MULTI-ASSET CLASS MONITOR HIGHLIGHTS

WEEK ENDED MAY 22, 2026

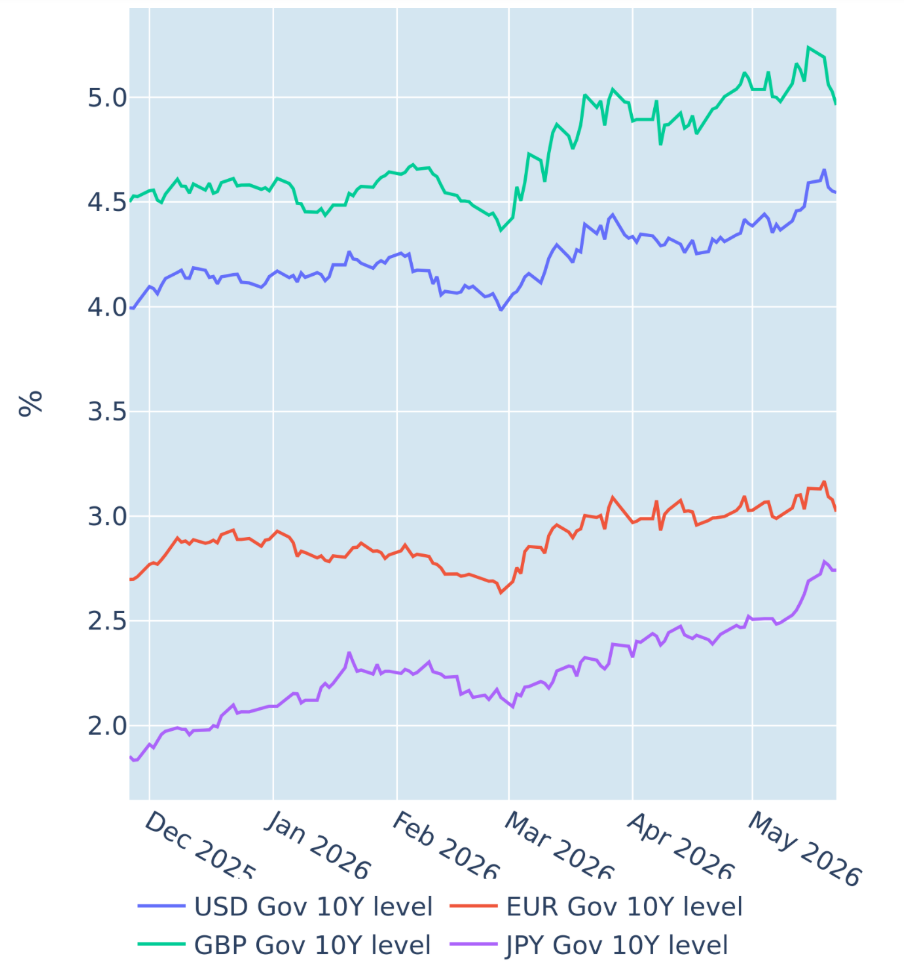

Gilts recover after downward inflation surprise

British government borrowing costs recorded their largest weekly decline in 29 months in the week ending May 22, 2026, following weaker-than-expected inflation data.

The Office for National Statistics reported on Wednesday that UK headline consumer prices rose by 2.8% in the twelve months to April, down from 3.3% the month before and well below analyst expectations of 3%. A decline had been widely anticipated, as the previous 12-month period still included last April’s sharp increase in prices, driven by tax and wage rises, as well as a higher government cap on household energy bills. By contrast, the energy price cap fell this April relative to the previous quarter. As it had been fixed at the end of February, shortly before the escalation of the Middle East conflict, this likely contributed to the larger-than-expected drop in inflation.

Short-term rate markets revised their policy expectations once more, pricing out a full rate hike by the Bank of England. The move propagated along the entire Gilt curve, with the 10-year yield falling 27 basis points — its largest weekly decline since December 2023. Roughly half of the move occurred immediately after Wednesday’s inflation release, with further support from easing oil prices and declining yields in other major government bond markets.

Gilts significantly outperformed German Bunds and US Treasuries, whose benchmark yields fell by 11 and 5 basis points, respectively. Political developments likely contributed to the additional volatility in UK rates. Over the past two weeks, markets have focused in particular on Andy Burnham — widely seen as a potential successor to Prime Minister Keir Starmer — at times treating him as a de facto next prime minister. The first week was dominated by concerns that a Burnham premiership could entail looser fiscal policy, pushing Gilt yields up by 26 basis points to near 19-year highs. However, those concerns eased the following Monday after his commitment to existing borrowing limits, helping drive last week’s equally sharp reversal. That said, a leadership challenge remains uncertain: Burnham would first need to win the Makerfield by-election in June before potentially triggering a leadership contest that could extend into the autumn.

Please refer to Figure 4 of the current Multi-Asset Class Risk Monitor (dated May 22, 2026) for further details.

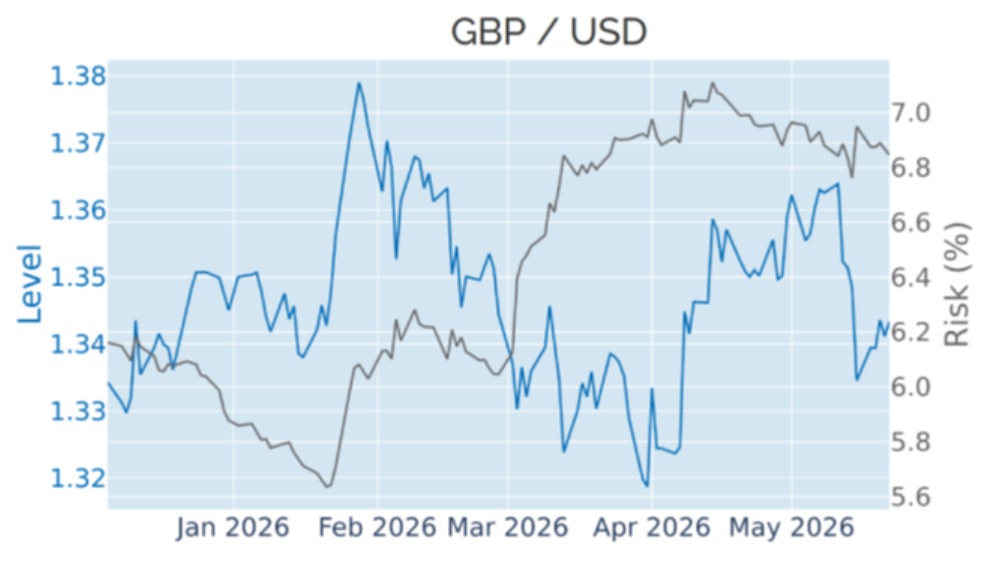

Sterling outperforms peers in UK-driven rebound

Sterling also recovered some of the previous week’s losses, albeit to a lesser extent than Gilts. It regained around 0.7% against the US dollar, following a 2.1% decline the week before. What stands out, however, is the pound’s relative performance. Sterling strengthened against most major currencies, including the euro and the yen, which both depreciated by around 0.3% against the dollar, while the Swiss franc was mostly flat.

This divergence is notable. In most circumstances, moves in exchange rates against the greenback are dominated by the USD leg of the relationship, with the other currencies largely moving in tandem, differing mainly in magnitude rather than direction. Last week’s price action deviated from that pattern, with sterling outperforming despite only a modest recovery against the dollar. This suggests that the adjustment was primarily driven by UK-specific factors — namely the downside inflation surprise, the associated repricing of Bank of England expectations, and evolving political developments — rather than a broader shift in global dollar dynamics.

Please refer to Figure 6 of the current Multi-Asset Class Risk Monitor (dated May 22, 2026) for further details.

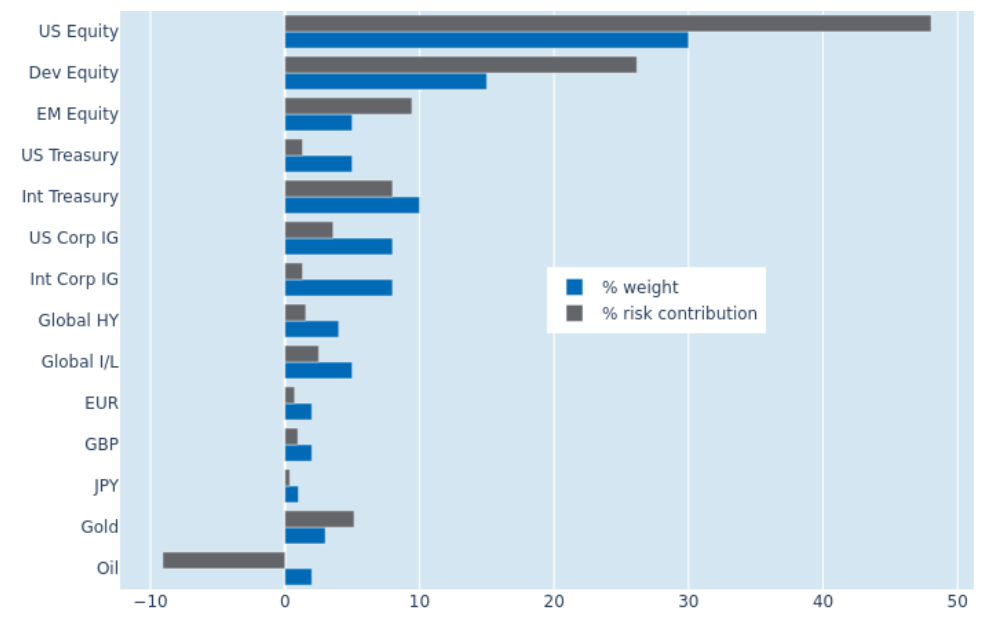

Joint stock-bond rebound lifts portfolio risk

Predicted short-term risk for the Axioma global multi-asset class model portfolio rose from 8.1% to 8.4% as of Friday, May 22, 2026, as global equity and bond markets recovered in tandem, supported by falling oil prices, easing inflation, and a downward revision in monetary policy expectations. The increase was most pronounced in USD investment grade corporate bonds, whose contribution to total portfolio risk rose from 2.1% to 3.5%. The risk contribution from US Treasury bonds also more than doubled, increasing from 0.6% to 1.3%.

Please refer to Figures 7-10 of the current Multi-Asset Class Risk Monitor (dated May 22, 2026) for further details.

You may also like

.png%3Fh%3D810%26iar%3D0%26w%3D1080&w=3840&q=75)