MULTI-ASSET CLASS MONITOR HIGHLIGHTS

WEEK ENDED JUNE 12, 2026

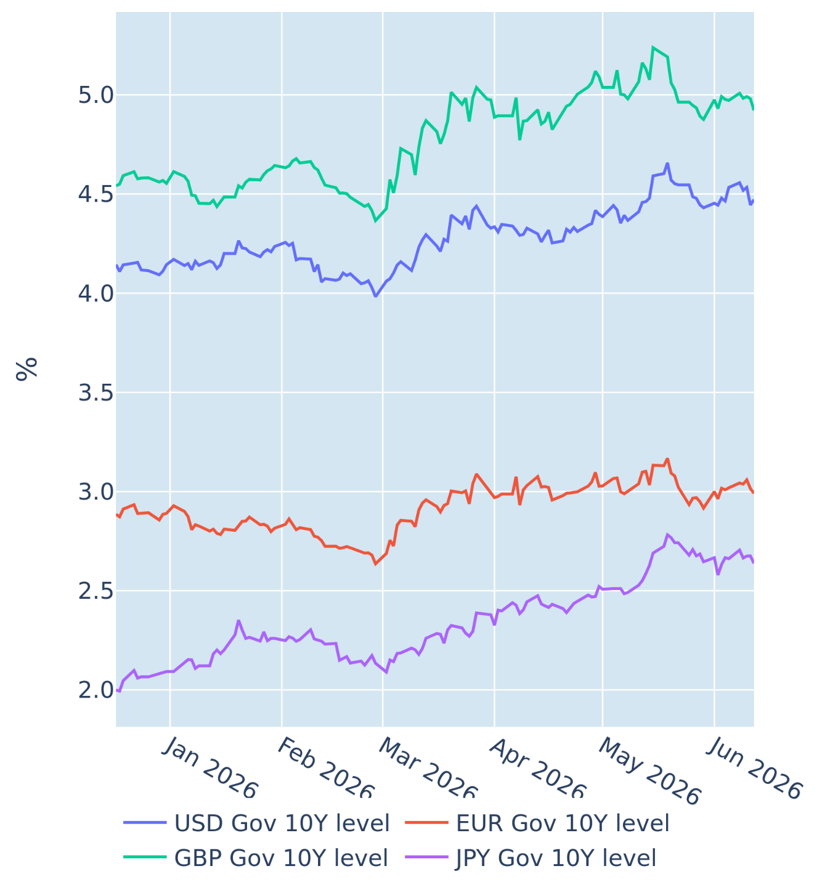

Global yields fall as geopolitics override economic data

Global bond yields eased again in the week ending June 12, 2026, as geopolitical developments overshadowed macroeconomic releases.

The Bureau of Labor Statistics reported on Wednesday that US headline inflation accelerated from 3.8% to 4.2% in May. Core prices rose more modestly to 2.9%, up only slightly from 2.8% in the previous month, as second-round effects from higher energy costs are still filtering through the wider economy. For comparison, in 2022, headline inflation peaked in June, while core inflation followed three months later.

The inflation data were widely anticipated, resulting in little immediate market reaction. Instead, Treasury yields declined by 8–10 basis points across most maturities on Thursday, amid renewed optimism that a deal between Iran and the US could be close.

UK gilt yields also ended the week significantly lower, although the main move occurred on Friday. Traders sharply revised their monetary policy expectations ahead of this week’s Monetary Policy Committee meeting. Governor Andrew Bailey had noted in recent weeks that the Bank of England could afford to take its time when considering next steps, as markets had already priced in a significant degree of monetary tightening.

That said, short-term interest rate derivatives markets priced out an entire rate hike between Wednesday and Friday, pushing the 2-year gilt yield down by nearly 10 basis points.

Please refer to Figure 4 of the current Multi-Asset Class Risk Monitor (dated June 12, 2026) for further details.

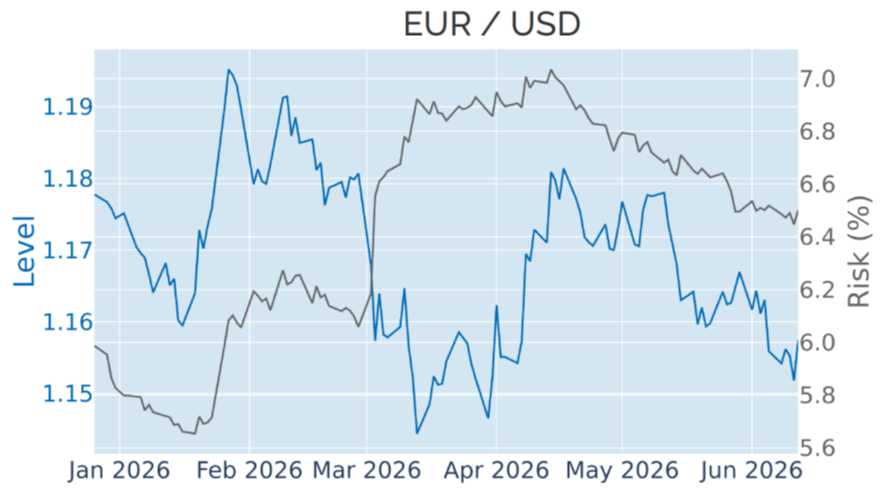

Euro is little moved despite ECB rate hike

The euro was little changed against most major trading partners in the week ending June 12, 2026, despite the European Central Bank becoming the first G7 central bank to tighten monetary policy in response to the Middle East energy shock last Thursday.

Like Wednesday’s US inflation data, the decision had been widely anticipated by market participants. The single currency depreciated by around 0.3% against the US dollar on the day of the announcement, consistent with its predominantly inverse relationship with interest rate differentials, but more than reversed the move on Friday, ending the week 0.1% higher.

Please refer to Figure 6 of the current Multi-Asset Class Risk Monitor (dated June 12, 2026) for further details.

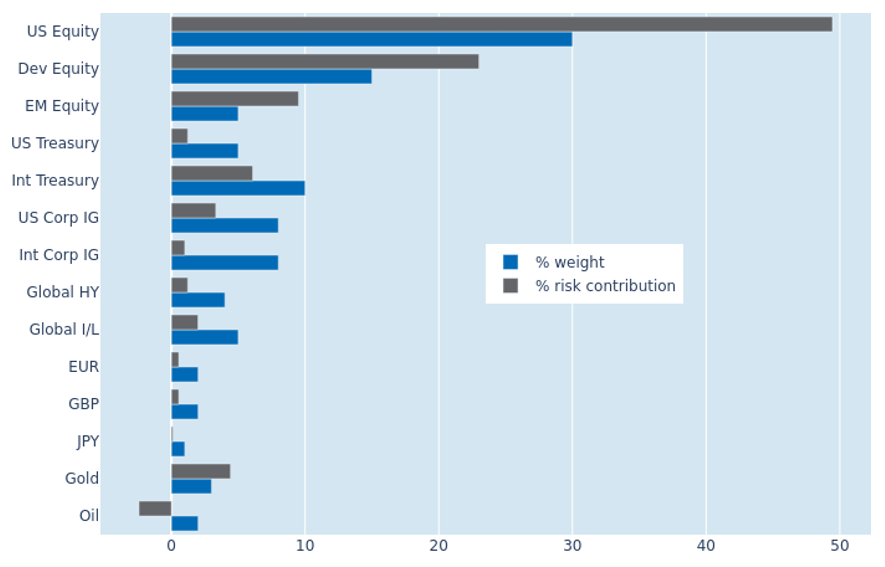

Commodity volatility lifts portfolio risk

Surging commodity volatility increased the predicted short-term risk of the Axioma global multi-asset class model portfolio by a full percentage point to 9% as of Friday, June 12, 2026, as the gold price fell to its lowest level in six months. As a result, the precious metal’s share of total portfolio risk rose from 2.5% to 4.4%. Its inverse relationship with the US dollar also made gold appear more positively correlated with non-USD assets, with developed equities seeing their percentage risk contribution increase by half a percentage point to 23%. Oil, meanwhile, had its risk-reducing effect curtailed from -6.9% to -2.4%, reflecting a less negative correlation with other asset classes in the portfolio.

Please refer to Figures 7-10 of the current Multi-Asset Class Risk Monitor (dated June 12, 2026) for further details.

You may also like