MULTI-ASSET CLASS MONITOR HIGHLIGHTS

WEEK ENDED MAY 1, 2026

Fed keeps easing bias — yet rates continue to rise

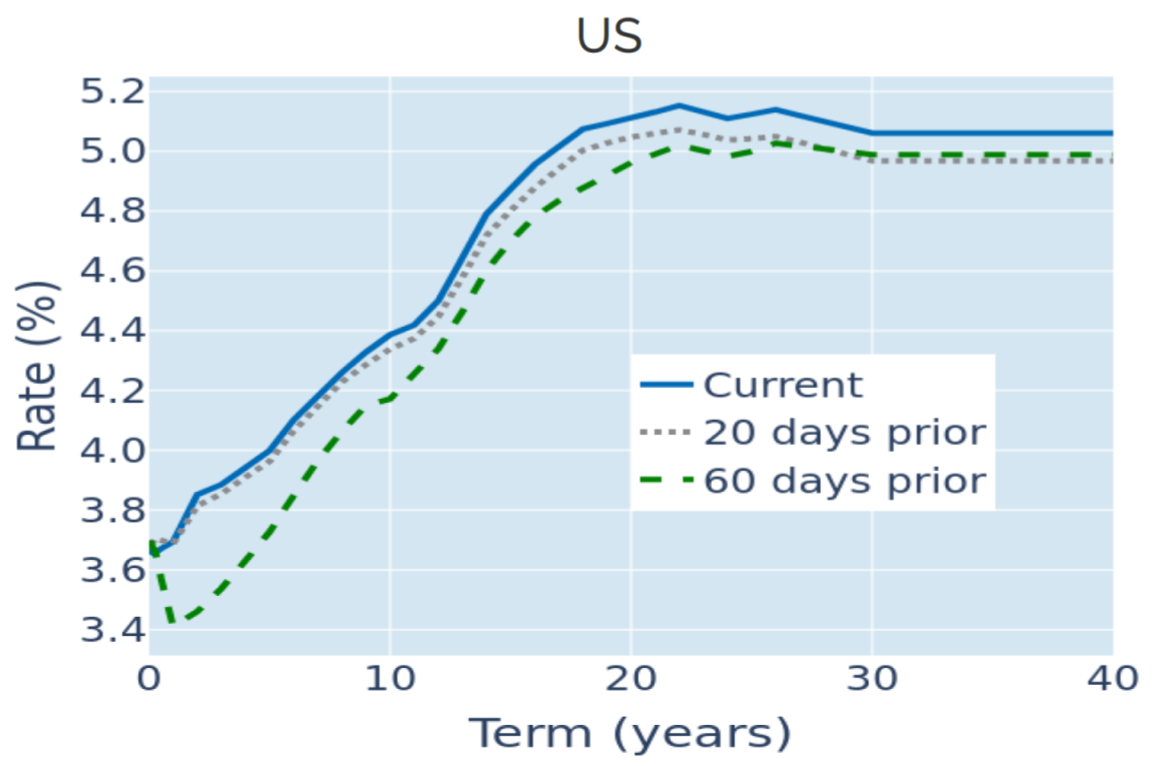

US Treasury yields climbed to five-week highs in the week ending May 1, 2026, despite the Fed maintaining what many observers described as an “easing bias” in its post-meeting statement. As expected, the FOMC kept its policy target unchanged, while noting that “additional adjustments” to rates remained under consideration.

While the wording appears directionally neutral at face value, it has widely been interpreted as signaling further monetary easing. That interpretation rests on the historical context: the qualifier “additional” was introduced in September 2025, when the Fed resumed cutting rates after a nine‑month pause, and has been retained since.

Importantly, the statement also revealed a notable degree of internal disagreement. Three committee members explicitly objected to including the easing language, even though they supported leaving the policy rate unchanged. Stephen Miran once again voted for an immediate 25‑basis‑point rate cut, bringing the total number of dissenters to four — the highest since 1992.

Despite the ostensibly dovish tone of the statement, markets focused on upside risks to inflation and interest rates stemming from higher energy prices. As a result, year-end projections for the federal funds rate were revised upward from 3.54% to 3.63%. The monetary policy-sensitive 2-year yield ended the week 10 basis points higher, while longer-dated rates rose by 8 basis points.

Please refer to Figure 3 of the current Multi-Asset Class Risk Monitor (dated May 1, 2026) for further details.

Dollar no longer profits from higher rates, as Tokyo intervenes

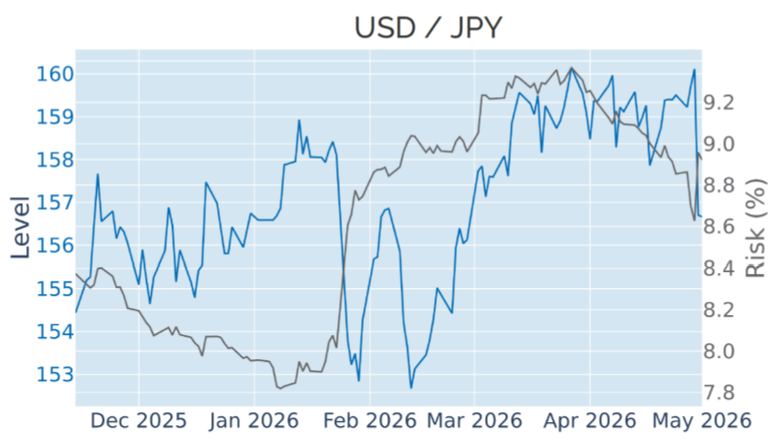

Unlike in the previous week, the dollar no longer benefitted from the continued upward revision in monetary-policy expectations and instead depreciated against all other G10 currencies. The largest move was against the Japanese yen, which gained more than 2% on Thursday amid reports of direct FX market interventions by authorities in Tokyo. The government action was accompanied by increasingly forceful warnings that it would no longer tolerate further weakness in its currency.

The move followed the Bank of Japan’s decision a day earlier to hold its policy rate steady, in line with market expectations, while highlighting inflation risks linked to the conflict in the Middle East. As with the Federal Reserve, the BoJ meeting revealed diverging views within the policy committee, with three of its nine members voting for an immediate tightening of monetary conditions.

Please refer to Figure 3 of the current Multi-Asset Class Risk Monitor (dated May 1, 2026) for further details.

Portfolio risk declines further as FX and equity volatilities continue to fall

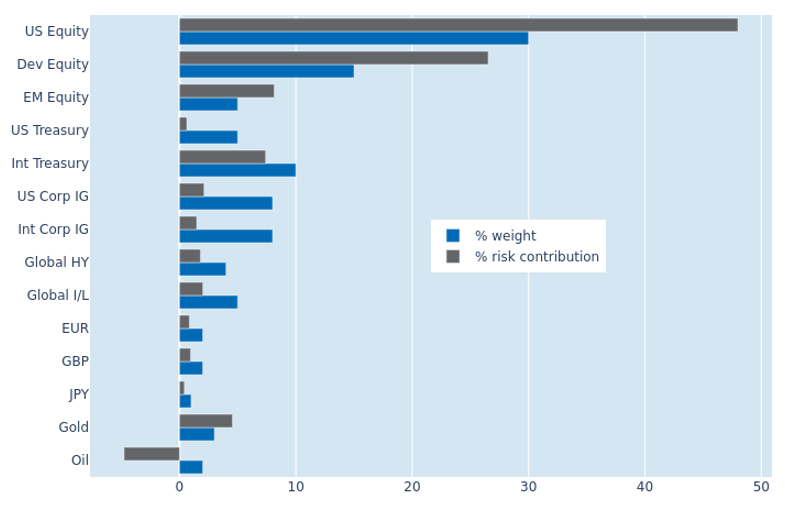

The predicted short term risk of the Axioma global multi asset class model portfolio declined another percentage point to 9.5% as of Friday, May 1, 2026, as equity and FX volatilities continued to fall for a fourth consecutive week. The reduction in risk was most pronounced for developed and emerging market equities, whose risk contributions declined by 1.1 and 1.2 percentage points, respectively. In contrast, US equities saw their share of total portfolio volatility rise by two percentage points to 48%. The remainder of the portfolio was largely unaffected, with cross‑asset correlations showing almost no change over the week.

Please refer to Figures 7-10 of the current Multi-Asset Class Risk Monitor (dated May 1, 2026) for further details.

You may also like

.png%3Fh%3D810%26iar%3D0%26w%3D1080&w=3840&q=75)

.png%3Fh%3D810%26iar%3D0%26w%3D1080&w=3840&q=75)