EQUITY RISK MONITOR HIGHLIGHTS

WEEK ENDED MARCH 20, 2026

Axioma Risk Monitor: Global equities are revisiting the 2022 playbook; Energy’s strong run has limited market impact

Global equities are revisiting the 2022 playbook

There are striking parallels between equity market reactions to Russia’s invasion of Ukraine in 2022 and those observed during the current crisis in the Middle East. In both episodes, a sharp oil shock rippled through global markets, igniting fears of higher inflation and weaker economic growth. At the same time, the US once again assumed its role as a safe haven, with the dollar strengthening forcefully in both periods.

These geopolitical shocks also unfolded in US midterm election years. In 2022, control of the House flipped from Democrats to Republicans, while prediction markets now strongly anticipate a reversal. The Senate remains a toss-up. Election years matter because political incentives are closely tied to near-term voter sentiment.

There are few signs that the current conflict is easing. Continued hostilities risk prolonging disruptions to oil supply, and recent escalations revived concerns about broader energy market dislocations. As in 2022, these developments have reinforced expectations of renewed global inflationary pressure.

Against this backdrop, central banks have turned more cautious. In a widely anticipated move, the Federal Reserve kept interest rates unchanged last Wednesday. The Fed was not alone: central banks in the UK, Switzerland, and Sweden also held rates steady. Rising oil prices have pushed investors to reassess the path of monetary policy, with markets increasingly pricing out rate cuts for the remainder of the year and even entertaining the possibility of rate hikes.

The contrast with 2022 is instructive. That year, the Fed raised rates seven times to rein in inflation, starting from an exceptionally low range of 0.00% to 0.25% as the economy emerged from prolonged Covid-era stimulus. By year-end, policy rates stood at 4.25% to 4.50%. Today, rates are already in the 3.50% to 3.75% range. While this reduces the likelihood of a similarly aggressive hiking cycle, the Fed’s recent pause, coupled with hints of potential increases later in the year, underscores that policy risks remain skewed to the upside.

A similar pattern is evident in Europe. The ECB raised rates for the first time in 11 years in July 2022, lifting them from deeply negative levels of minus 0.5%, and continued tightening through year-end, finishing at 2.50%. Last week, the ECB held rates at 2%. As in the US, there appears to be room for further increases in 2026 should inflationary pressures persist.

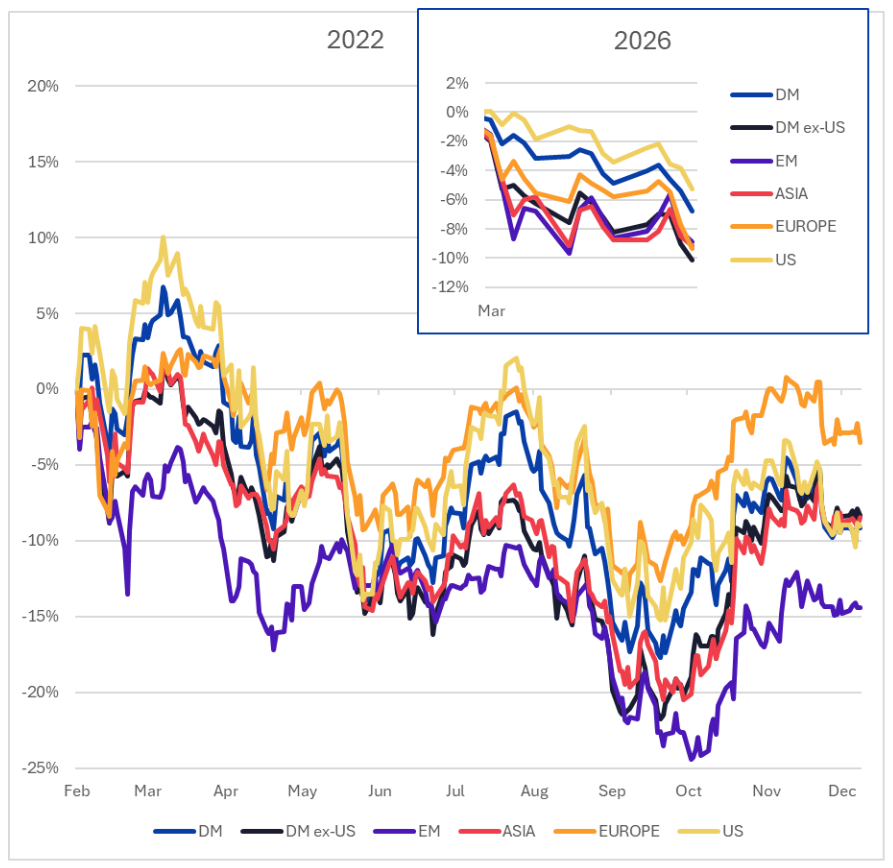

Market performance across regions has so far echoed the experience of 2022. Immediately after the outbreak of the Russia-Ukraine war, Emerging Markets, Developed Markets ex-US, and Asia suffered the steepest losses, with Europe underperforming the US. The same pattern has emerged following the onset of the Middle East conflict. However, in 2022, the far more aggressive US tightening cycle ultimately eroded the US market’s relative advantage, allowing Europe to outperform by year-end, supported in part by substantial government defense spending.

Emerging Markets endured the largest drawdowns not only in the immediate aftermath of the 2022 invasion but throughout the year. A similar outcome would be unsurprising in 2026 if the energy shock persists and the dollar continues to strengthen. As of last Friday, the US has experienced the smallest decline, down roughly 5%, while Emerging Markets, Asia, and Europe have each fallen by about 9% since the current conflict began.

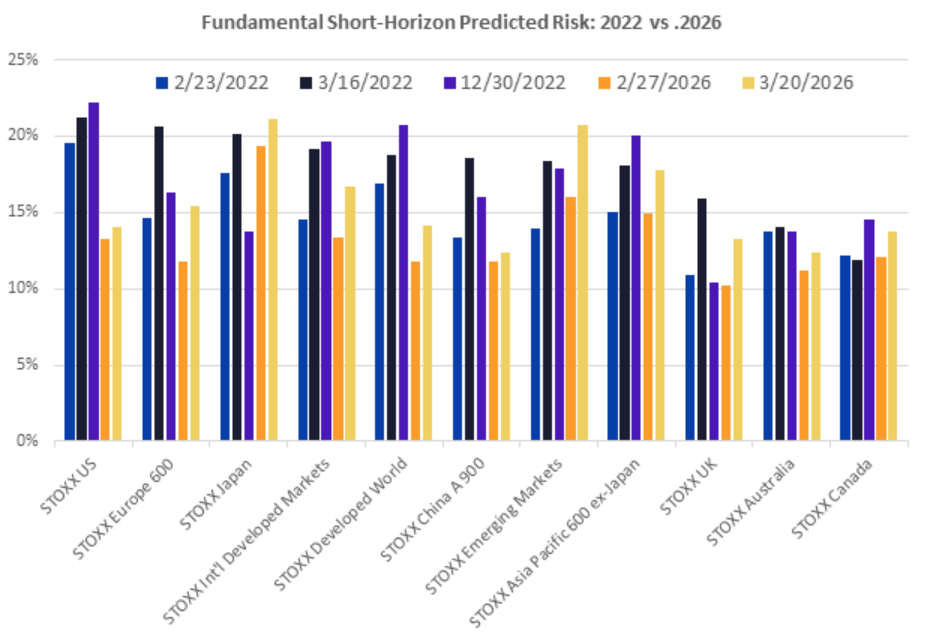

Risk dynamics also mirror the episode four years ago. Europe saw a sharp spike in risk in February 2022, as it has again in 2026, but ultimately finished 2022 among the least risky regions. Emerging Markets and Asia Pacific ex-Japan were among the riskiest regions after the conflict began in 2022 and show the same pattern today. Japan currently stands out as the riskiest region, with risk levels comparable to those seen four years ago, though its risk profile improved markedly by the end of 2022.

The US was the riskiest region heading into Russia’s invasion and retained that status through year end. In 2026, by contrast, US risk sat closer to the middle of the pack prior to February 28. Still, as in 2022, the increase in US risk following the onset of the conflict was relatively modest.

The charts below are not included in the Equity Risk Monitors but are available upon request:

Major Markets Cumulative Returns post-Crisis

Energy’s strong run has limited market impact

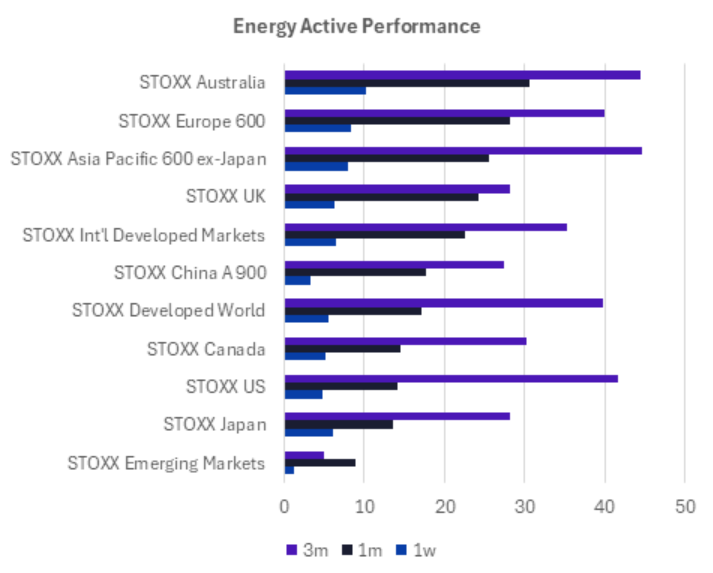

Despite its recent outperformance, Energy did little to offset losses in global equity indices, largely because of its relatively small benchmark weight. Even strong absolute returns were therefore insufficient to meaningfully lift headline index performance.

Although the sector has benefited from the recent spike in oil prices, Energy’s strength predates the escalation of the Middle East conflict. The sector has consistently outperformed its respective benchmark across most major regions over the past week, month, and threemonth periods, underscoring that its momentum has been building over time.

Over the past month, Energy delivered its strongest relative returns in Australia, Europe, and APAC exJapan, while active performance was more muted in the US, Japan, and Emerging Markets. Looking over the threemonth horizon, the US posted the thirdlargest active return, trailing only APAC exJapan and Australia.

Even so, the sector’s limited benchmark representation meant that its strong performance translated into minimal index impact across most regions. The UK, Europe, and Canada were notable exceptions, where Energy’s gains had a more visible influence on index returns. Elsewhere, the sector’s impressive performance over the past week, month, and three months largely failed to move the needle at the aggregate index level.

The chart below is not included in the Equity Risk Monitors but is available upon request:

See charts from the Equity Risk Monitors as of 20 March 2026:

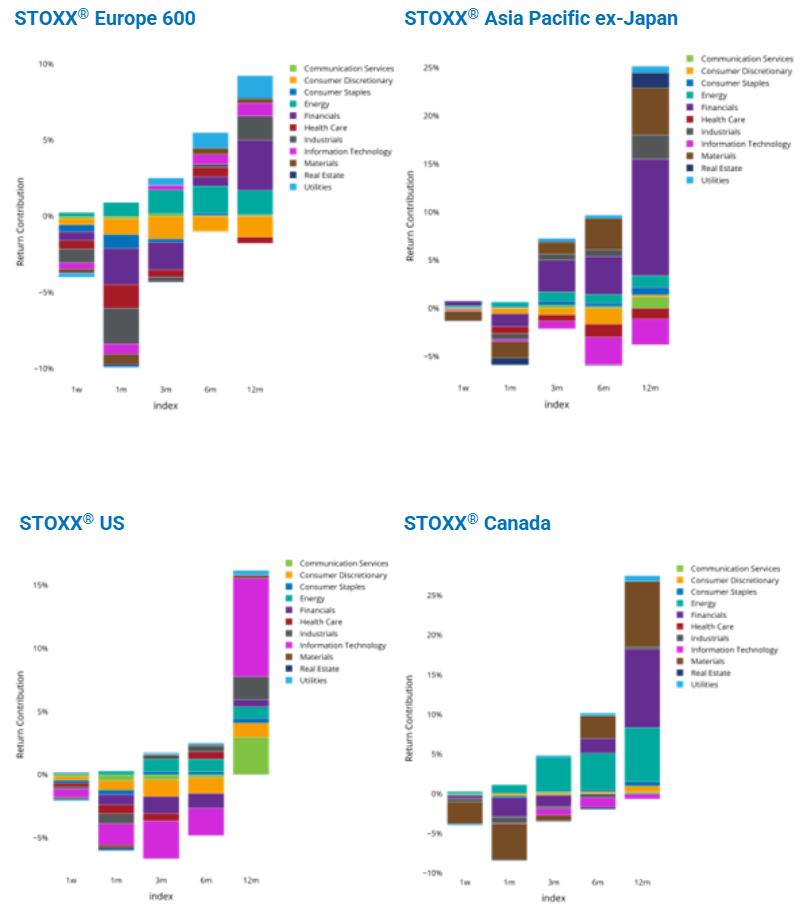

Sector Return Contribution

You may also like