MULTI-ASSET CLASS MONITOR HIGHLIGHTS

WEEK ENDED JUNE 5, 2026

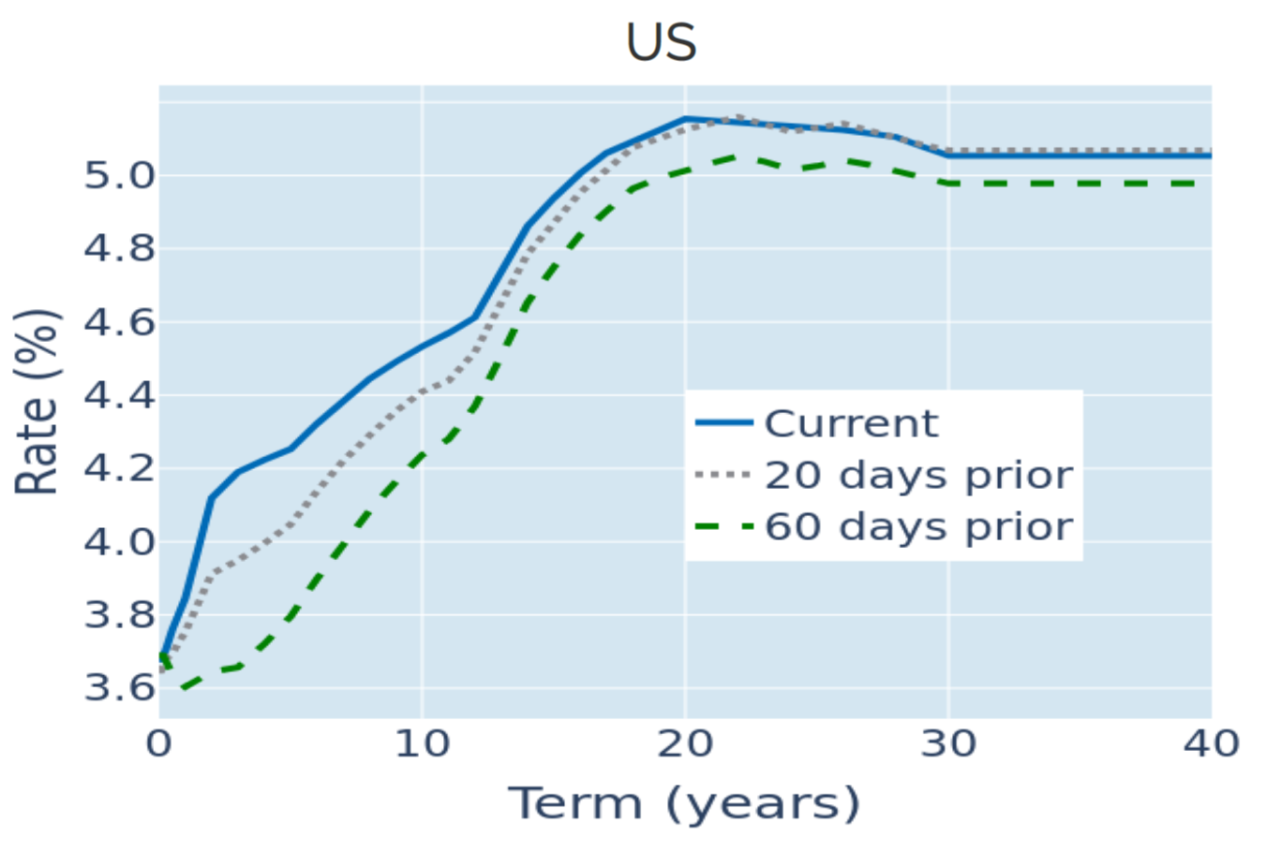

Strong payrolls push short-term yields to 15 month highs

A stronger-than-expected labor market report pushed short-term US borrowing costs to a 15 month high in the week ending June 5, 2026. The 2 year Treasury yield jumped 11 basis points on Friday after the Bureau of Labor Statistics reported that the economy added 172,000 jobs in May—more than double the 85,000 expected by analysts. Payrolls for March and April were also revised upward by a combined 93,000.

In response, fed funds futures traders again adjusted their outlook for monetary policy, lifting the implied probability of a rate hike this year from 45% to over 70%. The repricing extended across the curve: yields in the belly rose by 15–16 basis points, while long-end rates ended the week around 10 basis points higher.

Please refer to Figure 3 of the current Multi-Asset Class Risk Monitor (dated June 5, 2026) for further details.

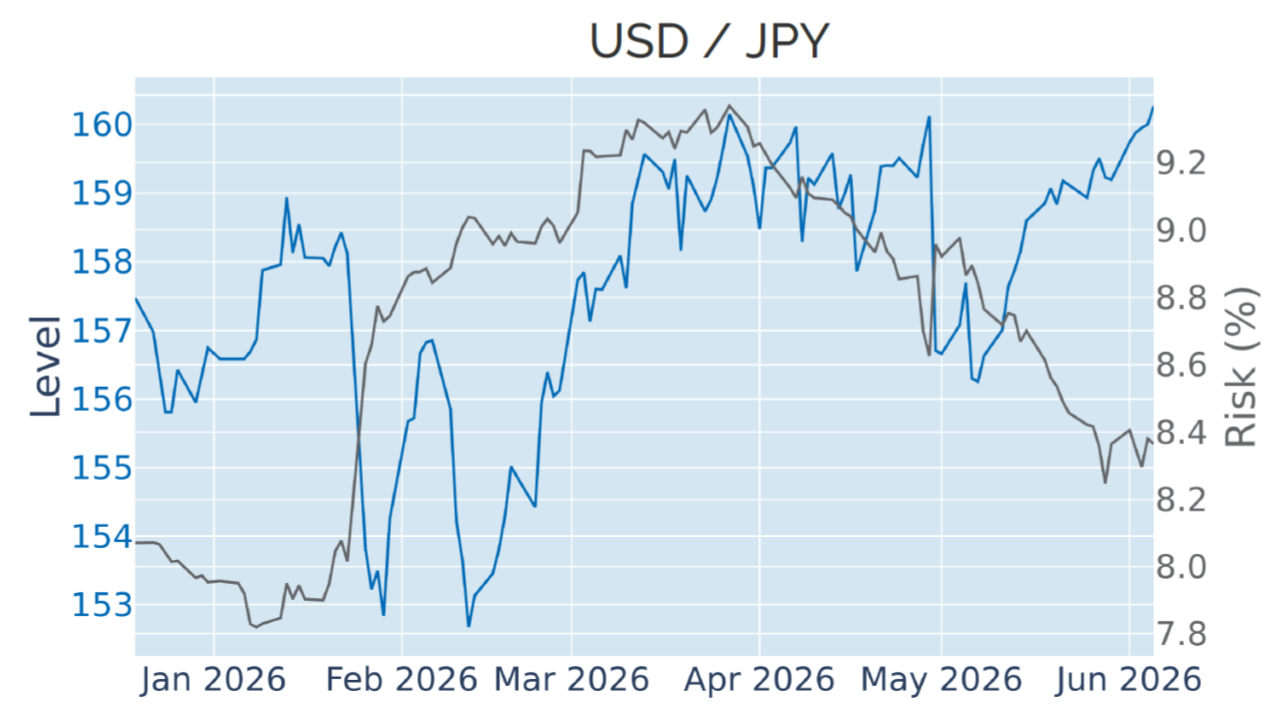

Renewed dollar strength pushes yen toward intervention threshold

The US dollar was once again the primary beneficiary of last week’s rise in rates. The Dollar Index gained 1.2%, climbing back above 100 for the first time since early April. As part of the move, the Japanese yen fell to its weakest level since July 2024, approaching the politically sensitive ¥160 mark, which in the past had triggered official intervention. Japanese authorities issued renewed warnings, reaffirming their readiness to respond and reserving their right to take “decisive action” against excessive volatility.

Please refer to Figure 6 of the current Multi-Asset Class Risk Monitor (dated June 5, 2026) for further details.

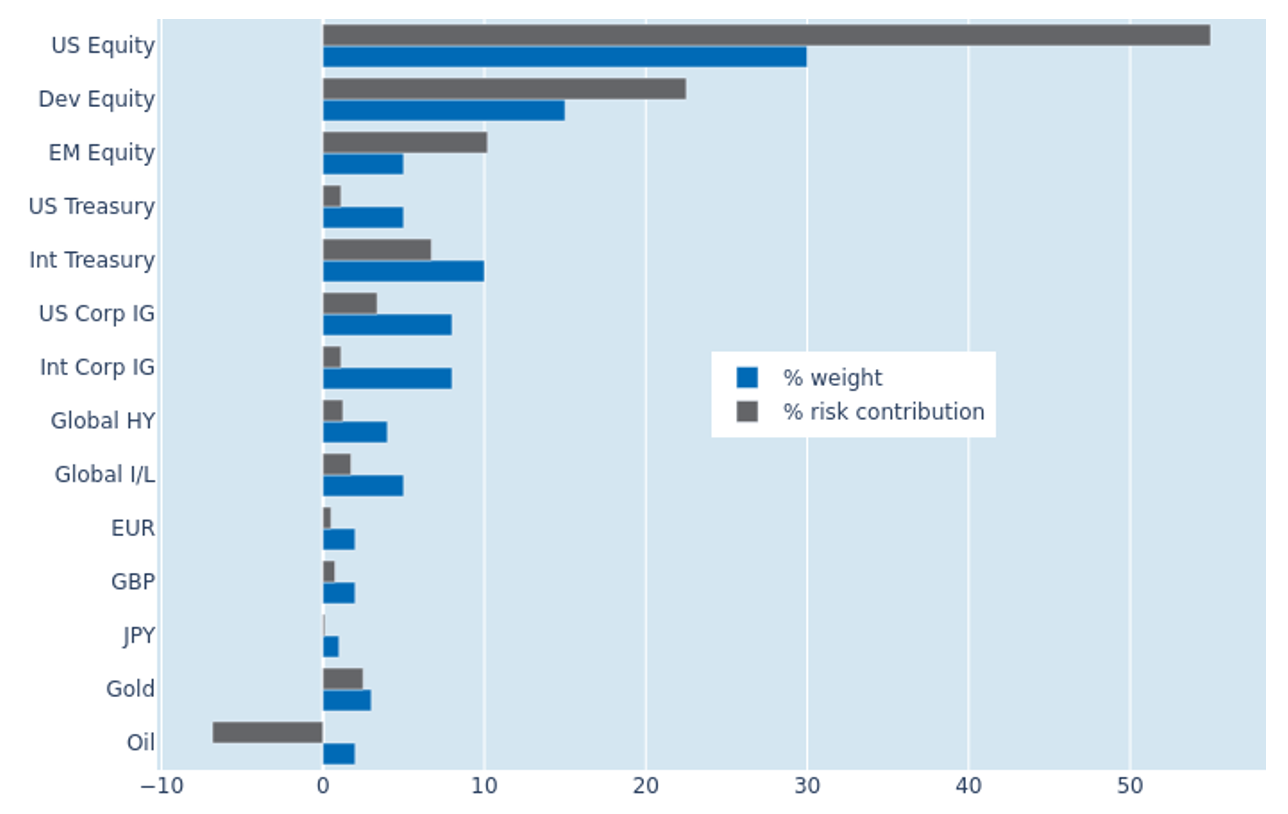

Lower equity volatility drives decline in portfolio risk

Predicted short-term risk for the Axioma global multi-asset class model portfolio eased from 8.9% to 8.0% as of Friday, June 5, 2026, largely reflecting lower equity volatility. The latter may appear somewhat counterintuitive, given that US stocks broke their nine week winning streak, but last week’s pullback meant that their standalone volatility actually declined. European and Japanese markets proved more resilient, resulting in weaker co-movement between local equity returns and their currencies against the dollar. As a result, developed non US equities saw the largest drop in their contribution to portfolio risk, falling from 25.5% to 22.5%. A similar dynamic benefited non USD government bonds, whose share of total volatility declined by 1.1 percentage points to 6.7%. Oil remained the only asset to reduce overall risk, although its diversifying effect diminished from -8.9% to 6.9%, as its correlation with US equities became less negative.

Please refer to Figures 7-10 of the current Multi-Asset Class Risk Monitor (dated June 5, 2026) for further details.

You may also like

.png%3Fh%3D810%26iar%3D0%26w%3D1080&w=3840&q=75)