MULTI-ASSET CLASS MONITOR HIGHLIGHTS

WEEK ENDED MAY 15, 2026

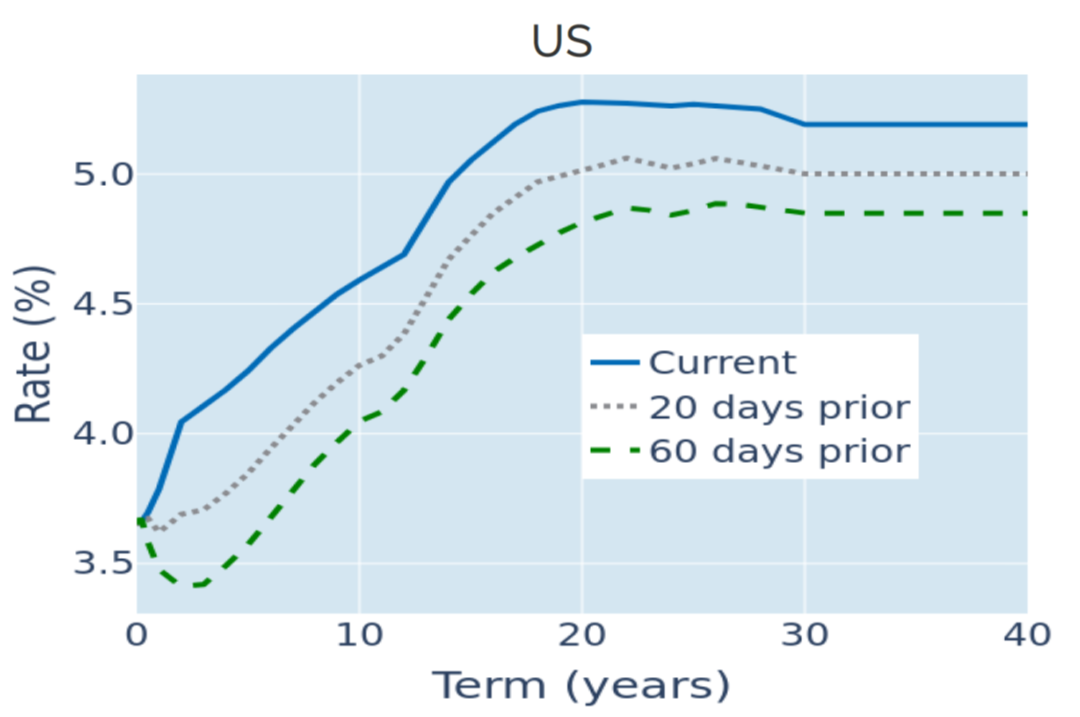

Inflation fears push Treasury yields to 16-month highs

Stronger‑than‑expected inflation pushed US Treasury yields to 16‑month highs in the week ending May 15, 2026, as traders raised the implied probability of a Fed rate hike this year to around 50%.

The Bureau of Labor Statistics reported on Tuesday that US headline consumer prices rose by 3.8% in the twelve months to April, up from 3.3% in March and above analyst expectations of 3.7%. The increase was predominantly driven by fuel and energy costs, with core inflation rising more moderately from 2.6% to 2.8%, although economists had again expected a smaller increase to 2.7%.

Inflation concerns were further exacerbated by another surge in oil prices on Friday, with Brent crude rising by more than 4%, as the Strait of Hormuz remained closed amid a lack of progress in peace talks between Iran and the US. The 30‑year Treasury yield climbed to its highest level since 2007, while the 10‑year benchmark returned to levels last seen when President Trump entered office in early 2025.

Please refer to Figure 3 of the current Multi-Asset Class Risk Monitor (dated May 15, 2026) for further details.

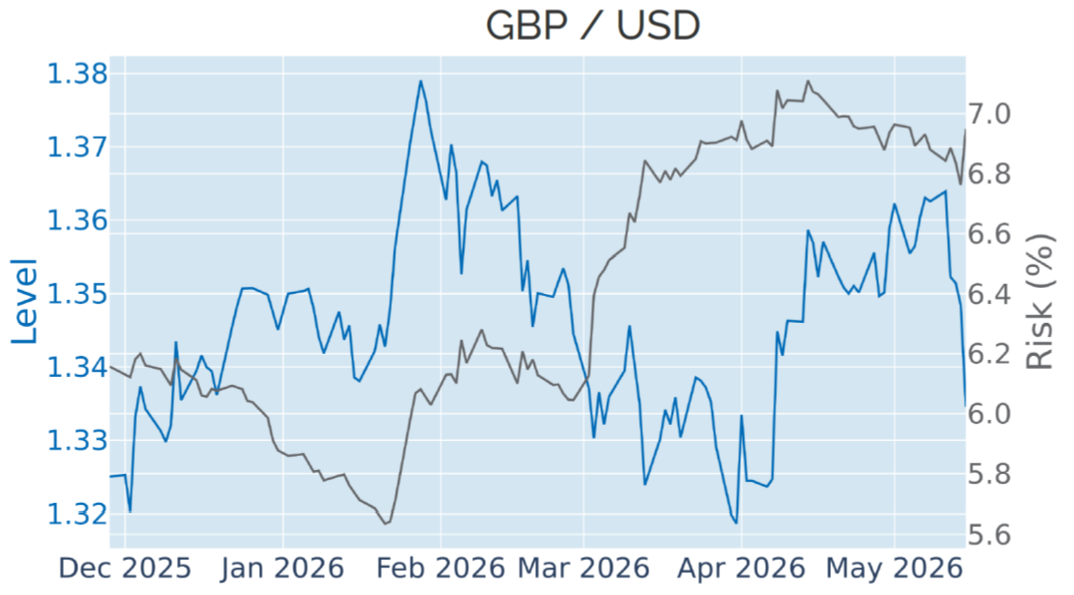

Gilt yields soar and pound weakens as UK political uncertainty persists

UK gilt yields moved higher alongside US Treasuries last week, while the pound fell to a five‑week low amid growing concerns about political stability. The 10‑year benchmark yield rose to its highest level since July 2007, as investors began to price the possibility that Andy Burnham could challenge Prime Minister Keir Starmer for the Labour leadership. Burnham is widely seen as more left‑leaning than Starmer, raising concerns about a potential loosening of the government’s fiscal stance.

Sterling also recorded its largest weekly decline against the US dollar in 30 months, although this needs to be viewed in the broader context of dollar strength driven by rising US interest rates. The last time the pound fell by more than 2% in a single week was in November 2024, when resurging inflation triggered a similar repricing of global monetary policy expectations.

Please refer to Figure 6 of the current Multi-Asset Class Risk Monitor (dated May 15, 2026) for further details.

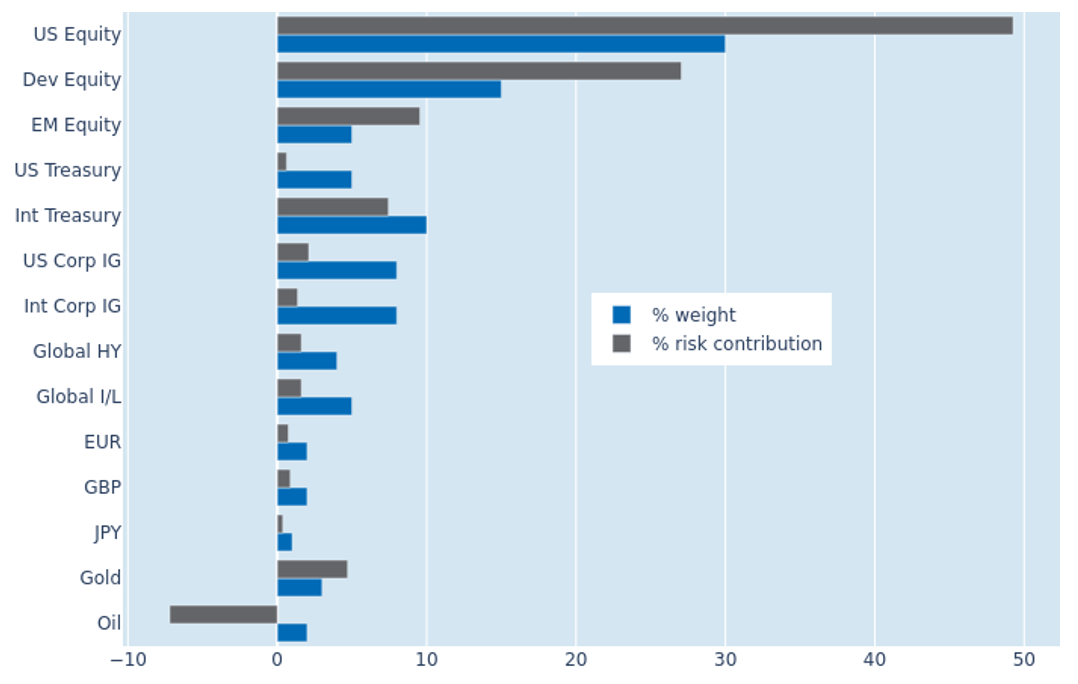

Lower FX and equity volatilities and correlations reduce portfolio risk

Predicted short‑term risk for the Axioma global multi‑asset class model portfolio declined by 1.3 percentage points to 8.1% as of Friday, May 15, 2026, reflecting a combination of lower equity volatility and a weaker relationship between equity returns and exchange rate movements against the US dollar. The latter effect primarily benefited non‑US developed equities, whose share of total portfolio risk declined from 27.6% to 27.0%. This was largely offset by a 0.7 percentage point increase in the contribution from US equities, even though their absolute risk level also fell. Risk contributions from other asset classes remained broadly unchanged, with only limited shifts in cross‑asset correlations.

Please refer to Figures 7-10 of the current Multi-Asset Class Risk Monitor (dated May 15, 2026) for further details.

You may also like

.png%3Fh%3D810%26iar%3D0%26w%3D1080&w=3840&q=75)