MULTI-ASSET CLASS MONITOR HIGHLIGHTS

WEEK ENDED APRIL 17, 2026

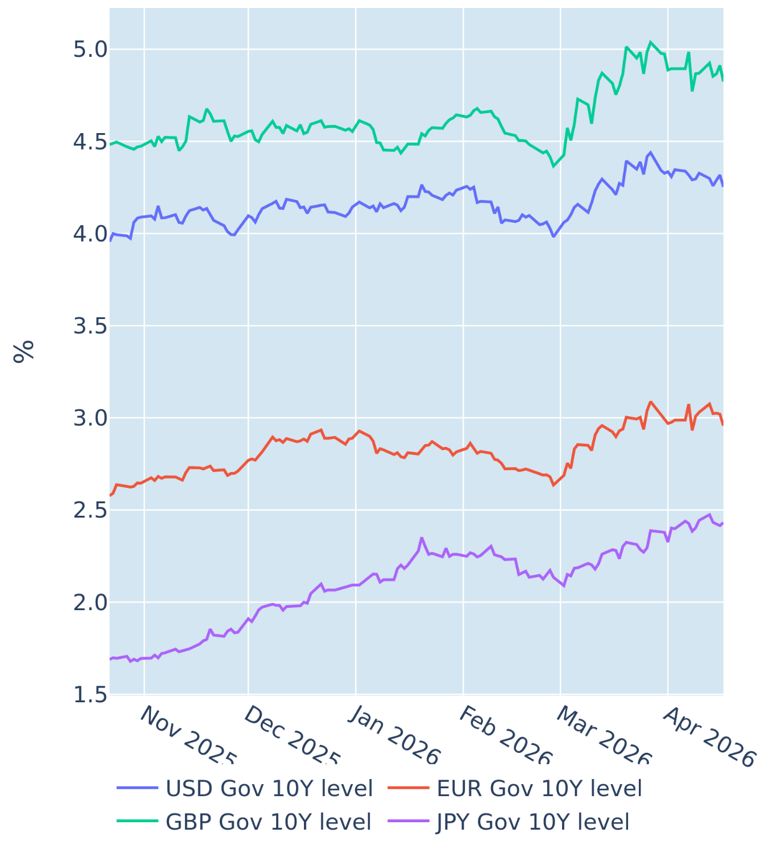

Bond yields ease over softer inflation and Middle East deescalation

US Treasury yields eased to a 4-week low in the week ending April 17, 2026, as investors continued to scale back their expectations of monetary tightening on the back lower-than-expected inflation and signs of deescalation in the Middle East.

The Bureau of Labor Statistics reported on Tuesday that US producer prices increased by 0.5% in March —less than half the pace predicted by analysts — raising the year-over-year growth rate from 3.4% to 4%. Annual core inflation, on the other hand, increased only marginally from 3.5% to 3.6%, mimicking the pattern observed for consumer prices a week earlier. In response, short-term interest rates futures traders raised the implied probability of a Fed rate cut over the next eight months from 23% to 31%.

The odds of Fed easing this year increased even further to over 50% on Friday, following news that the Strait of Hormuz had reopened. The monetary policy-sensitive 2-year yield ended the week 10 basis points lower as a result, while the 10-year benchmark declined by 7 basis points. European and UK borrowing costs also eased, as traders cut year-end rate expectations from three to two hikes for the European Central Bank, and from 50 to 25 basis points for the Bank of England.

Please refer to Figure 4 of the current Multi-Asset Class Risk Monitor (dated April 17, 2026) for further details.

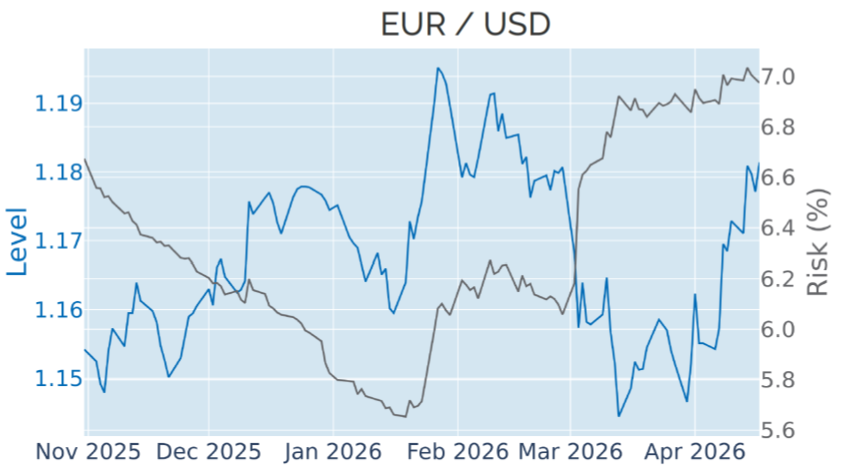

Lower rates continue to weigh on the dollar

The dollar weakened for a third consecutive week against most other currencies, closely tracking developments in fixed income markets, as declining US yields eroded the dollar’s interest‑rate advantage. On Tuesday in particular, all G10 currencies posted gains of between 0.5% and 1% against the greenback as softer inflation data triggered a broad reassessment of near‑term Fed policy.

The euro and the pound climbed to eight week highs, more than recouping their losses since the start of the conflict in the Middle East. Meanwhile, the Australian dollar and the Norwegian krone advanced to levels last seen in 2022, reflecting a seeming investor preference for commodity linked currencies.

Please refer to Figure 6 of the current Multi-Asset Class Risk Monitor (dated April 17, 2026) for further details.

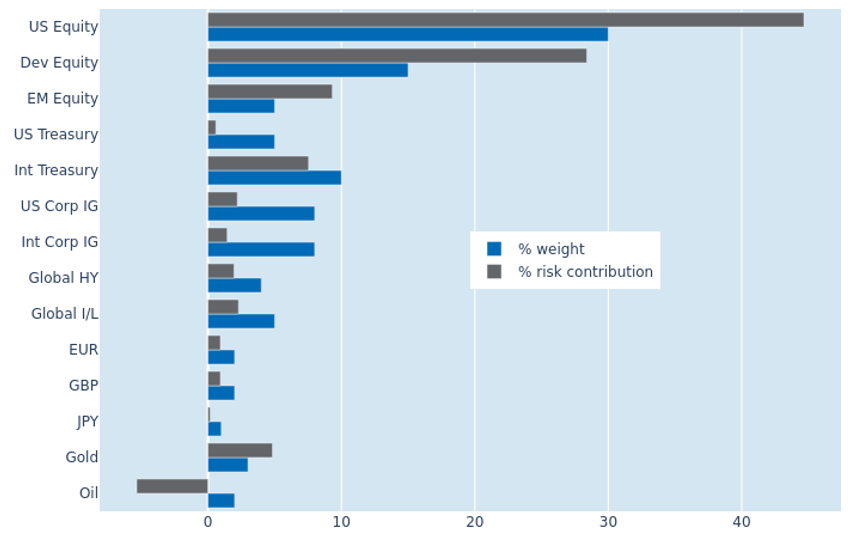

Ongoing stock market recovery reduces portfolio risk

The predicted short term risk for the Axioma global multi asset class model portfolio declined to 11.8% as of Friday, April 20, 2026, as the American stock market extended its recovery into a third week, claiming another all-time high. The reduction in portfolio risk was most pronounced for US equities, with their share of total portfolio volatility shrinking 0.6% to 44.6%. Non-US developed equities also saw their absolute risk contribution decline, but they are now the riskiest asset class relative to their monetary weight, as local share price gains were further boosted by stronger exchange rates against the dollar. Oil continued to provide diversification benefits, though to a lesser extent than in previous weeks, as its negative contribution to portfolio risk narrowed from -6.3% to -5.4%.

Please refer to Figures 7-10 of the current Multi-Asset Class Risk Monitor (dated April 17, 2026) for further details.

You may also like