MULTI-ASSET CLASS MONITOR HIGHLIGHTS

WEEK ENDED MAY 29, 2026

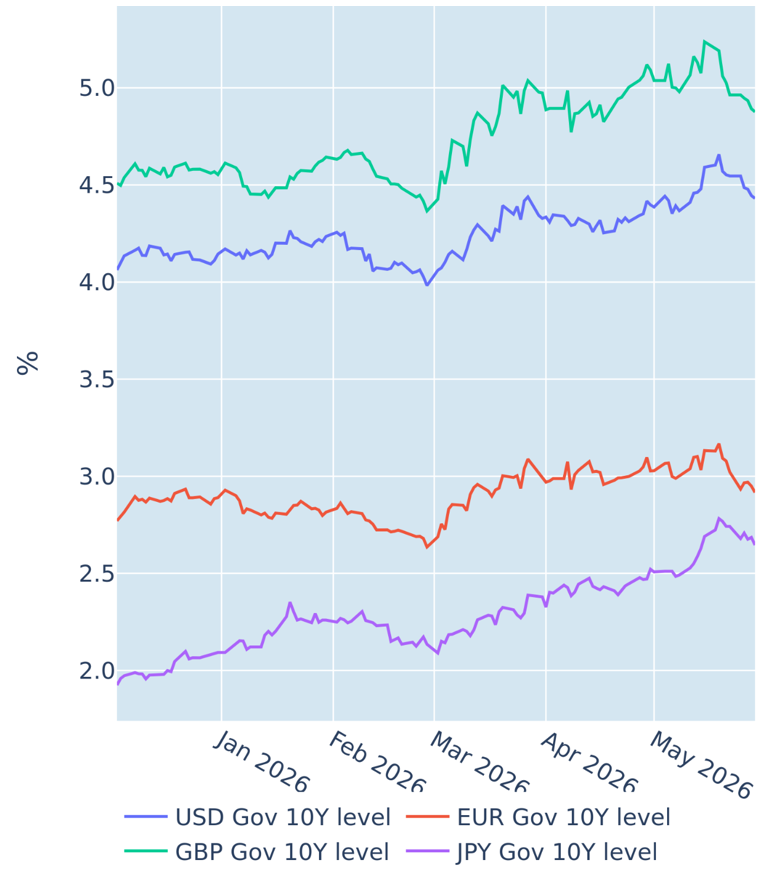

Falling energy prices pull Treasury yields lower

Global bond yields continued to fall in the week ending May 29, 2026, as oil prices eased amid signs that the US and Iran could be close to a deal. Crude dropped almost 10% last week, bringing the total monthly decline to 16% — the steepest fall since March 2020.

In response, the 10 year Treasury breakeven inflation rate, which is strongly positively correlated with energy costs, fell to its lowest level in more than five weeks, adding downward pressure on the corresponding nominal yield, which ended the week 11 basis points lower.

Declines were even more pronounced at the short end of the curve, with the monetary policy sensitive 2 year benchmark falling 15 basis points. This reflected a reassessment of the policy outlook, as traders lowered the implied probability of a Federal Reserve rate hike this year from 63% at the start of the week to roughly even odds by Friday.

Please refer to Figure 4 of the current Multi-Asset Class Risk Monitor (dated May 29, 2026) for further details.

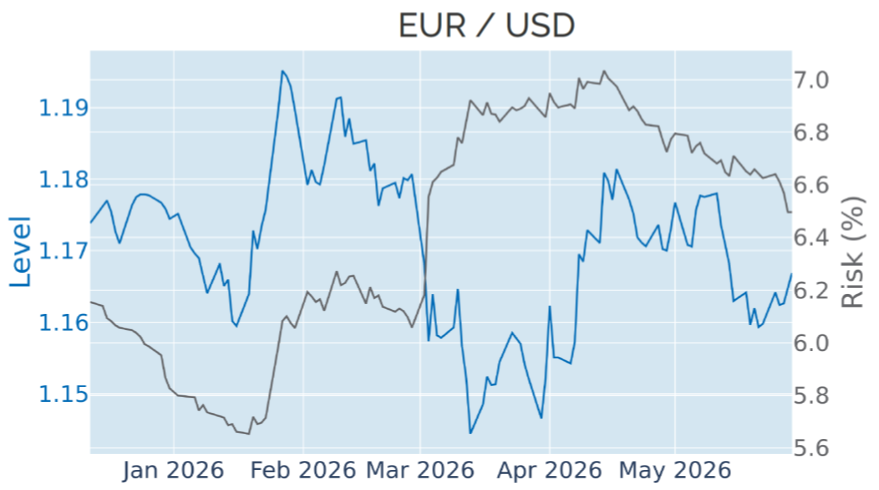

Dollar tracks decline in interest rates

Lower interest rates also weighed on the dollar, which weakened by 0.3% against a basket of major trading partners. The move reinforced the positive interaction between the greenback and Treasury yields that has prevailed since the Fed began its aggressive tightening cycle in June 2022.

That relationship briefly broke down during the capital flight from the US in the wake of “Liberation Day” in April 2025 and following Kevin Warsh’s nomination as the next Fed chair in January, when the dollar sold off even as long-term Treasury yields rose. But the co movement quickly re established itself, with both series moving in tandem in 13 of the last 16 weeks.

Please refer to Figure 6 of the current Multi-Asset Class Risk Monitor (dated May 29, 2026) for further details.

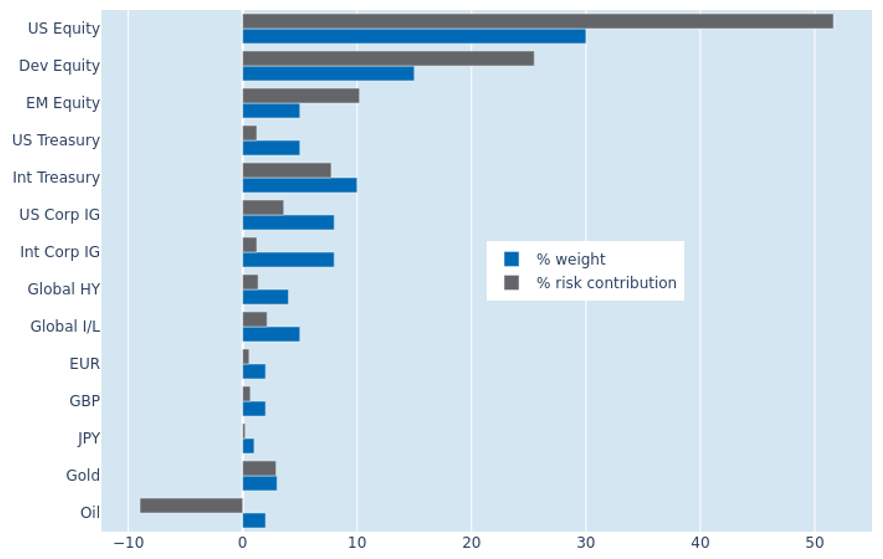

Ongoing equity rally pushes portfolio risk higher

Predicted short-term risk for the Axioma global multi-asset class model portfolio rose by another half percentage point to 8.9% as of Friday, May 29, 2026. The increase was most notable for US equities, whose share of total portfolio risk expanded by 3.6 percentage points to 51.6% after stock prices climbed for a ninth consecutive week.

This marks the longest weekly winning streak since the end of 2023, when easing inflation and the prospect of Fed rate cuts underpinned the rally — a stark contrast to the current environment, where inflation appears to be re accelerating and monetary policy risks are skewed to the upside.

The rise in equity risk was partly offset by a lower correlation with gold, whose contribution to overall portfolio risk declined from 5.1% to 2.9%.

Please refer to Figures 7-10 of the current Multi-Asset Class Risk Monitor (dated May 29, 2026) for further details.

You may also like

.png%3Fh%3D810%26iar%3D0%26w%3D1080&w=3840&q=75)