MULTI-ASSET CLASS MONITOR HIGHLIGHTS

WEEK ENDED JULY 10, 2026

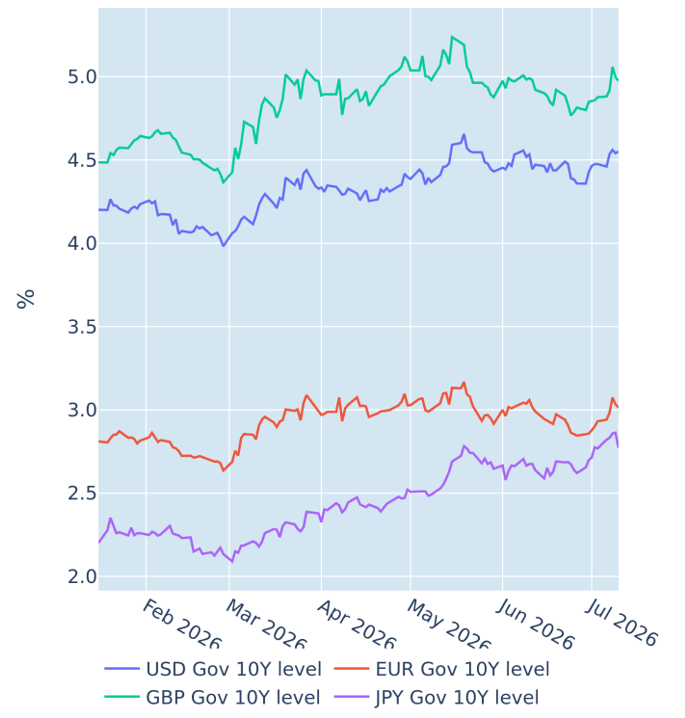

Middle East re-escalation drives global yields higher for a second week

Global bond yields climbed for a second consecutive week in the week ending July 10, 2026, as a renewed escalation in the Middle East reignited concerns over energy supply disruptions and reinforced the inflation risk premium embedded in global rates.

Gilts underperformed their peers, with the 10-year borrowing rate rising 10 basis points on the week, compared with 8 basis points each for the corresponding German Bund and US Treasury benchmarks. The moves were far from linear, though, and the regional split in timing looks largely mechanical rather than a genuine divergence in views. Long-term Treasury yields rose 7 basis points on Tuesday, with much of that move unfolding in the US afternoon, after Iranian forces attacked three commercial vessels in the Strait of Hormuz and Washington responded by revoking a sanctions waiver on Iranian oil exports late in the session. European yields therefore had little chance to react until the following day, with Bunds up 9 basis points and Gilts up 14 basis points on Wednesday, as European markets caught up with news that had already been digested in the US the day before.

Some of these gains were unwound again on Thursday, as oil prices eased once more on reports that Washington and Tehran were continuing technical talks despite the renewed fighting, tempering fears that the latest escalation would translate into a prolonged disruption to Gulf shipping.

The bond market selloff was accompanied by a renewed repricing of monetary policy expectations across major currency areas. On Wednesday, the 1-year SONIA forward rate climbed above 4.25%, implying two Bank of England rate hikes over the next 12 months. The futures-implied 3-month Euribor rate for December rose to 2.715%, similarly pointing to almost two more rate increases from the ECB before the end of the year. In the US, fed funds futures raised the implied probability of at least one rate hike this year from 78% to over 85% over the course of the week, with markets assigning a 70% chance that the move could come as early as September. The minutes of the June FOMC meeting, also released on Wednesday, may have reinforced that hawkish repricing, revealing that a few officials saw a case for raising rates immediately and that the committee remained evenly split on where rates should stand by year-end.

Please refer to Figure 4 of the current Multi-Asset Class Risk Monitor (dated July 10, 2026) for further details.

Sterling tracks UK rates higher as the yen slides to a 40-year low

Currency markets were considerably more muted last week, with most G10 pairs moving by less than half a percent against the dollar and no clear directional theme emerging. That said, two moves stood out. Sterling ended the week 0.4% stronger against the dollar, marking the third consecutive week in which the pound has moved in the same direction as UK interest rates and Gilt yields.

The Japanese yen, by contrast, fell to another 40-year low on Wednesday, its weakest level against the dollar since December 1986, as renewed concerns over Japan's fiscal trajectory lifted long-term JGB yields to multi-decade highs. The government's draft long-term economic strategy, which calls for more than ¥370 trillion in public and private investment through fiscal 2040 across 17 priority sectors, stoked worries about additional debt issuance, helping to push the 10-year JGB yield to a fresh 30-year high on Thursday. Those fiscal concerns were only partly offset by remarks from Finance Minister Satsuki Katayama, who indicated that the government would encourage the country's public pension funds to raise their holdings of domestic assets.

Please refer to Figure 6 of the current Multi-Asset Class Risk Monitor (dated July 10, 2026) for further details.

Portfolio risk plummets as equity volatility declines

Predicted short-term risk for the Axioma global multi-asset class model portfolio plummeted from 8.4% to 7.5% as of Friday, July 10, 2026, primarily reflecting a decline in standalone equity volatility, which accounted for roughly two-thirds of the overall reduction in risk. Non-US developed and emerging market stocks were the major beneficiaries, with their combined share of total risk shrinking from 37.7% to 36.9%, thanks to a slightly lower correlation with their American counterparts. Oil continued to act as the portfolio's principal diversifier, with its risk-reducing contribution deepening from -3.3% to -4.0%. This was partly driven by a decrease in its own volatility and partly by a more negative correlation with fixed income assets.

Please refer to Figures 7-10 of the current Multi-Asset Class Risk Monitor (dated July 10, 2026) for further details.

You may also like