MULTI-ASSET CLASS MONITOR HIGHLIGHTS

WEEK ENDED MARCH 13, 2026

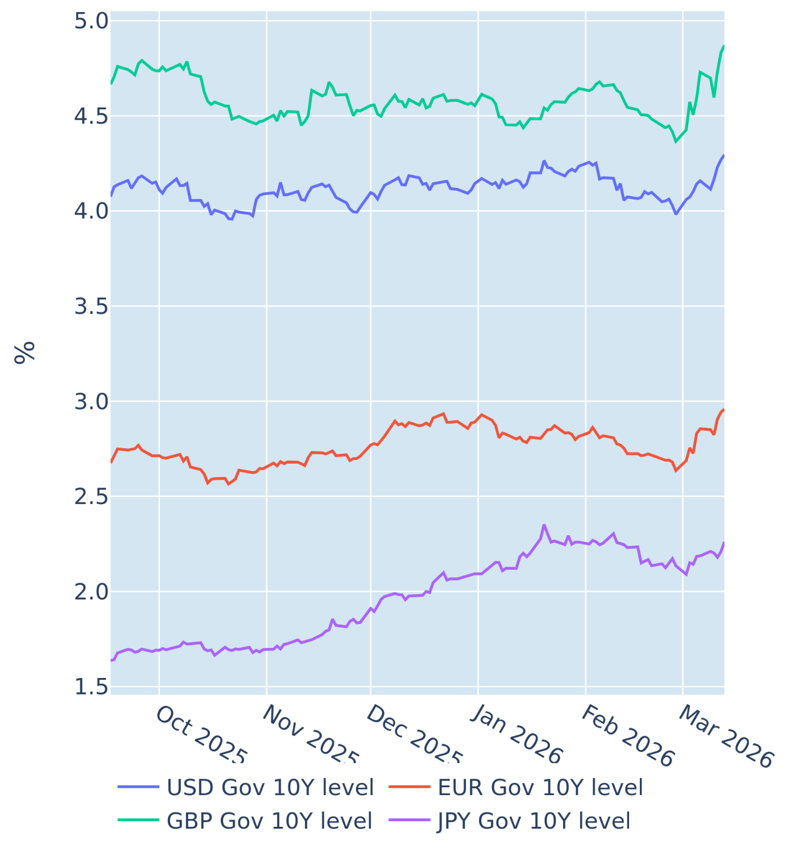

Ongoing increases in inflation and monetary policy expectations keep boosting bond yields

A further increase in inflation and monetary-policy expectations boosted global borrowing costs to their highest levels in months and years in the week ending March 13, 2026.

US Treasury yields kept rising across all maturities to a six-month high, as traders continued to price out anticipated rate cuts. Futures markets now imply only a 60% chance that the Federal Reserve will relax monetary conditions just one more time toward the end of this year, compared with 50 basis points worth of easing priced in before the start of the Iran conflict. The monetary policy-sensitive 2-year rate climbed another 17 basis points as a result, while the 10-year benchmark ended the week 0.13% higher, pushed up by a 3-basis point increase in the corresponding breakeven inflation rate.

On the other side of the Atlantic, market participants solidified their expectations that central banks will tighten the monetary screws in response to the anticipated inflationary impact of the ongoing oil price and supply shock. The Bank of England is now firmly expected to raise its base rate at some point in the next 12 months, pushing Gilt yields to their highest levels in more than a year. The 10-year German Bund yield even soared to an almost 15-year high, with the European Central Bank projected to raise its deposit rate by half a percentage point before the year is out.

Please refer to Figure 4 of the current Multi-Asset Class Risk Monitor (dated March 13, 2026) for further details.

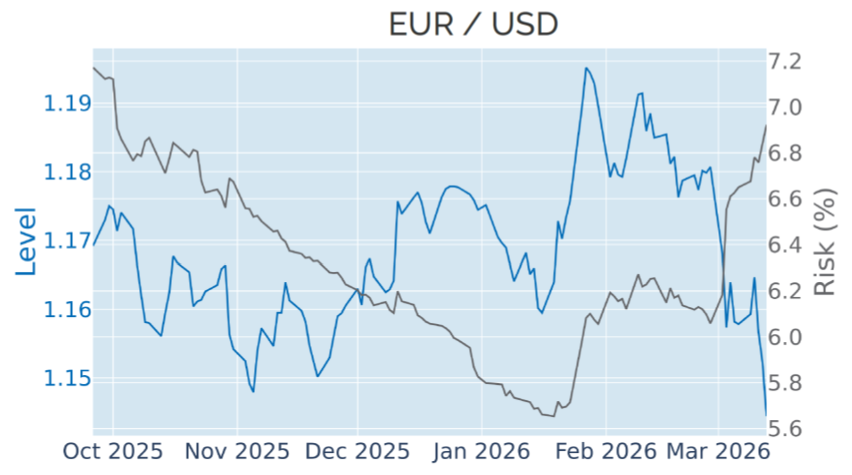

And the dollar is once again the sole beneficiary

The dollar was once again the sole beneficiary of last week’s surge in global yields, gaining 1.4% against a basket of major trading partners for the second week in a row. The move boosted the Dollar Index to its highest level since May 2025, up 4.3% from its most recent low at the end of January. The euro ended the week 1.2% weaker at a nine-month low just below $1.15, despite the significant rate increases and monetary-policy revisions in the single-currency area, while the Japanese yen depreciated to its cheapest level against its American rival since July 2024.

Please refer to Figure 6 of the current Multi-Asset Class Risk Monitor (dated March 13, 2026) for further details.

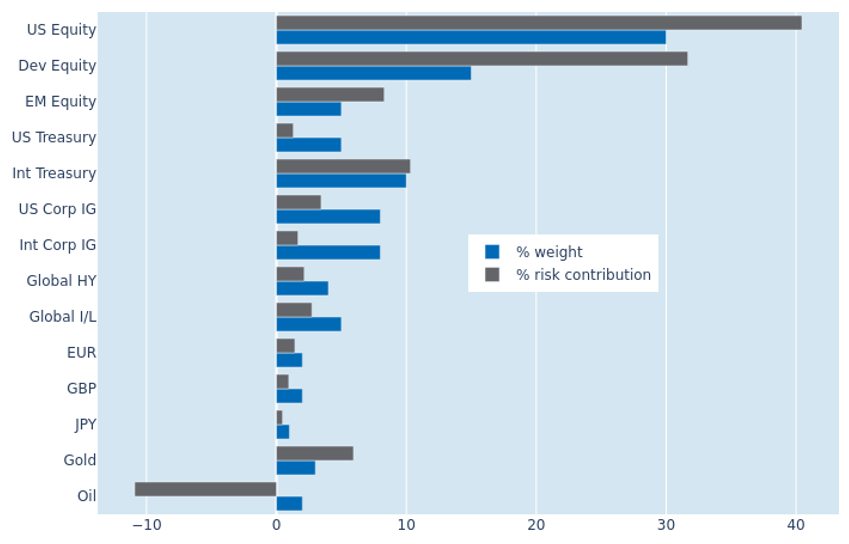

Portfolio risk eases as oil price surge offsets equity, bond, and FX losses

The predicted short-term risk of the Axioma global multi-asset class model portfolio eased slightly from 8.7% to 8.4% as of Friday, March 13, 2026, as the adverse effects of higher stock and bond market volatilities were more than outweighed by a more inverse relationship of both asset classes with oil prices. Thanks to its negative correlation with all other security types in the portfolio, oil became the biggest source of risk reduction in the portfolio, almost doubling its negative contribution from -6.3% to -10.9%. Combining the black commodity with non-US equities yielded the greatest diversification benefits, as the strong gains of the former balanced out not only local stock market losses but also weaker exchange rates against the dollar. US shares also profited to some extent from the inverse interaction, but a strong increase in their standalone volatility still meant that their percentage risk contribution expanded by 8.4% to 40.5%.

Please refer to Figures 7-10 of the current Multi-Asset Class Risk Monitor (dated March 13, 2026) for further details.

You may also like