MULTI-ASSET CLASS MONITOR HIGHLIGHTS

WEEK ENDED APRIL 24, 2026

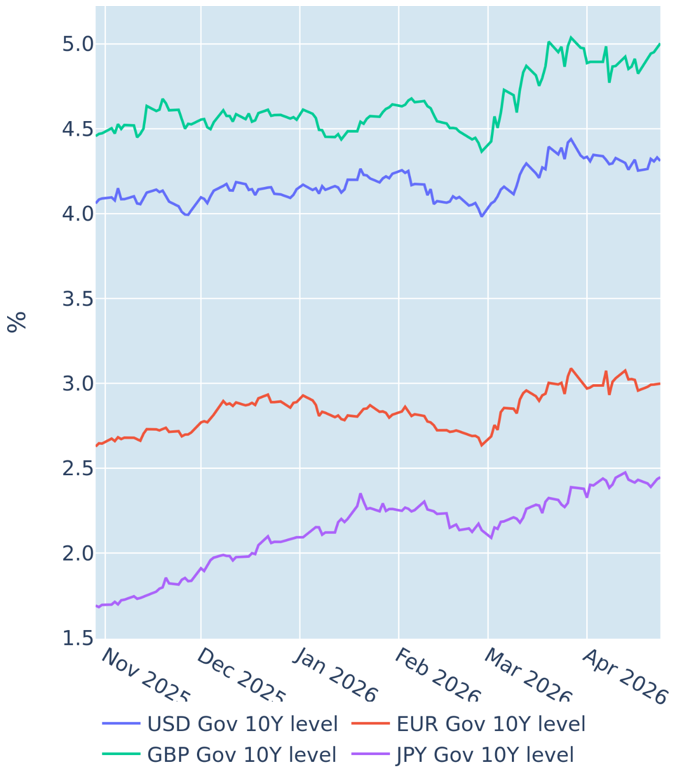

Resurging inflation reignites the ‘higher for longer’ yield narrative

Global bond yields rebounded sharply in the week ending April 24, 2026, as investors again revised monetary policy projections following renewed signs of resurging inflation.

Germany’s Federal Statistical Office announced on Monday that producer prices rose by 2.5% in March, Well above the 1.4% increase predicted by analysts. The rise — the steepest since August 2022 — was largely driven by a 7.5% surge in energy costs, reinforcing concerns that pipeline inflation pressures may be re emerging rather than fading.

In the UK, higher fuel prices and transport costs similarly drove headline CPI inflation higher, from 3.0% year on year in February to 3.3% in March. Core inflation eased modestly from 3.2% to 3.1%, consistent with the experience in other regions that energy shocks take time to propagate through the wider economy, but it remained the highest among G7 economies.

Short term interest rate futures moved to price a materially more restrictive Bank of England policy path, with markets adding almost a full additional rate hike over the next six months compared with the previous week. In response, the 2 year Gilt yield jumped by 27 basis points on the week, while the 10 year benchmark ended 18 basis points higher.

Please refer to Figure 4 of the current Multi-Asset Class Risk Monitor (dated April 24, 2026) for further details.

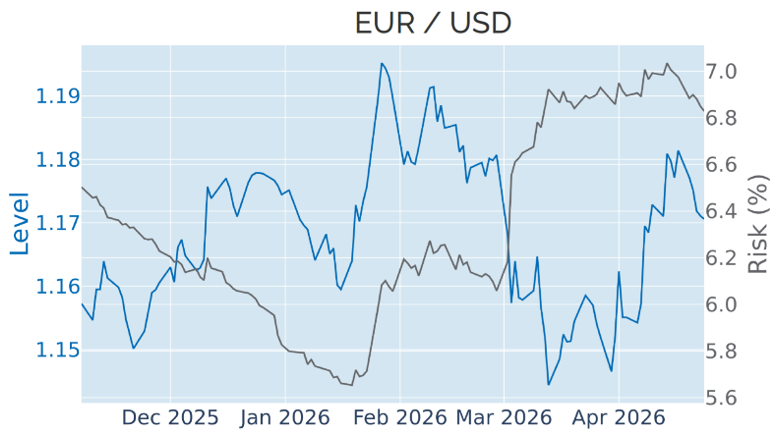

Dollar gains disproportionately from global monetary policy repricing

The dollar was once again the major winner of last week’s upward revision in global monetary policy expectations, appreciating by 0.4% against a trade weighted basket of major partners, even though the projected federal funds rate for December rose only modestly from 3.49% to 3.54%. This contrasted with much larger year end adjustments on the other side of the Atlantic, amounting to 32 basis points implied by SONIA futures and 19 basis points for Euribor contracts. Despite the more limited US repricing, the pound and the euro both depreciated against the dollar, losing 0.5% and 0.9%, respectively. The Japanese yen and Swiss franc also weakened by around 1% each.

Please refer to Figure 6 of the current Multi-Asset Class Risk Monitor (dated April 24, 2026) for further details.

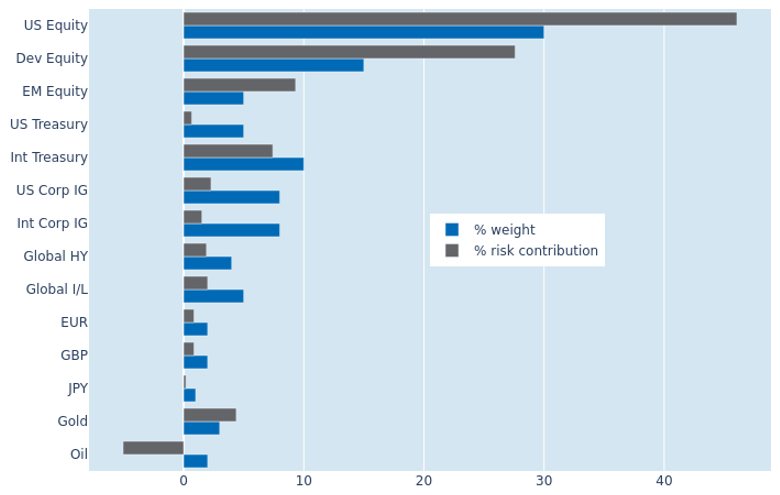

Lower FX and equity volatilities further reduce portfolio risk

A combination of lower FX and equity volatility further reduced the predicted short term risk of the Axioma global multi asset class model portfolio from 11.8% to 10.5% as of Friday, April 24, 2026. The simultaneous decline in these two major sources of volatility primarily benefited non US developed equities, whose share of total portfolio volatility fell from 28.4% to 27.6%. However, the strong positive interaction between local equity returns and exchange rate movements against the US dollar meant that non US equities continued to contribute a disproportionately large share of risk, with relative contributions close to twice their portfolio weight, compared with around 1.5 times for US equities.

Please refer to Figures 7-10 of the current Multi-Asset Class Risk Monitor (dated April 24, 2026) for further details.

You may also like

.png%3Fh%3D810%26iar%3D0%26w%3D1080&w=3840&q=75)

.png%3Fh%3D810%26iar%3D0%26w%3D1080&w=3840&q=75)