Exposing AI risk in credit portfolios

Author

Saboor Zahir

Senior Director, Solutions Engineering

AI disruption is creating idiosyncratic credit risks that sector-level analysis alone can't capture. This article shows how combining issuer-level stress testing with factor-based models reveals which names in your portfolio are most exposed to an AI reversal — and how to position accordingly before losses materialize.

Why looking at industries may not be enough

Not all names in an industry are affected equally by AI exposure – issuer-level granularity allows for more precise differentiation than a purely systematic approach.

Credit markets have begun repricing AI-related risks, and investor fears run in two directions. First, the ease of replicating established software-as-a-service (SaaS) products has cast doubt on the once-stable cashflows those businesses were assumed to generate. Second, markets worry that meeting AI demand will require material capital expenditure, driving companies to take on more debt.

In this article, we consider two key principles that debt is evaluated on:

- Probability of Default: how likely am I to get my money back or how likely is the issuer able to service its debt?

- Loss Given Default: if the issuer cannot pay off its debts, what’s left to salvage?

Investors are rethinking this at the industry level and that divergence is already visible at this level. Software credits spreads have re-priced materially relative to hardware, where physical assets on the balance sheet provide a cushion that pure-software balance sheets lack. But industry-level analysis only tells part of the story. In what follows, we examine how practitioners can identify which specific names in their portfolio are most exposed — and how to stress test that exposure rigorously.

Exhibit 1: Divergence in OAS Software BB1 USD and Hardware BB1 USD

Source: Axioma Spread Curves

Dark blue = Software BB1 USD / Light Blue = Hardware BB1 USD

Exhibit 2: Five-year point on Oracle Axioma Issuer Spread Curve since OpenAI deal announcement

Source: Axioma Spread Curves

AI stress test methodology

Understanding exposure to AI at the issuer level is key and stress testing offers a way to surface issuer-level risks in the portfolio. Traditional risk factor approaches in credit rely on sector or industry exposures, potentially missing issuer level risks to AI that are specific to their businesses. We highlight this by contrasting stress testing results using the Axioma Granular Spread Model (GR) and Axioma Credit Spread Factor Model (CSFM). The GR model leverages issuer level curves with full term structure to assess risk. On the other hand, the CSFM model is a factor-based approach that captures systematic risk through DTS factors across currency, rating, sector/industry, and region/country.

How to construct scenarios

Where two credit models diverge: Software & Services

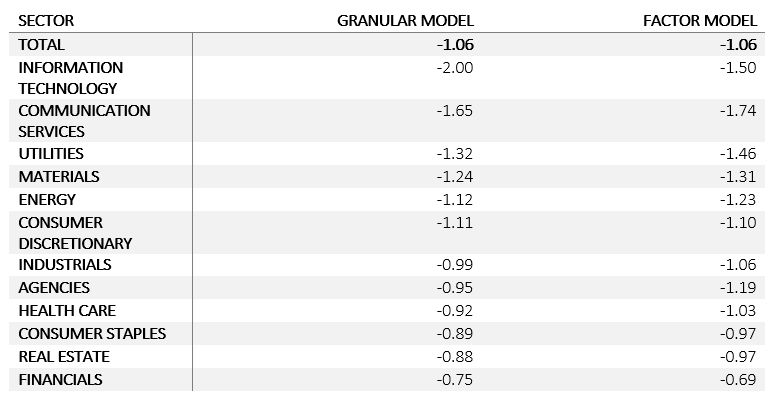

The stress tests were run both using the granular and factor-based models. At first glance, the top line returns for the portfolio look similar. The sector level results also look comparable with the exception of Information Technology.

Exhibit 3: Returns at the sector level – Axioma Granular Model vs Axioma Credit Spread Factor Model

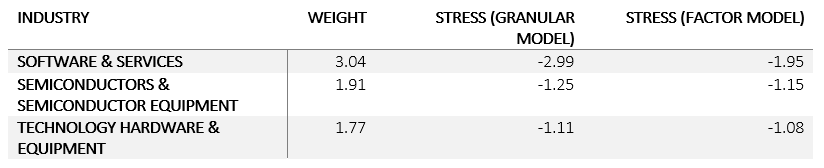

Exhibit 4: Tech sector analysis

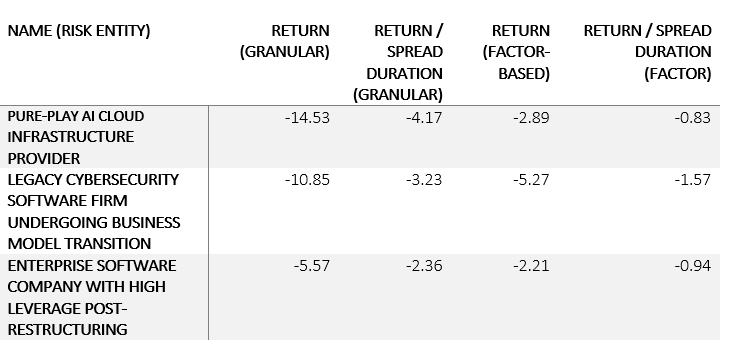

Digging into the Tech sector further, we can find that the losses are concentrated in Software companies (Exhibit 4). And as we look further into the software industry, we can see the entities that are most exposed to the AI reversal event (Exhibit 5). Below we show the results both in returns and return normalized by spread duration to account for spread sensitivity.

Exhibit 5: Return results normalized by spread duration

The factor-based model underestimates the name level risk for key names exposed to AI-reversal. For example, consider the pure-play AI cloud infrastructure provider above whose business is completely tied to the AI boom. The granular model captures this idiosyncratic risk more precisely than the sector-wide factor approach.

A better way to stress test AI exposure in fixed income

AI disruption is creating idiosyncratic business level risks that systematic models may not fully capture on their own. In periods of elevated uncertainty, capturing issuer-level granularity is key to assessing company-level risk exposures.

Want to see the full issuer-level results? Contact us to get the complete analysis.

FAQs

FAQs

Q: How do I stress test AI exposure in a credit portfolio?

Apply a shock to an AI thematic equity basket and use a predictive, transitive stress test to propagate the impact across your portfolio. Calibrate correlations over a recent window using exponential decay weighting and use issuer-level spread curves rather than sector factors alone to capture idiosyncratic name-level risk.

FAQs

Q: Why does sector-level analysis underestimate AI risk in credit portfolios?

Sector and industry classifications group issuers that can have very different business exposures to AI. A factor-based model applies systematic risk uniformly across a sector, missing the dispersion between names. Issuer-level granularity captures this.

FAQs

Q: What is the difference between the Axioma Granular Model and the Credit Spread Factor Model for stress testing?

The Granular Model uses issuer-level spread curves with full term structure, capturing idiosyncratic risk at the name level. The Credit Spread Factor Model is a systematic, factor-based approach using DTS factors across rating, sector, currency and region. In an AI stress test scenario, the two models produce similar top-line results but diverge significantly at the issuer level, particularly within Software & Services.

Relevant articles