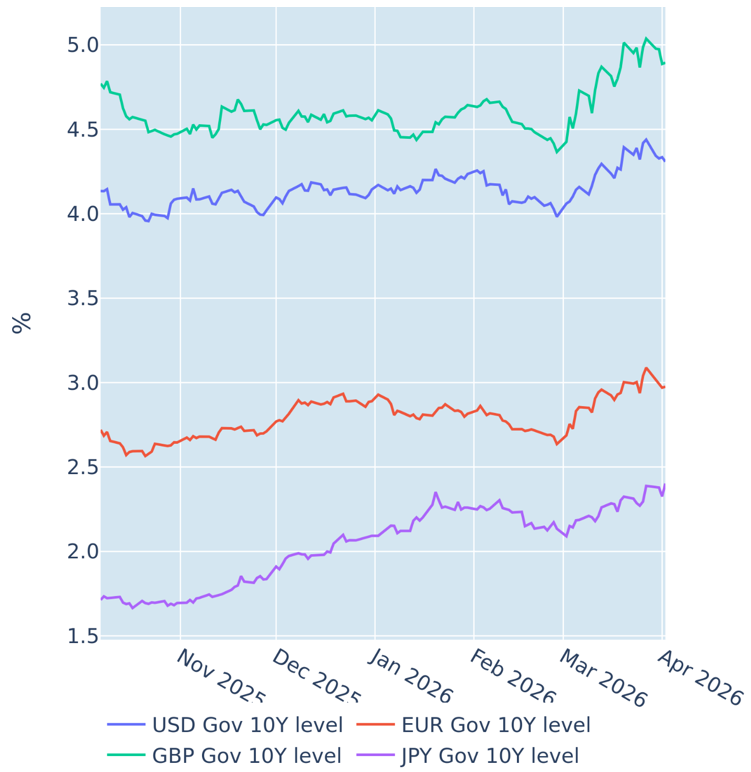

Global sovereign yields eased for the first time since the start of the Iran war in the short week ending April 2, 2026, as investor attention shifted from the inflationary impact of soaring energy prices to the potential damage to global growth. The move reflects a growing view that markets may have become overly pessimistic about the inflation outlook and the likely path of monetary policy.

That said, traders still expect the European Central Bank to hike rates by 75 basis points, the Bank of England to tighten by 50 basis points, and the Federal Reserve to leave its policy target unchanged this year. Longer term borrowing costs in the US and the euro area also remain more than 30 basis points above end February levels, while UK government yields are roughly 50 basis points higher at the 10 year point and around 75 basis points higher at shorter maturities.

Please refer to Figure 4 of the current Multi-Asset Class Risk Monitor (dated April 2, 2026) for further details.

Soaring equity volatility boosts portfolio risk

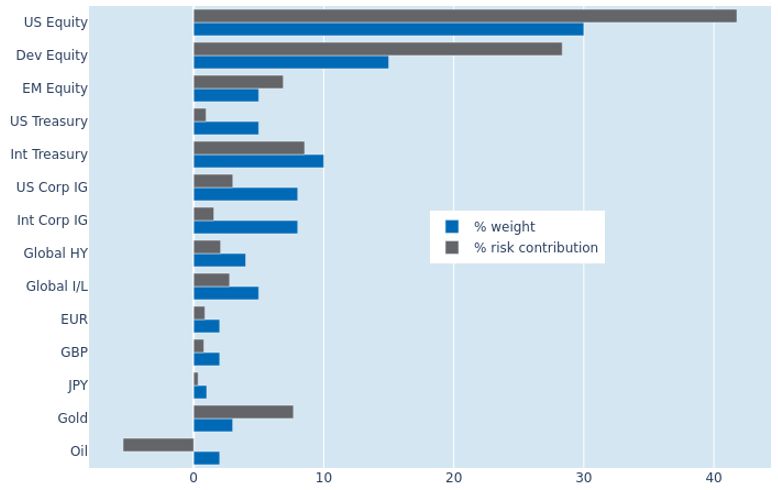

Soaring equity volatility pushed the predicted short term risk of the Axioma global multi asset model portfolio up by 2.5 percentage points to 11.6% as of Thursday, April 2, 2026. US equities accounted for most of the increase, with their share of total portfolio volatility rising from 37.5% to 41.8%. But non US developed shares still contributed a disproportionately high 28.3% of total risk relative to a portfolio weight of 15%, due to the strong positive correlation between local stock markets and exchange rates against the US dollar. Gold remained the riskiest asset, with a risk contribution more than 2.5 times its market value weight, while oil continued to provide diversification benefits and reduce overall portfolio risk.

Please refer to Figures 7-10 of the current Multi-Asset Class Risk Monitor (dated April 2, 2026) for further details.

You may also like