MULTI-ASSET CLASS MONITOR HIGHLIGHTS

WEEK ENDED JULY 3, 2026

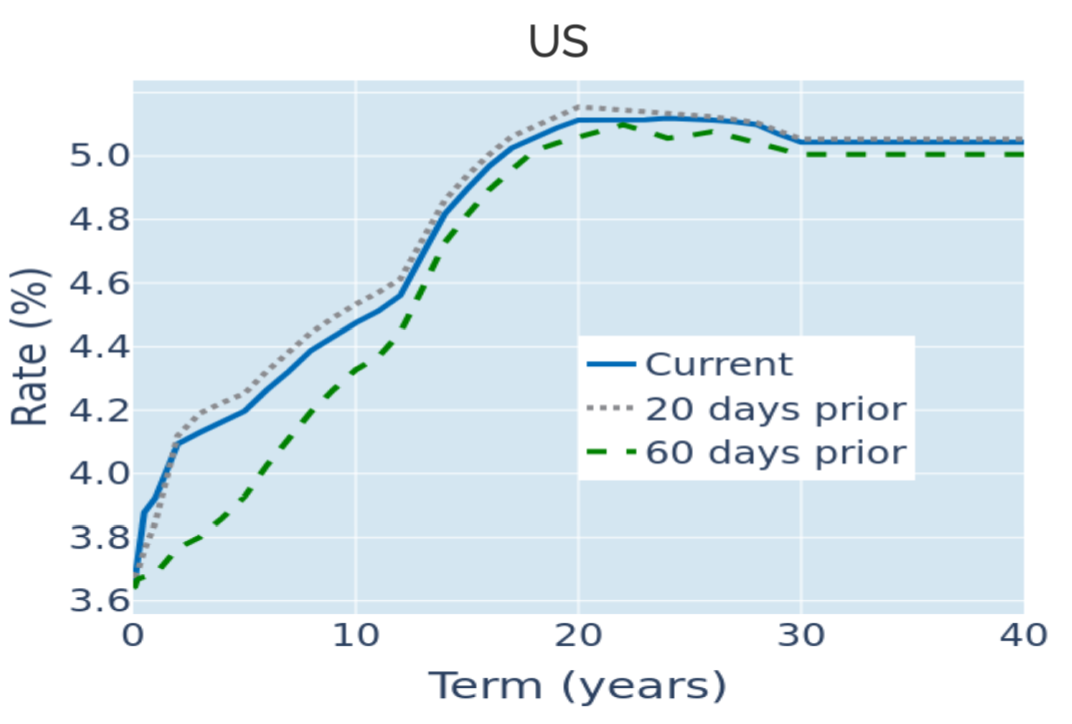

Treasury curve re-steepens as short end whipsaws on conflicting labor data

The US Treasury curve steepened in the week ending July 3, 2026, as short yields whipsawed on the back of conflicting labor market signals, while longer borrowing rates pushed higher throughout.

The 2-year yield rose 3 basis points on Monday and a further 4 basis points on Tuesday, as a stronger-than-expected JOLTS — May job openings came in at 7.6 million versus the 7.3 million expected — reinforced the view of continued labor market resilience. The move extended by another 3 basis points on Wednesday, bringing the cumulative rise to 10 basis points, as Fed Chair Kevin Warsh's comment that "prices are too high" at the European Central Bank forum outweighed a soft ADP report showing just 98,000 private jobs added in June, below the 113,000 forecast. The gains were then partly reversed on Thursday, when the June nonfarm payrolls showed just 57,000 jobs added — roughly half the consensus estimate — pulling the 2-year yield back by 3 basis points and leaving it 7 basis points higher for the week.

This was in contrast to the 10-year benchmark, which climbed steadily throughout the week without giving back any of its gains, closing 11 basis points higher compared with the previous Friday.

Please refer to Figure 3 of the current Multi-Asset Class Risk Monitor (dated July 2, 2026) for further details.

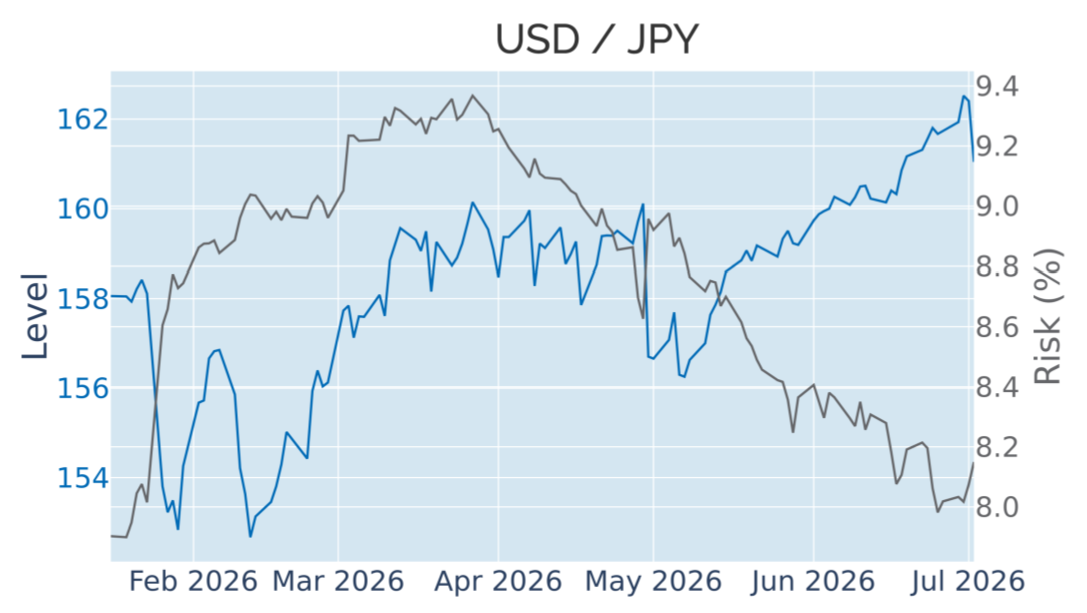

Yen touches a 40-year low before a late-week dollar stumble lifts it into the black

The Japanese yen fell to its weakest level against the dollar since 1986 on Tuesday, edging past ¥162, as the persistent gap between US and Japanese rates continued to weigh on the currency. Speculation mounted over possible intervention by Japanese authorities, with Finance Minister Satsuki Katayama repeating that officials stood ready to act "at any time if needed" — but no intervention was confirmed, and traders remained skeptical that any action would provide more than temporary relief.

The currency nonetheless recovered to end the week higher, as broad-based dollar weakness set in from Thursday onward following the weaker-than-expected June payrolls report, which prompted traders to scale back Fed rate-hike expectations.

Please refer to Figure 6 of the current Multi-Asset Class Risk Monitor (dated July 2, 2026) for further details.

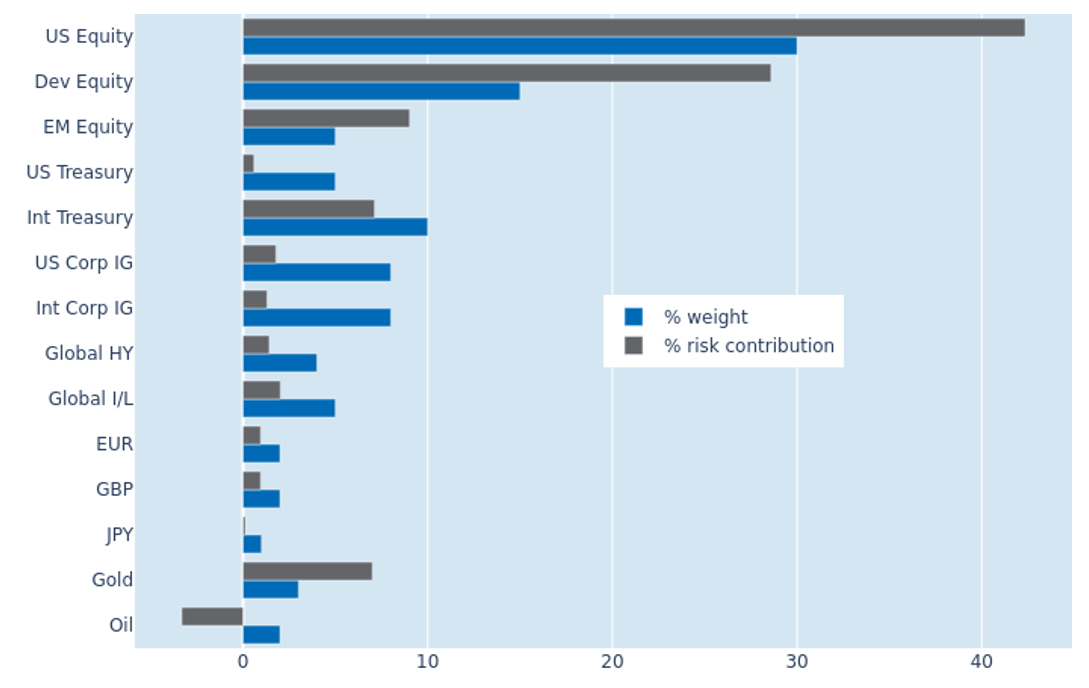

Lower equity volatility and weaker stock-bond correlation reduce portfolio risk

Predicted short-term risk for the Axioma global multi-asset class model portfolio eased from 8.8% to 8.4% as of Thursday, July 2, 2026, primarily reflecting a decline in stock market volatility. US equities benefited most from the move, with their share of total portfolio risk falling from 46.9% to 42.4%. A weaker relationship between stock and bond returns added to the decline, as the two asset classes' recent tendency to move in tandem became noticeably less pronounced over the week. Non-US developed equities moved against the broader trend, however, with their share of total portfolio risk expanding by 6.8 percentage points to 28.6%. This likely reflects the positive correlation between currency and equity returns, which meant that continued FX volatility added to the overall risk profile of internationally exposed equities even as pure equity risk eased elsewhere. The rest of the portfolio was largely unchanged, with correlations across other asset classes remaining broadly stable.

Please refer to Figures 7-10 of the current Multi-Asset Class Risk Monitor (dated July 2, 2026) for further details.

You may also like