EQUITY RISK MONITOR HIGHLIGHTS

WEEK ENDED APRIL 03, 2026

UK: Inflation Expectations Hammer FX Sensitive companies

The UK has been troubled by persistently higher inflation more than other developed countries over the last 12 months, and the new external shock of higher energy input costs caused by the Iran war and closure of the Strait of Hormuz has only exacerbated this issue.

While GBP lost about 2% of its value vs. USD and just 0.55% vs. the World Bank SDR basket that the Axioma Exchange Rate Sensitivity (ERS) factor is based on, the UK Exchange Rate Sensitivity factor was down 3.84% in March, which is a -5 standard deviation event relative to expectations at the beginning of March and the worst monthly return for this factor in its history including late June/July 2016 after the Brexit referendum, when GBP lost about 12% vs. USD and 8% vs. EUR and the ERS factor return was -2.1%.

The ERS factor does not measure instantaneous sensitivity to exchange rates- it partially explains the returns of companies whose residual returns have exhibited sensitivity to exchange rates. Even if the home currency doesn’t move much over a crisis period like the one we currently find ourselves in, if the perceived terms of trade in a country change, this is when we see large moves in the factor return, because the companies that have “exchange rate sensitivity” are being re-priced- in some cases by orders of magnitude more than the currency itself has been repriced to that point.

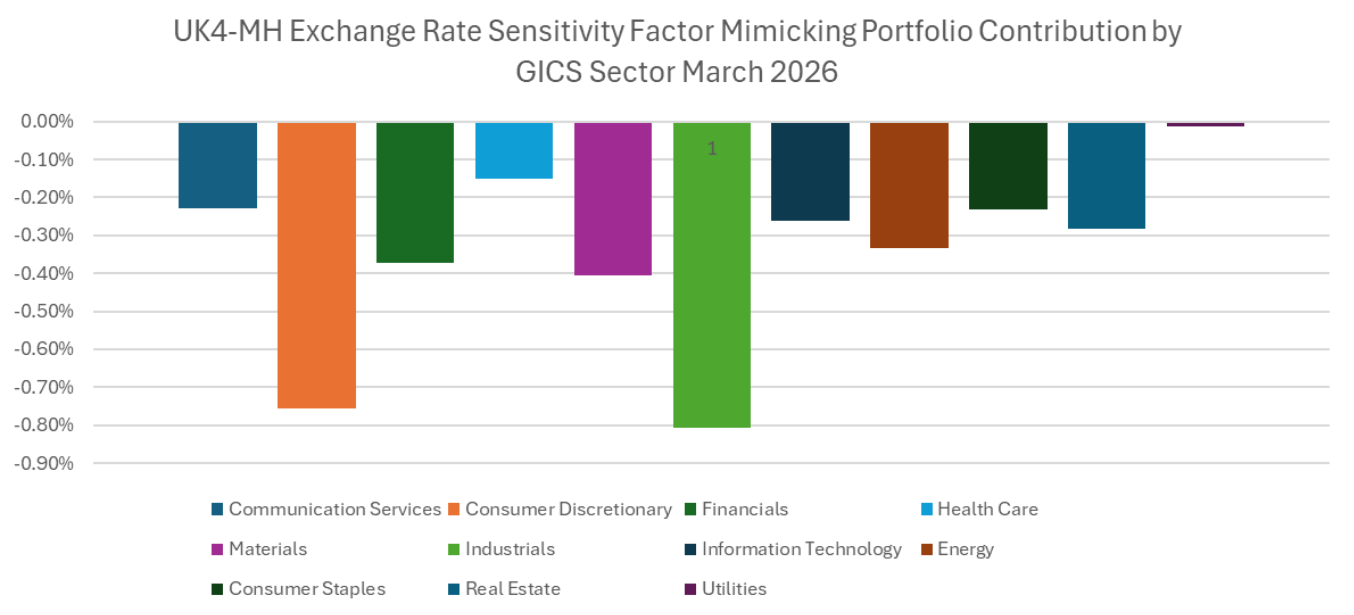

We can see this in sharper relief by examining the return of the UK ERS factor mimicking portfolio (FMP). An FMP is the solution to the weighted-least squares regression that yields the daily factor returns- the set of asset weights that gives us unit exposure to each individual factor and zero exposure to all other factors with minimal specific return. When we sort the assets in the UK ERS FMP by GICS Sector, we can see which sectors of the UK economy were most affected by this apparent repricing:

The three sectors most affected are 1) Industrials, 2) Consumer Discretionary, and 3) Materials. Industrials suffer because of higher fuel costs, priced in USD; Discretionary suffers from higher shipping costs (mainly from Asia) directly related to potential fuel shortages in Asian exporting countries, and Materials because of higher feedstock costs being supplied from the Persian Gulf region.

The ERS factor in other models behaved as follows:

Exchange Rate Sensitivity Factor Returns: March 2026

Australia experienced a similar factor return, but no other market came close. The UK result may be due to the fact that the domestic situation was already inflationary due to a wage-price spiral, and now the prospect of imported inflation via the oil shock has the potential to weaken Sterling further than previously thought, making the outlook for those FX-sensitive companies worse.

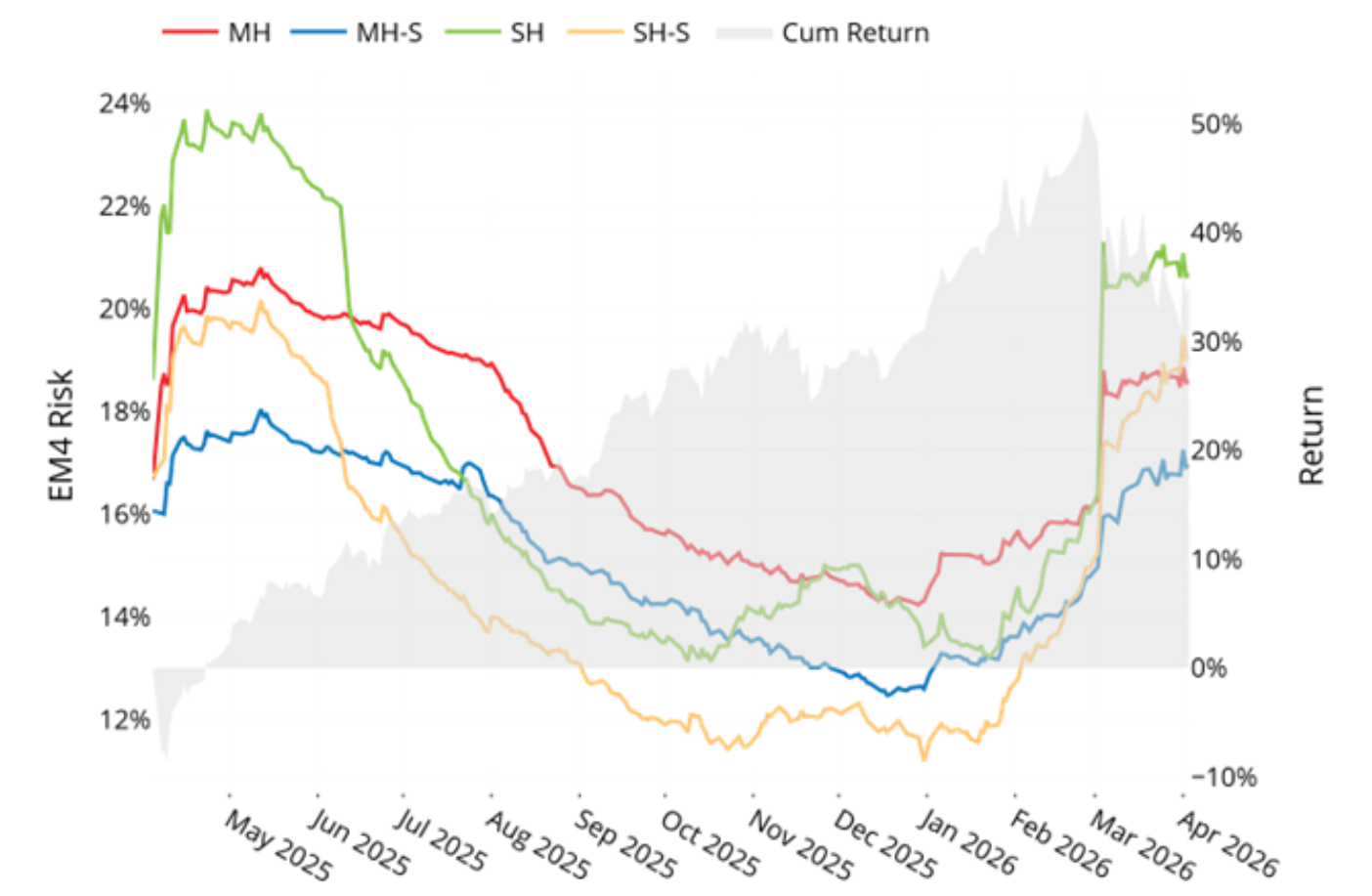

Emerging Markets Risk Surge

Just when everyone thought it was safe to go back in the “pool” of Emerging Markets equities after years of outsize gains in US Equities, the STOXX Emerging Markets index is down 10.3% since the outbreak of hostilities in the Persian Gulf while predicted risk has soared 46% on average across the 4 EM risk models- the largest change in any of the markets we track:

See chart from the STOXX Emerging Markets Equity Risk Monitor of March 3, 2026

Chart 7, STOXX Emerging Markets- Predicted Risk

Prior to this war-related correction (drawdown?), the EM index had been on a tear, rising 48% between May 2025 and the end of February 2026. On December 31, 2025 the average forecast risk over all 4 EM models was just 12.9%, and as of April 3 it is 18.8%.

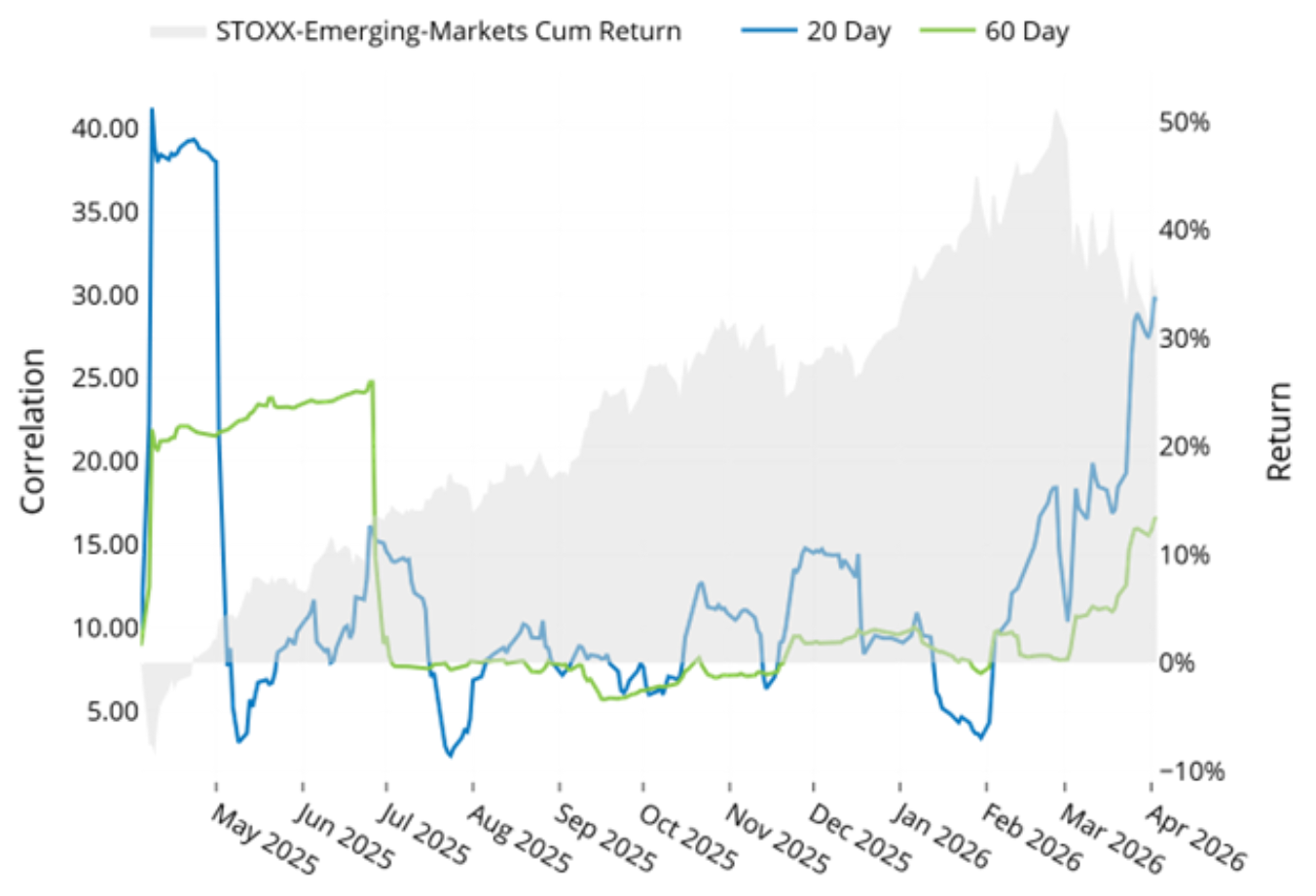

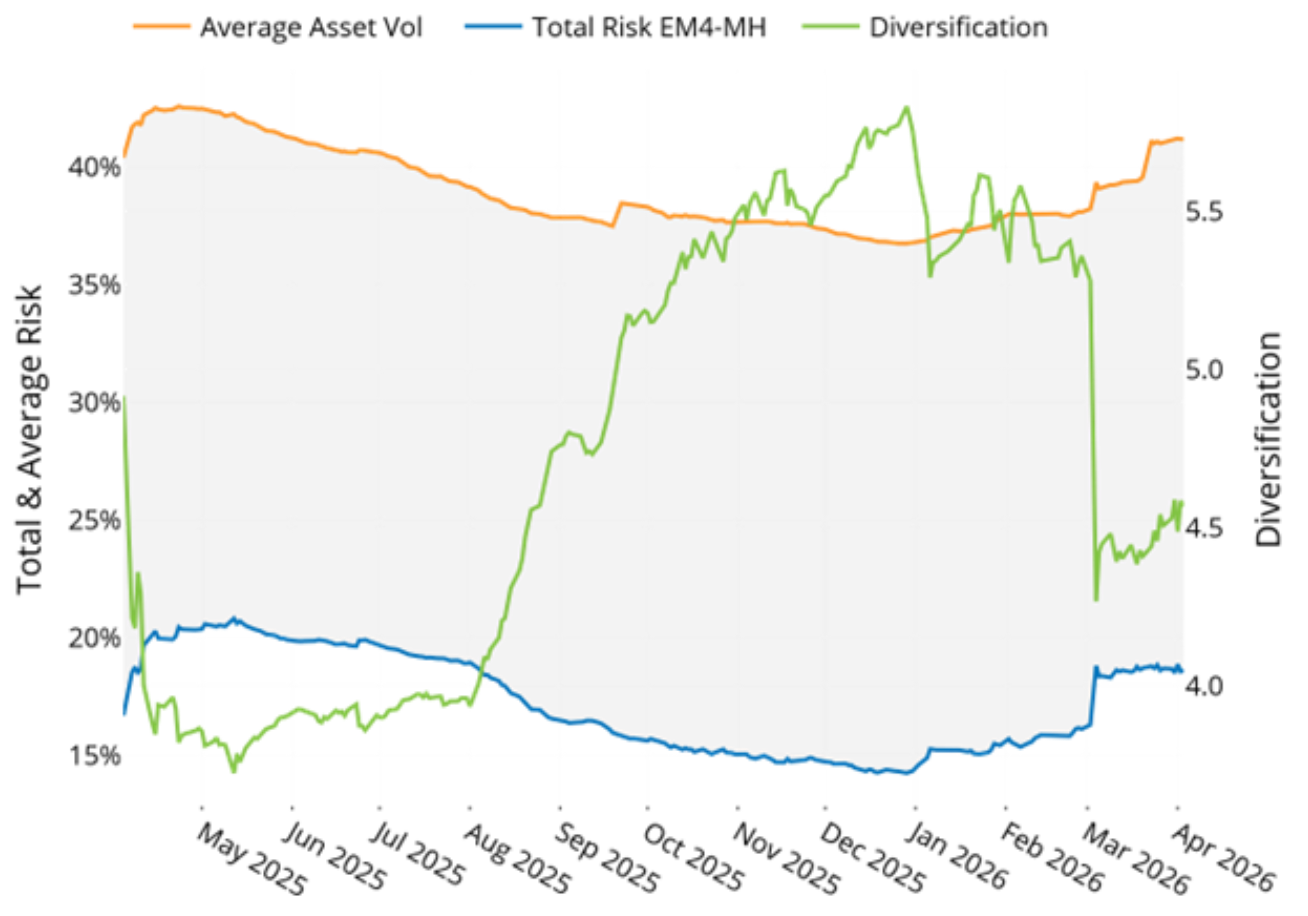

In sharp contrast to the US market, correlations in Emerging Markets are soaring to “Liberation Day” levels and the index “Diversification Ratio”, which describes the difference between the weighted average asset volatility and index portfolio volatility has fallen precipitously:

See chart from the STOXX Emerging Markets Equity Risk Monitor of March 3, 2026

Chart 12, STOXX Emerging Markets- Rolling Average Asset Correlations

Chart 22, STOXX Emerging Markets- Diversification Ratio

Just about every CIO and Investment pundit has talked up rebalancing away from the US and towards Emerging Markets for the opportunity and what seemed like a long-overdue rotation, but these last few weeks have served as a reminder that while a sizable allocation to EM might be warranted, it is still a high-beta, riskier class of equity investing that tends to be very sensitive to flows.

You may also like