MULTI-ASSET CLASS MONITOR HIGHLIGHTS

WEEK ENDED APRIL 10, 2026

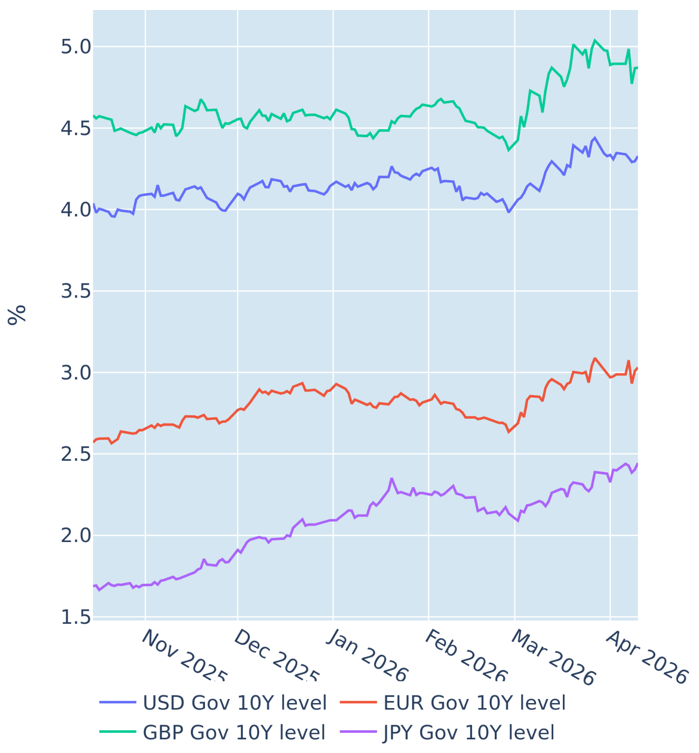

Global bond investors pause to gauge the impact of surging oil prices

Global sovereign yields stabilized in the week ending April 10, 2026, as bond investors weighed the inflationary impact of the ongoing conflict in the Middle East — and the accompanying surge in oil prices — against the potential damage to economic growth.

The conundrum was also reflected in the latest FOMC minutes, released on Wednesday, which noted that “upside risks to inflation and downside risks to employment were elevated.” Regarding the future path of monetary policy, committee members left market participants guessing, warning that persistent inflation “could call for rate increases” while simultaneously stressing that a softening labor market “could warrant additional rate cuts.”

Friday’s US inflation report, meanwhile, shed some light on the short-term impact of higher petrol prices, which lifted annual headline CPI growth from 2.4% in February to 3.3% in March—its largest monthly increase since 2022. Core inflation, however, rose only marginally, from 2.5% to 2.6%. That divergence is not unusual, as oil price shocks tend to take time to feed through into the broader economy via higher transport, energy, and raw material costs. Following the wake of the Russian invasion of Ukraine, for instance, overall US consumer price growth peaked at 9.1% in June 2022, while core inflation reached its high-water mark of 6.6% with a three-month lag.

Please refer to Figure 4 of the current Multi-Asset Class Risk Monitor (dated April 10, 2026) for further details.

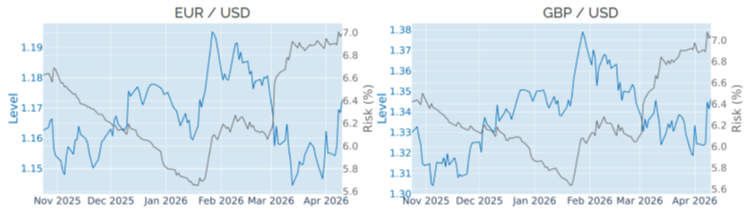

Dollar weakens as traders scale back monetary policy expectations

The US dollar depreciated by 1.4% against a basket of major trading partners in the week ending April 10, 2026, as investors continued to scale back their monetary policy expectations. Federal funds futures for the December once more imply a 30% probability that the Fed could reduce its policy target at least once this year — a sharp reversal from the nearly 44% chance of a rate hike priced in on March 26. European traders also pared back their projections for ECB tightening, from nearly a full percentage point to under 75 basis points. The Bank of England is likewise still expected to raise rates this year, though only by half a percentage point rather than 75 basis points or more.

Please refer to Figure 4 of the current Multi-Asset Class Risk Monitor (dated April 10, 2026) for further details.

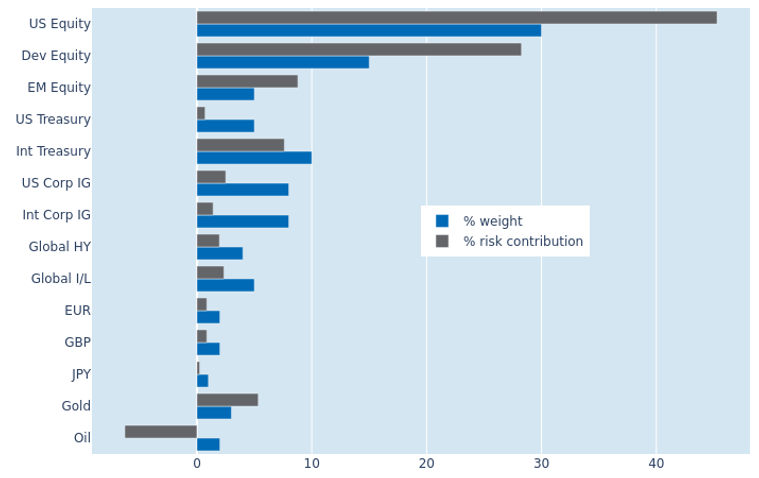

Portfolio risk climbs further amid ongoing stock market recovery

Predicted short term risk for the Axioma global multi asset class model portfolio rose by a further 1.1 percentage points to 12.7% as of Friday, April 10, 2026, as global stock markets continued to recovery, aided by currency gains against the US dollar. US equities recorded the largest increase in their share of total portfolio volatility, rising from 41.8% to 45.3%, followed by emerging markets, whose risk contribution expand by 1.9 percentage points. Developed non-US shares also experienced higher volatility and a stronger co-movement with their American counterparts, though these adverse effects were offset by declining correlations with both gold and oil. The two commodities benefited from this as well: gold saw its risk contribution contract from 7.7% to 5.4%, while oil increased its risk-reducing effect from -5.4% to -6.3%.

Please refer to Figures 7-10 of the current Multi-Asset Class Risk Monitor (dated April 10, 2026) for further details.

You may also like