MULTI-ASSET CLASS MONITOR HIGHLIGHTS

WEEK ENDED MARCH 20, 2026

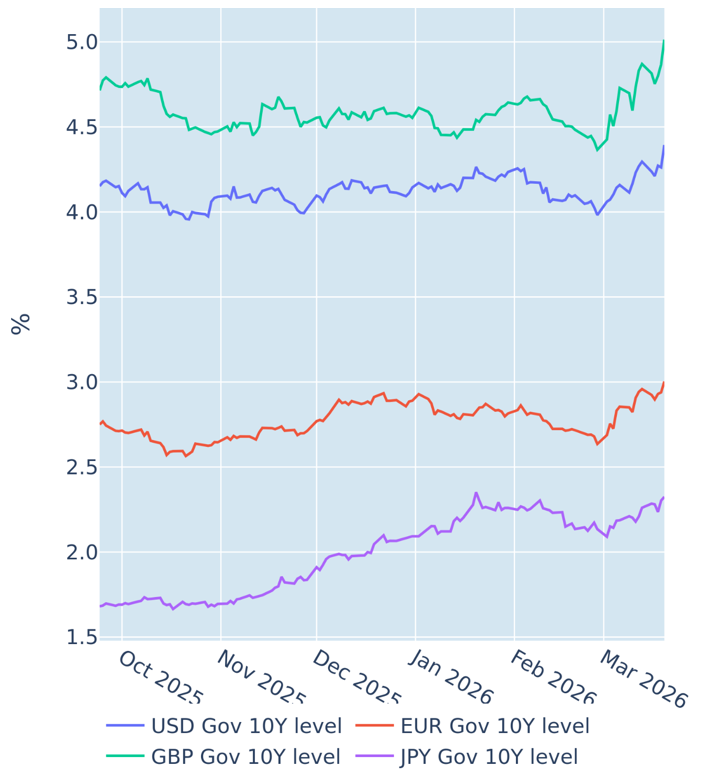

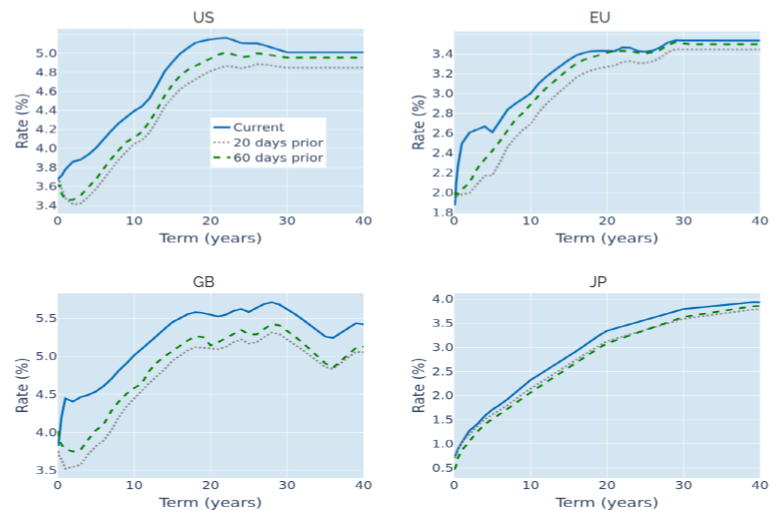

Global yields continue to soar as central banks quash rate cut hopes

Global borrowing costs extended their sharp rise in the week ending March 20, 2026, as all major central banks quashed all remaining hopes of monetary easing, underscoring renewed inflation risks instead. The Federal Reserve held rates steady in line with market expectations on Wednesday, but revised its inflation projections higher, explicitly linking the shift to surging oil prices and Middle East supply disruptions. On the following day, the European Central Bank struck a similar tone in its monetary policy announcement, warning that the war‑driven energy shock created “upside risks for inflation.” The Bank of England specifically highlighted the potential second‑round effects “through wage and price-setting” and stressed that all MPC members “stood ready to act as necessary to ensure that CPI inflation remained on track to meet the 2% target in the medium term.” The Bank of Japan also noted the need for special attention toward “the impact of the rise in crude oil prices on the outlook for underlying CPI inflation.”

The respective yield curves all reacted with a “bearish flattening,” as the renewed upward revision in monetary policy expectations pushed short rates up even further, while higher inflation projections buoyed long yields. But the scale of the selloff varied greatly across regions. With the Fed no longer expected to cut rates this year, the monetary policy-sensitive 2-year Treasury yield climbed another 15 basis points, while the 10-year benchmark ended the week 0.11% higher. The pivot was stronger in the Eurozone, where long Bund yields were only marginally higher, whereas the short end soared by more than 20 basis points, as traders priced in at least three rate hikes from the ECB before the year is out.

But it was the UK which experienced by far the biggest increase in borrowing costs. The country already had the highest inflation and interest rates among the G7 economies before the onset of the conflict, which gives both the BoE and the government even less flexibility to deal the latest crisis. Since the start of this month, the 2-year Gilt yield has risen a full percentage point—similar to what happened in the ‘mini-budget’ crisis in 2022—while the 10-year borrowing rate climbed above 5% for the first time since 2008.

Please refer to Figures 3 & 4 of the current Multi-Asset Class Risk Monitor (dated March 20, 2026) for further details.

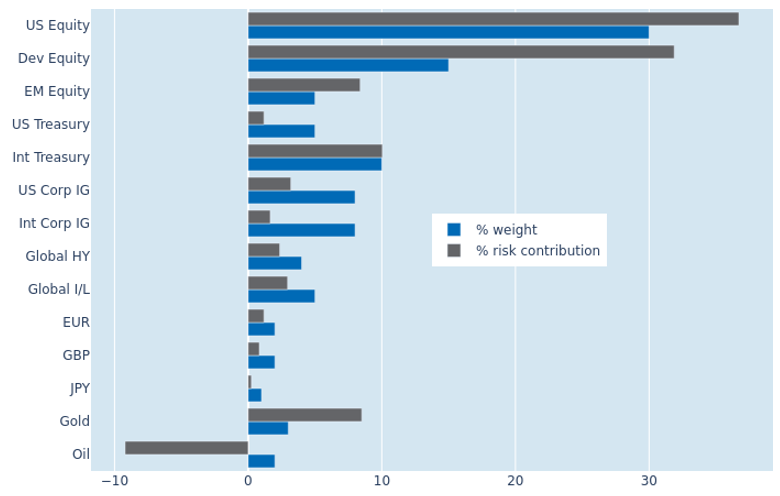

Portfolio risk remains stable as commodity contributions diverge

The predicted short‑term risk of the Axioma global multi‑asset model portfolio remained broadly stable at around 8.5% on Friday, March 20, 2026. Lower standalone volatility in US equities reduced their contribution to overall risk from 40.5% to 36.8%. But this was largely offset by shifting cross‑asset correlations, particularly with commodities, as both gold and oil saw higher percentage risk contributions rise by 2.7% and 1.7%, respectively. Despite this common increase, the two commodities played very different roles. Gold once again emerged as the riskiest asset relative to its portfolio weight, with declining prices for a third consecutive week amplifying its volatility at a time of broader market stress. Oil, by contrast, continued to act as a diversification buffer, with its higher prices and correlation profile helping to dampen, rather than amplify, overall portfolio risk.

Please refer to Figures 7-10 of the current Multi-Asset Class Risk Monitor (dated March 20, 2026) for further details.

You may also like