IBOR

Release 26.07

![]()

Enable immediate blocking of positions directly from election workflows

This enhancement introduces the ability to initiate position blocking directly from the corporate action manager election window, removing the dependency on static data availability.

Previously, blocking for elective corporate actions relied on static data being loaded before blocking transactions could be generated. This created operational challenges where clients needed to secure positions immediately after making elections - particularly for pledged or sensitive holdings - but were unable to do so automatically due to dependency on static data.

With this release, blocking is now driven directly from the election workflow. Clients can define and apply blocking at the moment an election is saved, ensuring immediate blocking of eligible elected positions. The solution supports a wide range of elective event types, including tender offers, exchange offers, mergers, and rights issues.

Key enhancements include updates across the user interface, APIs, data model, and processing logic. The solution introduces configurable blocking defaults, enhanced election grids with blocking controls, and new backend processing capable of generating blocking transactions without waiting for static data.

Benefits

- Reduces operational risk by preventing unintended position sales after elections

- Enables real-time blocking aligned with election activity

- Eliminates dependency on static data timing for blocking

- Improves control and transparency

- Supports a broad range of elective event types for consistent handling

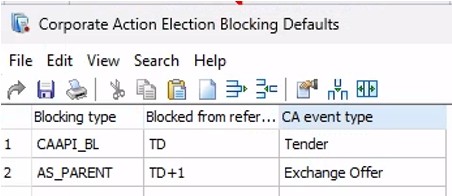

A new Corporate Action Elections Blocking Defaults window has been introduced to let users define default parent-blocking rules for elective corporate action events. In this window, users can maintain a CA event type, Blocking type, and Blocked from reference date. The event type can be specified for event-specific rules, while a default row without an event type is used as fallback. These defaults are applied when elections are saved, so blocking information can be populated directly on the election instead of relying on blocking setup in CA static data.

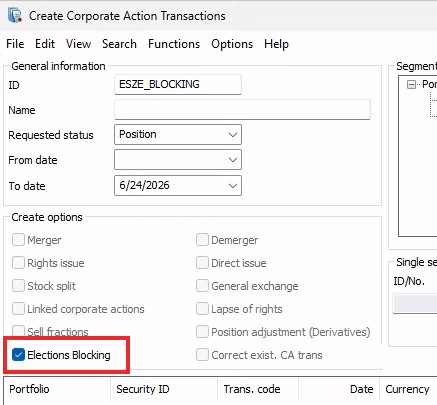

On the Create Corporate Action Transaction window, a new Elections Blocking option is available. When selected, the system generates parent blocking transactions based on the saved election blocking data. This allows blocking transactions to be created even when CA static data has not yet been created or transferred. The process is intended for elective events, where blocking must happen as soon as the election is made, and creates blocking transactions for the relevant elected holdings/options.

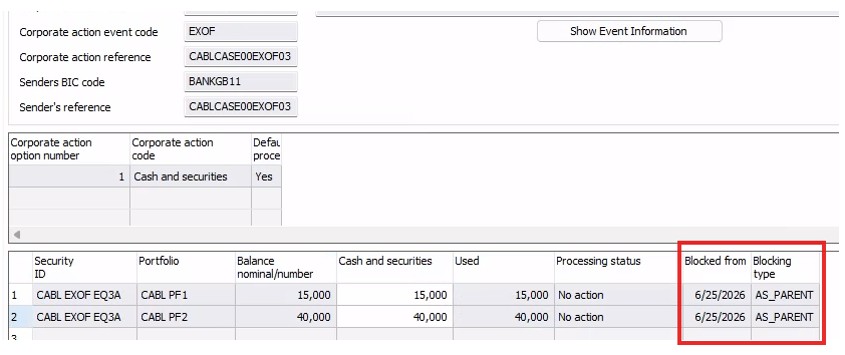

In the CAM Elections window, the blocking fields are now available directly on the election grid for supported events. Users can work with Blocking type, Blocked until, and the new Blocked from field. The fields show existing blocking information where blocking already exists, or allow blocking values to be applied and saved from the election flow. When relevant election or blocking values are changed, the system can delete existing election-based blocking transactions so that corrected transactions can be generated again.

Subscription-based licensing

Equity - Securities

Sales module dependency

Equities & Fixed Income

![]()

End-to-end improvements for TRS processing, including automated cancellation and enhanced import handling

This release introduces a comprehensive set of enhancements to improve the automation, accuracy, and robustness of Total Return Swap (TRS) corporate action processing for Single Name contracts.

A key capability introduced is the ability to cancel previously booked corporate action transactions directly through import files. Clients can now identify transactions using their own references and perform cancellations in a structured, automated way, with the option to rebook corrected transactions separately. This removes the need for manual intervention in Trade Manager and streamlines correction workflows.

In addition, the release introduces real termination transaction generation, aligning system behaviour with the true economic outcome of events such as full call, partial call, and final maturity.

Real termination processing includes:

- Direct generation from import files, using event-driven inputs

- Population of the corporate action event type on the transaction

- Accurate sizing using nominal/number of shares from the file

- Price and FX rate handling at termination, supporting single- and cross-currency TRS

- Validation to ensure eligibility (e.g., bond-underlying TRS only)

Beyond termination, the release strengthens the TRS import and processing framework through:

- Improved contract identification via security references

- Standardised transaction status assignment

- Enhanced XML mapping and validation controls

- Trade date support within cancellation workflows

Operational transparency is improved via clearer batch job validation messages aligned to XML tags, making issues easier to diagnose and resolve.

Benefits to Clients

- Enables true economic termination of TRS contracts, improving accuracy and reporting

- Provides automated cancellation and correction workflows, reducing manual effort

- Improves data accuracy through precise handling of nominal, price, and FX at termination

- Enhances traceability with event-linked transactions and external references

- Reduces operational risk and exceptions, especially for complex and backdated events

- Improves transparency and troubleshooting with clearer validation and logs

Subscription-based licensing

Corporate Actions Manager, TM Total Return Swap

Sales module dependency

Corporate Actions Manager, TM Total Return Swap

![]()

Rollover lifecycle event for TRS – Single Name equity Swap

As of release 26.07, the rollover with new trade id, lifecycle event has been added to the Equity Swap instrument.

Benefits

- As of release 26.07, you can book a rollover for a single name Total Return Swap (TRS) contract in SimCorp Dimension. You can close an existing TRS contract and open a new one with a different trade ID, while adjusting the notional amount, spread, and so on. This enhancement gives you greater control over contract renewals, terms, and balances. You can manage TRS contract lifecycles more easily and accurately.

- When you book a rollover, you close the old contract and open a new one. The new contract uses its own trade ID, balances, and terms. During the rollover, you can change the notional amount, spread, and so on. You can also specify a closing price for the old contract, and an opening price for the new contract.

- SimCorp Dimension calculates the profit and loss (P/L) for the closed contracts. You can choose not to trigger payment on the TRS close transaction by selecting the Do not trigger payment on TRS close transaction check box. If you select this check box, the old contract stays open to ensure that income can be received and reset after the rollover. Otherwise, the close leg of the rollover can include a cash amount. This functionality is only available for a single-name TRS with an underlying equity.

Subscription-based licensing

TM Total Return Swap

Sales module dependency

Alternative Investments Manager, Cash-flow TM Total Return Swap

![]()

General reconciliation enhancements

Reconciliation Manager supports reconciliation actions directly on grouped rows in the Results Monitor. When results are grouped, users can select one or more valid group rows and apply supported actions to the underlying reconciliation results in each group, instead of expanding the group and selecting individual result rows manually.

Supported group-level actions include matching and unmatching, adding free comments, assigning results to a user, and updating multiple classification fields at once via the Deviation Details applet. Payment and cash-related actions are also supported, including interim suspense payments, partial pay, and force close.

This makes high-volume reconciliation work faster and easier, especially when users already work with grouped views (e.g., group by matching index) to analyse exceptions. Actions are only enabled when the records from the groups are valid for the action, helping users apply bulk updates safely while keeping the existing Results Monitor workflow.

- Reduces manual effort by allowing actions on grouped reconciliation results.

- Improves efficiency when handling large volumes of exceptions.

- Keeps the familiar Results Monitor grouping workflow.

- Applies actions per selected group, preserving existing validation rules.

Subscription-based licensing

IBOR Manager And Investment Operations API

Sales module dependency

Reconciliation Manager

Browse the Release Portal

Release 26.04

OTC – CDS Index option in Trade Manager

The CDS index option is now available in Trade Manager, featuring a Trade Manager-based Index CDS as its underlying instrument. This option uses an EU style exercise, meaning it can only be exercised at expiration, and physical delivery, which requires that the underlying CDS contract is delivered to the holder when the option is exercised. These mechanisms provide clarity and standardization for transaction settlement.

The CDS index option supports both cleared and bilateral transaction flows, along with all related lifecycle transactions, making it flexible for different trading environments.

Strike price can be defined as either a spread or a price, and the underlying index CDS is specified using the recently introduced CDS Standard Product functionality (effective from 07/25).

Theoretical pricing of the CDS index option is fully supported through the OneLib and FINCAD pricing libraries. OneLib and FINCAD are specialized software tools that perform complex calculations to estimate the fair value of financial instruments, helping users assess option pricing and risk.

As of the 26.04 release, the “Done deal” flow is fully supported, allowing users to efficiently finalize transactions. Please note that order flow integration will be available in a future release, ensuring a seamless experience for managing orders once this functionality is introduced.

Benefits

- The CDS index option is a new instrument type in Trade Manager, fully integrated into both cleared and bilateral lifecycle flows. Exercising this option results in the creation of a Trade Manager-based index CDS, streamlining the process for users.

- This option is fully aligned with clearing house protocols. A risk manager can use the CDS index option to hedge credit volatility by purchasing the option and then exercising it to obtain exposure to the underlying index CDS. This enables efficient management of credit risk and supports strategic migration of positions to optimize clearing and settlement.

Subscription-based licensing

TM CDS Index option

Sales module dependency

Credit - Credit Default Swaps and Swaptions

![]()

Automated Increase-based processing of selected TRS corporate actions via structured file import

It is now possible to automatically create Increase transactions for selected corporate action events on single-name Total Return Swaps (TRS) through the import of a structured file containing corporate action information (for example, XML-based files).

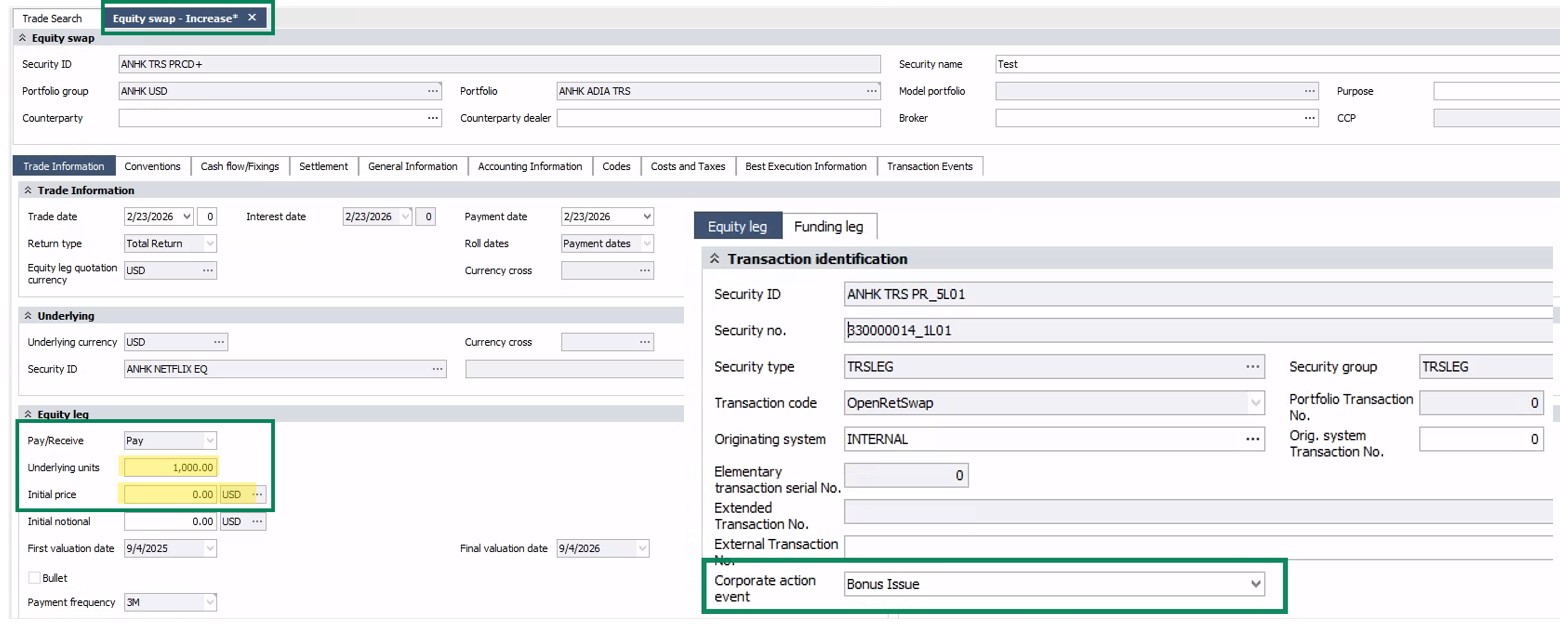

For supported event types such as Bonus Issue (BONU), Stock Split (SPLF), and Stock Dividend (DVSE), the system can generate an Increase transaction to reflect the nominal impact of the corporate action. These increased transactions can be created in Trade Manager with the transaction price automatically set to zero. This allows nominal adjustments resulting from corporate actions to be reflected while preserving the existing TRS contract, supporting better trade continuity and more operationally efficient processing.

The enhancement also introduces integration flexibility for corporate action event files. The import uses a hardcoded default mapping for supported structured file tags and optionally allows clients to apply an XSLT transformation to translate their own structured file formats into the expected format. This removes the need for a dedicated tag-mapping screen, reduces configuration effort, and simplifies support for client-specific file layouts. The import supports structured corporate action event files, allows multiple files to be processed from the configured import directory, and passes the resulting changes to Trade Manager for downstream handling.

Benefits

- Streamlines corporate action processing for TRS by enabling nominal adjustments to be handled through a dedicated Increase transaction, reducing operational complexity for supported event types

- Preserves trade continuity by keeping the original TRS contract intact, helping firms maintain clearer trade histories and simpler lifecycle management

- Improves integration flexibility by supporting structured corporate action event files and allowing client-specific formats to be translated using XSLT where needed

- Supports scalable growth by establishing a robust and extensible foundation for future enhancements to TRS corporate action processing and import capabilities

- Improves valuation accuracy by ensuring nominal adjustments are applied at a zero price, allowing the next reset to fully and correctly recalculate the contract value

This image highlights an Increase transaction booked at a zero price, automatically generated from corporate action information and clearly marked with the corporate action event indicator.

Caption: Zero priced CA Increase transaction with corporate action indicator

Subscription-based licensing

Corporate Actions Manager, TM Total Return Swap

Sales module dependency

Corporate Actions Manager, TM Total Return Swap

Enabled TRS closure using Modify Position based on Number of units

As of release 26.04, the following new fields have been added to the Modify position option in Asset Manager:

- Existing number of underlying

- You can modify Number of underlying, but can only view Existing number of underlying.

These fields enable you to use the Modify position option in Asset Manager to partially close Total Return Swap (TRS) positions based on the number of Underlying units rather than the Initial notional number. In addition, the Balance number of underlying field has been added to the Simulations applet. - Over the lifetime of a TRS contract, the initial notional can change because of periodic resets, which enables a portfolio manager to think more in terms of the underlying. The Number of underlying field can also be modified in the Simulations applet in Asset Manager.

- The Underlying units field in the Trade Manager equates to the Number of underlying field in Asset Manager. This is valid for:

- You can modify Number of underlying, but can only view Existing number of underlying.

- Instrument sub-type — Bond swap, Equity swap, Index swap

- Transaction type — Close

Benefits

- Enables users to close a TRS based on number of units rather than notional amount

Subscription-based licensing

TM Total Return Swap

Sales module dependency

TM Total Return Swap

Added Status Tab to TRS basket

As of release 26.04, you can view the basket composition information for TRS baskets in the Trade Manager. This enhancement provides transparency in how resets and basket adjustments affect basket valuations during lifecycle management of TRS baskets.

The new Basket Status sub-tab displays a snapshot view of basket composition on the date specified in the As of date field. The Basket Status sub-tab shows the following information for a TRS basket on a specific date:

- The Last reset date field displays the most recent reset date for reference. The corresponding Basket value QC field displays the aggregated value of all basket constituents at that time. These fields are auto-populated and cannot be modified.

- You can view the basket composition based on adjustments that are applied sequentially by dates, on top of the last reset or initial basket (whichever is applicable).

- You can also view the averaged prices and FX rates derived from the reset date and any adjustments that follow in the basket status information grid.

To view the latest TRS basket status, go to the Basket Status sub-tab in the Basket Information section under the Trade Information tab. Alternatively, you can also view the Basket Status sub-tab under the new Basket Information tab. In the As of date field, you can enter the date for which the basket status must be displayed. The basket status information grid displays the valuation inputs and adjustments applicable to that specific date.

The values in the basket status information grid do not appear in other pricing or grids but enable you to validate expected performance after adjustments.

Benefits

Enables users to view an update or past view of the current basket constituents on a TRS bond basket or equity basket

Subscription-based licensing

TM Total Return Swap

Sales module dependency

TM Total Return Swap

Bulk processing added to OTC web API

New endpoints have been added to the OTC web API, designed to handle large volumes of incoming contracts. These endpoints accept any mix of either transactions or order, and will then process these in the most optimal way. Significant performance improvements have been observed for this approach. Furthermore, resiliency mechanisms have been implemented for these endpoints, so that in case of an outage they can resume execution at the appropriate point, without manual intervention.

Benefits

- Significant performance improvement, especially at large volumes

- Resiliency mechanisms have been built in, to reduce operational risk

Subscription-based licensing

OTC web API

Sales module dependency

Trade Manager

Added four more classification-like fields with value-level authorizations and bulk update.

Reconciliation Manager now supports four additional controlled classification fields (Classification 2–5) alongside the existing Classification. This makes it easier to tag and organise reconciliation results using pre-defined, consistent values instead of relying on free text.

The new classification fields are available in Reconciliation Manager screens (Results Monitor and dashboards) and support fast, bulk updates. You can enter values in the redesigned Deviation Details applet and apply them to multiple selected results in one go, with per-field control over whether existing values should be overridden or not. Reconciliation free code 5 (of type: Date) and Free Comment can now be updated in bulk as well.

Classification lists can be maintained per reconciliation setup, so different teams can work with the terminology that fits their process and reconciliation type.

Importantly, the solution has two levels of authorisation support:

- users can be restricted from updating fields by removing access to the field itself

- specific classification values can be made read only for unauthorised profiles

This enables more governed operational workflows — for example, using controlled classifications as part of break approval or escalation flows — while keeping automation possible via extended Auto-fill rules and rollover support.

Each classification field comes with three related values: ID (the editable field), plus Name and Description — enabling more meaningful, longer text to be displayed in the Results Monitor and used for reporting.

Benefits

- improving transparency, data quality and consistency

- faster break processing via bulk operations

- improved governance and control through authorisations

Subscription-based licensing

Reconciliation Manager

Sales module dependency

IBOR Manager

Release 26.01

Spread option enhancements

As of version 26.01, the Spread option, OTC instrument supports forward premium payments and barrier conditions on the underlying assets in the Trade Manager.

With the forward premium payment enablement, the user can define when the premium is paid (spot or forward). With this enhancement, you can select whether the premium is paid upfront (spot) or at maturity (forward).

Optionally, you can also define the barrier levels for each underlying asset to control when the option becomes active. To support rate contingency, two optional fields—Upper barrier and Lower barrier—have been added for each underlying asset. These fields define thresholds that determine whether the option becomes active and generates a payoff.

The pricing correlation setup is now optional and only required if you specify a contract-specific pricing model. If you price the spread option without this model, you do not need to specify pricing correlation.

Benefits

- Enables users to book a Spread Option transaction according to market standards

- Enables users to handle more exotic Spread Option variants with conditional payoffs

Subscription-based licensing

TM Spread Option

Sales module dependency

TM Spread Option

![]()

Handling caps/floors on daily fixings

As of version 26.01, you can apply caps and floors to daily reference rate fixings on overnight index swaps (OIS) for Flexi Formula Swap XpressInstruments.

Benefits

- Enables the user to apply a cap or a floor on the individual daily fixing rate, like SOFR/SONIA, when calculating the daily compounded rate

Subscription-based licensing

XpressInstruments custom

Sales module dependency

N/A

![]()

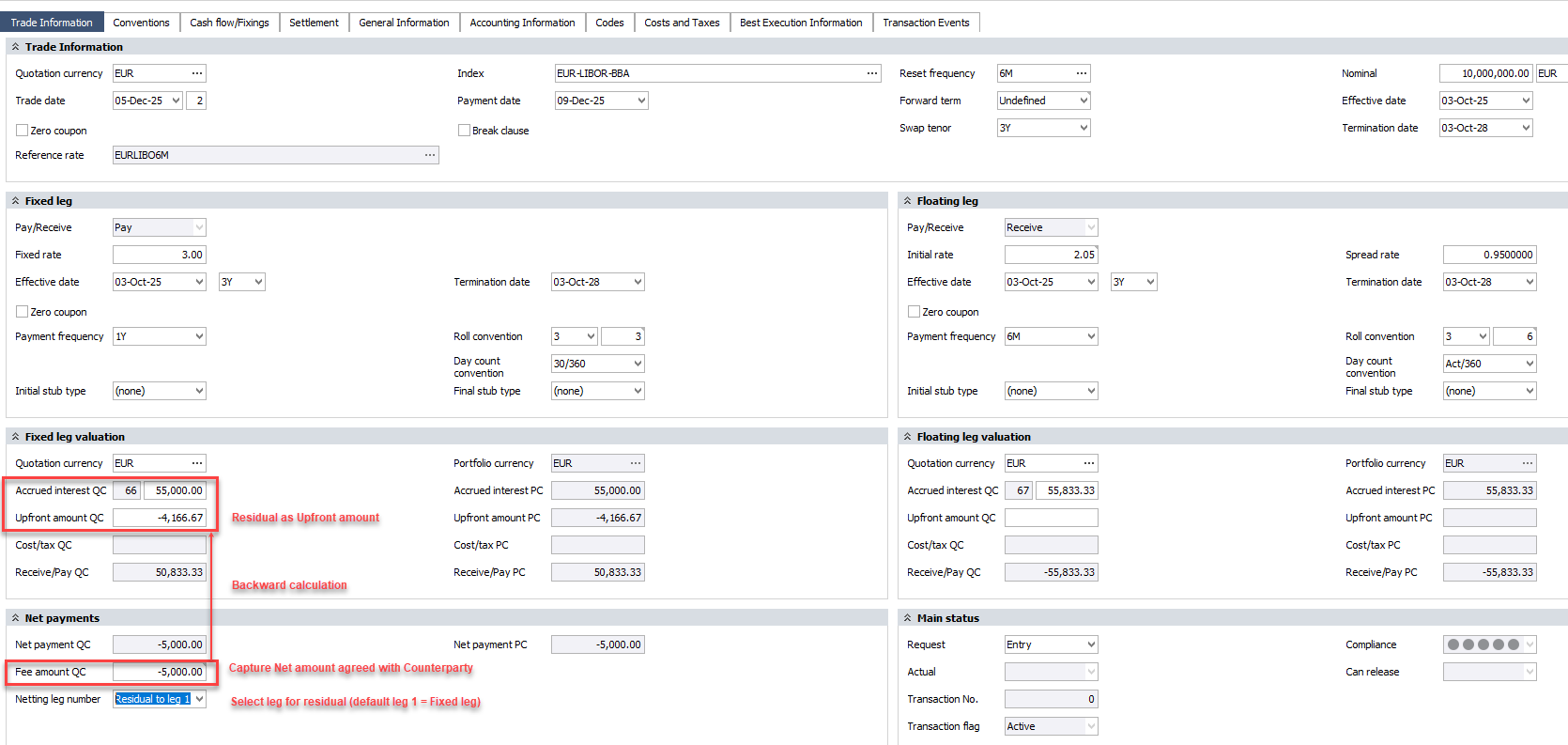

Interest rate swaps – Support trading on NPV

As of version 26.01 it is possible to trade Interest Rate Swaps (deliverable and non deliverable currencies) based on agreed net present value. SimCorp Dimension will then do the backward calculation of accrued interest on the two legs and place the residual as an upfront amount on the chosen leg (Default is to place the Residual on leg 1, which is the fixed leg for the supported types).

This new feature is especially relevant when doing offset trades and post trade events for bilateral swaps and it is the Standard used by most Trading platforms. The new feature is available for

Swap types:

- IR swap, fixed/float

- IR swap, OIS

- Non-deliverable IR swap fixed/float

Event types: - Close (existing)

- open new

- Increase existing

- Offset close

- Increase new

- Novate

Benefits

- Align with market standards when executing offset trades and performing post trade events

Subscription-based licensing

Interest Rate – Swaps and Swaptions

Sales module dependency

Fixed/Float Interest Rate Swaps,

Asset swaps and Non-deliverable swaps

![]()

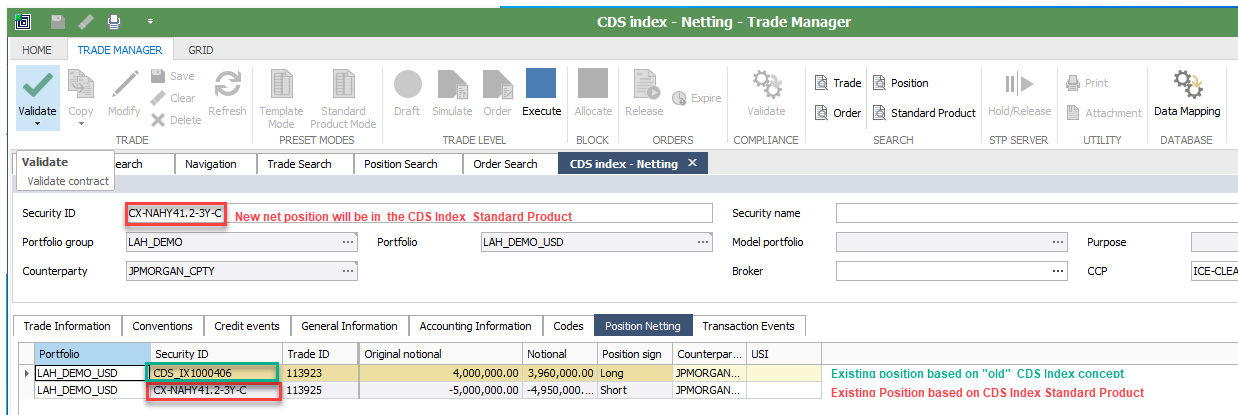

CDS Index – New features for CDS Index Standard products

A group of new features Related to CDS Index has been introduced with 26.01.

The first new feature is the possibility to define standard settlement days for transactions based on standard products (typically 1 day for Cleared CDS Index Trades and 3 days for bilateral). The standard settlement days can be maintained in the convention tab for CDS Index Standard products.

The second feature introduced with 26.01 is the possibility to do netting across existing positions using the “old” CDS Index concept and positions using the “new” CDS Index Standard product concept. The result will be a position in the Standard Product. This feature makes it possible to make a smooth and easy transition of existing CDS Index positions (based on the “old” concept”) to the new CDS Index Standard Product concept without need for a “big bang” or conversion of existing data.

Benefits

- Smooth transition from the “old” CDS Index concept to the “new” concept based on Standard Products

Subscription-based licensing

Credit – Credit default Swaps and Swaptions

Sales module dependency

CDS Index as a standard product

![]()

Valuation of Mid Curve Swaptions and CMS Spread Options

You can now perform advanced valuation and risk analysis for complex interest rate derivatives using two new pricing models:

- Gaussian-Copula Model with Normal SABR for CMS Spread Options

Enables accurate pricing and sensitivity analysis for CMS spread options, incorporating swap rate correlations and volatility surfaces.

- Bachelier Model for Mid-Curve Swaptions

Supports valuation of mid-curve swaptions and is captured in Trade Manager, providing robust analytics under normal volatility assumptions.

Instrument Scope

- TM Spread Option, OTC, with underlying CMS rate

- TM Swaptions, Fixed/Float and OIS, with Forward term

Benefits

Comprehensive Risk Metrics

Calculate prices, sensitivities, and Greeks including:

- Delta, Gamma, Vega, Theta

- DV01, OAS

- Dirty price, Clean price

- Correlation sensitivity (Rho)

Improved Accuracy for Complex Structures

Advanced models (Gaussian-Copula + SABR, Bachelier) allow calibration to market prices and precise valuation of instruments sensitive to correlation and volatility shifts.

Scenario Analysis and Portfolio Impact

Incorporate market data scenarios for portfolio-level calculations, improving decision-making under different market conditions.

Streamlined Workflow

Direct integration with Trade Manager and Volatility Curve Definitions ensures smooth setup:

- CMS Spread Options: Configure underlying reference rate, par yield convention, and single-look payment structure.

- Mid-Curve Swaptions: Capture trades with correct reset frequency and ATM moneyness.

Transparency and Troubleshooting

Use Calculation Trace and Explain Calculation for detailed diagnostics during valuation.

Why This Is Valuable

These enhancements empower users to:

- Confidently price and manage risk for CMS spread options and mid-curve swaptions.

- Meet regulatory and internal risk management requirements with accurate Greeks and correlation sensitivities.

- Reduce operational complexity by leveraging integrated workflows and standardized data sources.

Subscription-based licensing

Interest Rate - OTC Derivatives,

Interest Rate – Swaps and Swaptions

Sales module dependency

No dependency

![]()

Valuation of Convertible Bonds with Ayache-Forsyth-Vetzal model

You can now use Ayache-Forsyth-Vetzal (AFV) model for pricing convertible bonds. This enhancement enables accurate valuation and risk analysis for convertible bonds using advanced numerical methods, supporting both theoretical pricing and calibration to market price.

- Convertible bonds with underlying instruments:

- Equity

- Fund certificate

- GDR/ADR

Benefits

- Comprehensive Analytics for Convertible Bonds

- Calculate a wide range of key ratios and risk measures.

- Credit Spread Handling

- The AFV model uses the spread yield curve for credit spread specification, ensuring more accurate discounting and calibration.

- Dividend Projection Support

- For convertible bonds with equity underlyings, valuations incorporate time-series dividend projections.

- Calibration to Market Prices

- The Quoted price + yield curve method supports calibration by calculating OAS, enabling alignment with observed market prices.

- Integrated Workflow and Transparency

- Updated Explain Calculation report reflects AFV model enhancements, and Calculation Trace supports troubleshooting.

Why This Is Valuable

These enhancements empower users to:

- Accurately price and manage risk for convertible bonds in portfolios.

- Incorporate realistic dividend projections and credit spreads for better valuation precision.

- Meet compliance and reporting requirements with full transparency and detailed analytics.

- Streamline workflows by leveraging integrated pricing definitions and volatility curve settings.

Subscription-based licensing

Foundations

Sales module dependency

No dependency

Release 25.10

Index fixing for swaps in Trade Manager

As of version 25.10, users of TRS in the trade manager can add their own “customer” business centers in addition to the standard business centers maintained by Simcorp. Users can add the new business centers via the new business center form and will be able to link them business center calendars in the same way as the previous standard centers.

These new “customer” business centers will be shown with the business center owner as “customer” and will only be selectable on the following instruments:

- Index Swaps

- Bond Swaps

- Equity Swap

- Bond swap, baskets

- Equity Swap, baskets

This enhancement will allow users to define business centers that are not in the current FpML list such as exchange business centers. This will enhance the flexibility of those instruments where they are permitted.

Subscription based licensing

TM Total Return Swap

Sales module dependency

TM Total Return Swap

![]()

Enhancements for exotic FX options in Trade Manager

As of version 25.10, the Trade Manager introduces enhancements for exotic FX options, with a focus on improving lifecycle handling, transparency, and alignment with market standards. These enhancements support correct modelling of barrier options, rebate handling, and valuation logic across the following exotic FX options:

- FX Option, Double Barrier

- FX Option, Single Barrier

- FX Option, Touch

Benefits

- Barrier window configuration—For FX Option, Single Barrier, FX Option, Double Barrier, and FX Option, Touch instruments, you can define a custom barrier observation period. You can do so by using the new Barrier window start and Barrier window end fields. This barrier observation period is independent of the effective dates and expiry dates applicable for the option but must remain within the effective expiry range.You can start the barrier observation period on the same day as the option's effective date, in line with market standards.

- Barrier window type—For FX Option, Single Barrier and FX Option, Double Barrier instruments, you can specify the barrier window type as either American or European in the new Barrier window type field.

- Rebate handling—For FX Option, Single Barrier and FX Option, Double Barrier instruments, the new Rebate field is available. SimCorp Dimension supports rebate amounts and automatically processes them for knock-in and knock-out scenarios where the option remains, or becomes inactive. Rebate payments are generated on expiry and are handled as separate payments, with no link to forward premium.

- Barrier description—For FX Option, Single Barrier and FX Option, Double Barrier instruments, a second option is available next to the Barrier type field. This second option reflects combinations of option types and barrier types applicable to the FX option.

- Support for knock-in/knock-out barrier combinations—For FX Option, Double Barrier, you can configure barrier type combinations such as knock-in-knock-out scenarios.

- Monitored values—For FX Option, Single Barrier, FX Option, Double Barrier, and FX Option, Touch instruments, the new BARRIER_HIT and OPTION_ACTIVE monitored values are available. These values help you track whether a barrier has been breached and whether the option is currently active. These values can be retrieved by using relevant formula functions. You can also use the new getximmonitored() formula function that retrieves monitored values from XpressInstruments—specifically for use in transaction-level and position-level contexts.

Subscription based licensing

TM Total Return Swap

Sales module dependency

TM Total Return Swap

![]()

Enhancements to TRS business centres in Trade Manager

As of version 25.10, users of TRS in the trade manager can add their own “customer” business centers in addition to the standard business centers maintained by Simcorp. Users can add the new business centers via the new business center form and will be able to link them business center calendars in the same way as the previous standard centers.

These new “customer” business centers will be shown with the business center owner as “customer” and will only be selectable on the following instruments:

- Index Swaps

- Bond Swaps

- Equity Swap

- Bond swap, baskets

- Equity Swap, baskets

This enhancement will allow users to define business centers that are not in the current FpML list such as exchange business centers. This will enhance the flexibility of those instruments where they are permitted.

Subscription based licensing

TM Total Return Swap

Sales module dependency

TM Total Return Swap

Release 25.07 IBOR

![]()

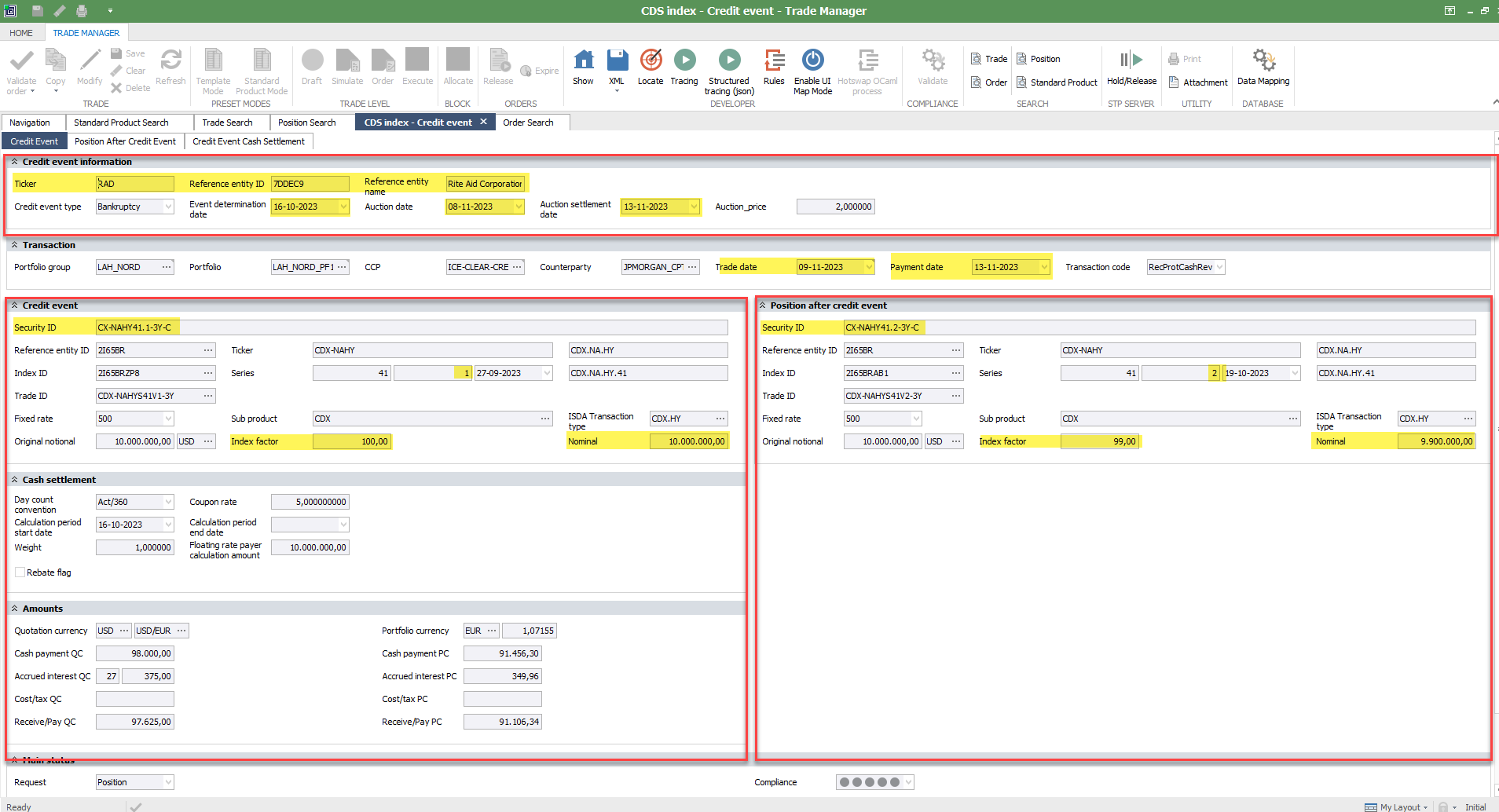

CDS Index - Support of hard credit events

A new Event type, Credit Event, has been introduced for CDS Index to improve the handling of hard credit events (e.g., bankruptcy, failure to pay). The new event type combines the settlement of the credit event with the re-versioning of the continuing CDS Index position to the new index version.

The new Event type is available for CDS Index:

- In the Trade Manager Position search for manual processing of credit events.

- As a new option in Create Credit Derivatives Transactions supporting an automated flow.

The new event type is a two-legged transaction where:

- The first leg contains information about the old version of the Index and the settlement of the Credit Event.

- The second leg contains information about the continuing position in the new index version.

A feature of the new event type is, that it supports different views on the re-versioning in front office and back office.

- In front office, the re-versioning will take place the day after the auction date, when trading in the new index version will start.

- The back office view will align with the Trade Information warehouse and the clearing house, keeping positions in the old version open until the auction settlement date, when the re-versioning takes place.

New Credit Event transaction type in the Trade Manager.

The new Credit Event transaction contains 3 tabs:

- Credit event tab showing an overview of the credit event, the position before and after the credit event, including settlement information.

- Position After Credit Event tab containing detailed information about the position continuing after the credit event.

- Credit Event Settlement tab containing detailed information about the position before the credit event and its settlement.

The overview tab (see above) is divided into 4 sections:

- First section contains information about the credit event, including defaulting entity, auction date, price, and auction settlement date. This information is generated based on Credit Event data and can’t be changed.

- Second section contains affected portfolio, other position identifiers, and main transaction data such as transaction type and trade and payment date.

- Third section contains information about the position before the Credit Event (based on standard product) and the settlement information of the Credit Event.

- The fourth section contains information about the continuing position in the new standard product representing the new index version and adjusted nominal.

On a credit event transaction, SimCorp Dimension calculates P/L values based on the notional portion of the CDS position corresponding to reference entities in the index version that have experienced a hard credit event.

Thus, in the P/L sub-window, on the out leg, you can view:

- P/L values calculated for the defaulted parts only.

- Cost value, book value, and up front-related balances relevant to the entire position.

Balances proportional to nominal outstanding are reallocated and booked to the new CDS index version position.

As a result of a credit event, positions in the old CDS index version are fully closed, and a position in the new CDS index version is opened.

Please note:

- A prerequisite for using the new Credit Event type is the use of CDS Index Standard Products. Standard product for the new version must be created in advance.

- The use of the new event type requires the use of the upfront approach for CDS Index Trades.

- You are recommended to use the Up-front in book value - advanced multiple trades swap payments setting option in the FAM window, even though SimCorp Dimension supports all applicable CDS Index Swap payment options in relation to CDS indices standard product accounting.

- UTI/USI will remain the same for the position in the new index version

Benefits

- Optimized credit event handling by combining settlement of the credit event and re-versioning of the continuing position into one new event type.

- Improved handling of positions seen in front office. Positions will be shown in the new version the day after the auction date.

- Improved handling of positions seen in back office. Positions will be shown in the old version until the auction settlement date (where the re-versioning also takes place in the DTTC trade Information warehouse and at the Clearing House).

- Improved accounting handling with transfer of values from the old to the new version.

Subscription based licensing

Credit-Credit Default Swaps and Swaptions

Sales module dependency

CDS Index as a standard product

CDS Index

Trade Manager

Enhanced notional reset handling and cash flow calculations for total return swaps in the Trade Manager

Nominal changes, notional resets, and cash flow calculations of total return swaps will be reflected more accurately in the Trade Manager

As of version 25.07, nominal changes, notional resets, and cash flow calculations of total return swaps will be reflected more accurately in the Trade Manager TRS instruments:

Instrument scope:

- Bond swap

- Bond swap, basket

- Equity swap

- Equity swap, basket

- Index swap

Note: This feature is not applicable to TRS basket contracts with adjustment transactions.

Key benefits

- Accurate cash flow information—Factoring in the new notional on existing reset transactions resolves previous discrepancies in the cash flow information of the funding leg for open and lifecycle transactions. Notional changes between resets, occurring due to any lifecycle transaction, are considered to ensure correct nominals on both performance and funding legs.

- Enhanced view of reset transactions—The Resets tab displays detailed information for both performance and funding legs, including notional changes and performance amounts. This offers a more integrated and transparent overview. A mouse-over tooltip on the Notional field in the grid highlights the impact of reset transactions affected by lifecycle transactions.

- Enhanced view of lifecycle transactions—You can also view the details of all lifecycle transactions associated with a TRS trade in the added Lifecycle Transactions tab under the Cash flow/Fixings tab in the Trade Manager. You can monitor the notional changes and performance amounts for lifecycle transactions created in the Trade Manager. This enhancement streamlines the TRS workflow by offering comprehensive insights into the trade.

Subscription based licensing

TM Total Return Swap

Sales module dependency

TM Total Return Swap

Removed limitation on number of business centers for total return swaps

The Trade Manager previously had a limitation of the number of business centres on a TRS instrument and this has now been removed

As of version 25.07, you can select any number of business centres for the following TRS instruments in the Trade Manager:

- Bond swap

- Bond swap, basket

- Equity swap

- Equity swap, basket

- Index swap

This feature is only applicable to payment dates, valuation dates, reset dates, and FX conventions for TRS instruments.

Benefits

- Users can enter any number of business centres in TRS instruments now.

Subscription based licensing

TM Total Return Swap

Sales module dependency

TM Total Return Swap

Added Expiry Time and Expiry Time zone to FX Options in Trade Manager

As of version 25.07, you can add settlement information for a new FX option trade in the Trade Manager. Two fields, Expiry time and Expiry time zone, have been added for the following FX option instruments in the Trade Manager:

- FX Option

- FX Option, Digital

- FX Option, Double Barrier

- FX Option, Single Barrier

- FX Option, Touch

- The Expiry time field contains the latest time (in hh:mm format) and the Expiry time zone field contains the applicable time zone when the option can be exercised.

- Both fields are optional and available for data import.

- Neither field can be modified during the lifecycle of the trade.

- To enter these details for an FX option trade in the Trade Manager:

- Go to the Trade Information section on the Trade Information tab of the contract.

Set the latest possible time to exercise the option as Expiry time and select the Expiry time zone to the applicable time zone.

Subscription based licensing

N/A

Sales module dependency

Trade Manager

Include US Pools as underlying for TM Straight repos

Nominal changes, notional resets and cash flow calculations of total return swaps will be reflected more accurately in the Trade Manager

As of version 25.07, nominal changes, notional resets, and cash flow calculations of total return swaps will be reflected more accurately in the Trade Manager TRS instruments:

Instrument scope:

- TM Repo (straight repo)

Key benefits

- Ability to select US Pool instrument as underlying instrument type.

- When selecting underlying Security ID only US Pool securities are selectable.

- Pool factors from the underlying US pool are taken into account, when calculating the settlement amount.

Subscription based licensing

TM Straight repo

Sales module dependency

TM Straight repo

Corporate Action Instruction Widget

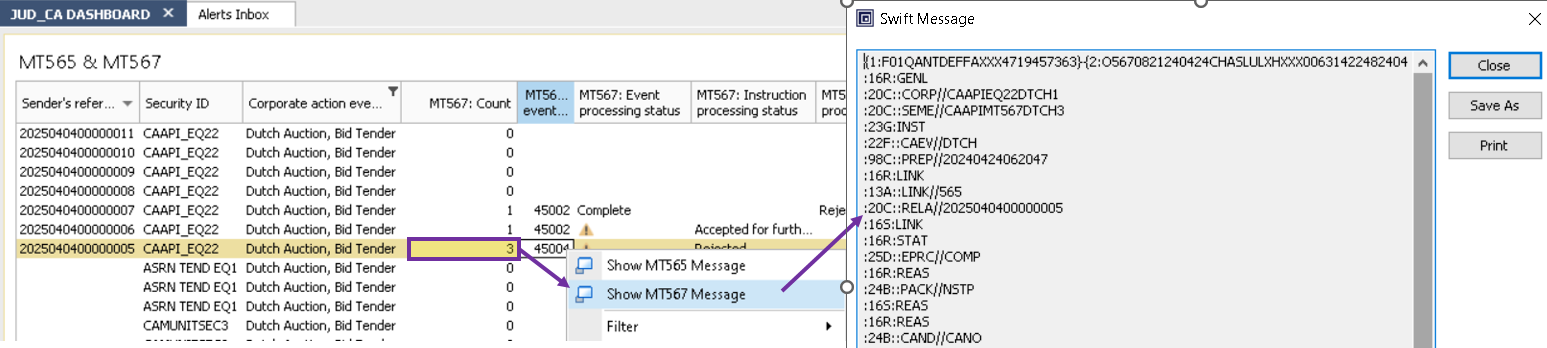

Automatic linkage and display of MT565/MT567 status and reason

The new Instructions Widget offers a significant enhancement to Corporate Actions processing capability. It is designed to provide greater transparency and efficiency by offering a consolidated, real-time view of MT567 status messages linked to each MT565 corporate action instruction.

This widget automatically links incoming MT567 messages to the corresponding MT565 event and displays the latest MT567 status code (e.g., PACK, PEND, CANC) along with the associated reason code. This enables users to immediately understand the current position of their instruction. Where multiple active MT567 messages exist for a single MT565, the widget shows the total count and displays the latest.

In addition, users can:

- View the full MT565 and MT567 message content directly from widget by right clicking on the widget item.

- See the full narrative text associated with the reason code, offering additional context for rejected or pending instructions.

- View the distinct status types (e.g., Instruction status, Processing status, Cancellation status) all in one place.

This enhancement allows users to work more efficiently, reducing the need to search across multiple windows.

Benefits

- Instantly view the latest status of MT565/MT567 messages without switching screens.

- Helps operations teams identify and resolve issues early, reducing downstream risk and ensuring timely, accurate processing.

- Minimizes the risk of settlement failures, missed entitlements, and instruction rejections or cancellations.

- Eliminates the need for manual reconciliation, freeing up valuable operational resources.

This image shows the MT567 Instruction Widget within the Corporate Action Dashboard, highlighting the status, reason, and narrative fields.

This image demonstrates the right-click functionality, revealing options to Show MT565 Message and Show MT567 Message for full message visibility.

Subscription based licensing

Equity - Securities

Sales module dependency

Equities

Ability to dynamically calculate tolerances during reconciliation based on rules

Tolerances in general reconciliation can now be specified in a more flexible way. Use predefined rules to dynamically determine and apply the appropriate tolerances based on the values of the internal reconciliation results. You can now, in a single reconciliation rule, specify different tolerances for various currencies, for example, 1 EUR for payments that settle in EUR and 10 YEN for payments in YEN. You can apply tolerances to all numeric reconciliation fields.

This setup also allows for entering a universal base tolerance in a base currency. Set a threshold for the reconciliation tolerances in a base currency, for example 1 USD, and get the threshold calculated automatically in different currencies, using the prespecified FX rates, and have those applied during reconciliation. The FX rates can be automatically updated via a batch job or manually as often as needed.

You can define the tolerance conditions in the Dynamic Tolerance Conditions window and use them in the Reconciliation rules.

Benefits

- More precision and consistency when reconciling.

- Define distinct tolerances per currency within a single rule .

- Manage tolerance logic with flexibility in one place (Dynamic Tolerance Conditions window).

Subscription based licensing

Reconciliation Manager

Sales module dependency

IBOR Manager

Release 25.04 IBOR

New batch job for updating OTC contract calendars

During the lifetime of an OTC contract, there may be changes to the definition of which days are non-banking days in the relevant business centers. A date that may have been a banking day when the contract was entered into, and so expected to have e.g. a swap payment, can turn out to be a non-banking day due to a new holiday.

With the new batch job ‘OTC Instruments– Validate All,’ such changes can be automatically detected and reflected on IRS and TRS contracts, correcting any days that are now non-banking days.

Benefits

- Automates the maintenance of banking days on IRS and TRS contracts.

Subscription based licensing

N/A

Sales module dependency

Trade Manager

Support for MXN OISs and MXN OIS swaptions with lunar calendars

As part of the industry-wide move away from LIBOR based benchmarks to alternative risk-free rates (“RFRs”) and following the announcements made by the Banco de México, as of 1 January 2025, new MXN swap contracts will be based on TIIE de Fondeo (an overnight rate), thereby replacing the existing 28-day Interbank Equilibrium Interest Rate in local currency (Tasa de Interés Interbancaria de Equilibrio, “28D-TIIE”).

This change will affect all MXN swaps with OIS legs. Therefore, Dimension now supports lunar calendars for the following Trade Manager swap instruments: IR swap, OIS, IR swap, OIS, basis, Cross currency, basis, Cross currency, fix/float, Non-deliverable IR swap, fix/float, Non-deliverable cross currency, fix/float.

These swap enhancements are available from 25.04 but have also been patched down to 24.10 and 25.01.

Secondly, from 25.04, Dimension now also supports handling lunar calendars for the Trade Manager instrument Swaption, IR swap, OI.S

Benefits

- The ability to handle MXN-based OTC contracts with lunar calendars

Subscription based licensing

N/A

Sales module dependency

Trade Manager

Support for NDS swaptions with physical delivery

Until 25.04, the existing Trade Manager instrument Swaption, Non-deliverable IR swap, fixed/float could only handle the settlement method Collateralized Cash Price”. The number of settlement methods has now increased, so Dimension now supports the following settlement methods: Physical, Cleared Physical, Cash Price and Collateralized Cash Price.

Secondly, we have also applied the Forward term to Swaption, Non-deliverable IR swap, fixed/float, allowing clients to handle forward-staring/mid-curve NDS swaptions.

Benefits

- Widen the scope and usability of the Trade Manager instrument Swaption, Non-deliverable IR swap, fixed/float.

Subscription based licensing

N/A

Sales module dependency

Trade Manager

Support for rounding on the Price QC field for Cross Currency TRS

We have added support to allow the ability to round the Price QC field on the Trade Manager to a defined decimal precision and rounding method.Additionally, this rounding on the Price QC field will continue throughout the lifecycle of the Total Return Swap.

Benefits

- Correctly support Cross Currency Total Return Swap rounding on the Price QC field for Index Swap, Bond Swap, and Equity Swap instruments.

Subscription based licensing

N/A

Sales module dependency

TM Total Return Swap

Support Forward Starting TRS with known Initial Price and Initial FX Rate

We have added support to allow users to define an Initial Price and an Initial FX Rate on a Forward Starting TRS. Previously, this was restricted and had to be created via valuation fixings/FX Fixings. Now, users can enter the initial price and/or initial FX Rate for a forward-starting TRS, and these will be picked up from Trade Manager in the initial exchange transaction.

Benefits

- Users can enter Price/FX Rate on a Forward Starting TRS from Trade Manager, and it will be used in the initial exchange without further action from the user.

Subscription based licensing

N/A

Sales module dependency

TM Total Return Swap

TRS – Portfolio Swap Agreement Tool

We have added support for a Portfolio Swap Agreement tool for Total Return Swaps. This allows users to define a Portfolio Swap Agreement in the newly created form in SCD. This reference can then be applied to multiple TRS trades using the portfolio swap agreement field in Trade Manager.

Benefits

- Users can link multiple Total Return Swaps in a synthetic wrapper within SCD.

Subscription based licensing

N/A

Sales module dependency

TM Total Return Swap

TRS – Increase lifecycle event available in Asset Manager Modify Position

We have added support for the Increase lifecycle event in the Modify Position functionality within Asset Manager. Previously, this was only available via Trade Manager.

Benefits

- Users can perform an Increase on a Total Return Swap using Asset Manager.

Subscription based licensing

N/A

Sales module dependency

TM Total Return Swap

TRS – Contract Simulation

Contract Simulations were not supported for Total Return Swap Baskets in Trade Manager and Asset Manager. This has now been added to enhance the overall functionality of the Equity Swap, Basket, and Bond Swap, Basket. We have also enhanced the single-name TRS contract simulation by adding the conventions tab, so that users can change defaults without accessing Trade Manager.

Benefits

- Users can perform a contract simulation for a Total Return Swap Basket in both Trade Manager and Asset Manager.

- Asset Manager users can now change default settings on TRS Single name without accessing Trade Manager.

Subscription based licensing

N/A

Sales module dependency

TM Total Return Swap

Release 25.01 IBOR

Price method “Quoted price and yield curve” can now use quoted price as input for FRAs

The price method quoted price + yield curve has been enhanced for FRAs to support changes in market quotations. Previously, FRAs were predominately quoted in yields, but more market vendors and clearing houses are now providing price information for FRAs in the form of of quoted prices.

With the quoted price + yield curves, it is now possible to use either a quoted yield or quoted price as input. As before, yield curve sensitivities are calculated regardless of the type of market quote used.

Benefits

- Supports the new type of market quoting for FRAs when using price method quoted price + yield curve to accommodate market standards.

- The same sensitivities are calculated, no matter which type of quote (yield or price) is used.

Subscription based licensing

Foundation

Sales module dependency

N/A

Audit trail for reconciliation execution actions and reconciliation results

Enhanced history log of manual changes

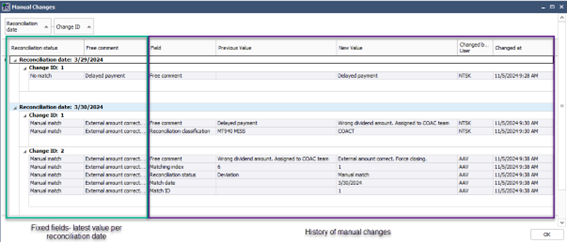

You can now access the full history of manual changes, even for results rolled over multiple days. In addition to displaying the manually changed fields, the new native fields Reconciliation Status and Free Comments provide an easy overview by displaying the latest value for each reconciliation day. All this is presented in a brand-new GUI, offering a more intuitive and user-friendly experience with customizable views, including filtering, grouping, or sorting.

Benefits

- Improved transparency to track and understand the evolution of the reconciliation results over time

- Better analysis and decision-making

New GUI showing details about the changes from this record inception date

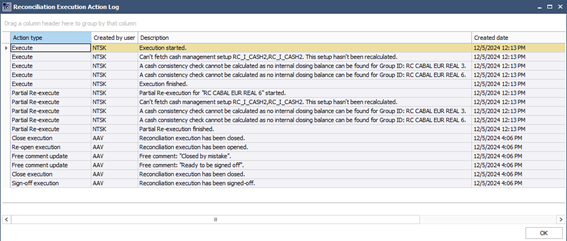

New audit trail for reconciliation execution actions

This version introduces an audit trail for actions performed at the reconciliation execution level. The log is accessible directly from the Reconciliation Manager.

For the following reconciliation actions, the log provides detailed information on when the action was started, any warnings or errors, when the action was completed, and by whom:

- Execute

- Partial re-execute

- Re-execute

- Internal import

- External import

- Apply auto-fill rules (only when applied manually or through a batch job)

- Re-open execution

- Close execution

- Sign-off execution

- Changes to the execution free comment (with the new comment visible in the Description)

Benefits

Improved transparency and accountability over the reconciliation process

Easier access to see errors or warnings that happen during execution or re-execution

Actions log for a reconciliation execution

Subscription based licensing

IBOR Manager

Sales module dependency

Reconciliation Manager

Ability to use a holiday calendar for calculating date deviations

Date deviation can now be calculated using business days instead of calendar days. The holiday calendar used for calculating break age can now also be used to calculate date deviations.

Benefits

- Date calculations are more accurate and aligned with your business operations

- Increased matching rates and reduced manual effort for resolving false deviations

Subscription based licensing

IBOR Manager

Sales module dependency

Reconciliation Manager

Ability to apply auto-fill rules manually

Rules created in the auto-fill rules application can now be triggered manually, directly from the Reconciliation Manager, for both active and inactive rules. This complements the existing options of applying rules during execution (for active rules) or via a batch job (both active and inactive rules).

Moreover, the engine has been enhanced to also allow deactivation/reactivation of the reconciliation records, based on predetermined rules.

To applied rules, these actions are logged in the new reconciliation execution log.

Benefits

- Users can apply rules on an ad-hoc basis with just a few clicks

- Reduce tedious manual work and the risk of errors by setting up rules for automatic filling

Deactivated checkmark can be turned on or off based on rules

Pressing Apply auto-fill rules and choosing one or multiple auto-fill rules to apply

Subscription based licensing

IBOR Manager

Sales module dependency

Reconciliation Manager

Automatically process CFDs on position adjustment MAND Corporate Actions.

With the increasing complexity of financial markets and the growing demand for derivatives processing, automation has become a necessity. This enhancement empowers our clients to seamlessly manage Contract for Differences (CFDs) processing for the following mandatory position adjustment corporate actions events:

- Bonus issue

- Stock splits

- Reverse stock splits / Consolidations

Benefits

- Enables users to assess how a portfolio of funds will respond to future changes in market conditions and identify factors that could jeopardize the investment strategy’s success.

- Enables users to produce more robust forecasts, as stress scenarios can reflect a wider variation of possible futures and situations that may not have occurred in the past.

- Allows users to flexibly combine several types of cashflow-related stresses, such as accelerating capital calls, delaying repayments, and extending fund lifetimes, define the groups of funds to which these combined stresses can be applied.

Subscription based licensing

Corporate Actions Manager

Sales module dependency

Corporate Actions Manager, Equities

OTC Web API

We have launched the OTC web API, which allows for programmatic access to the OTC functionality in SimCorp Dimension. Orders and transactions on OTC contracts can now be created, changed, deleted, and updated. The API is integrated with the Front Office API, so that it is now possible to combine OTC and non-OTC orders in automated flows.

Benefits

- Enables automation of OTC workflows that were traditionally handled manually within the Trade Manager

- Enables easier integration with Front Office processing

- Enables export of OTC contracts to external systems

Subscription based licensing

OTC Web API

Sales module dependency

N/A

Create inflation curves from index bonds

In many developed markets, forward-looking inflation curves are best created from inflation derivatives, primarily from zero coupon inflation swaps (ZCIS). In other markets, such as Mexico and Brazil, where there is no liquid ZCIS market, the best alternative is to use index bonds. The former has long been possible in SimCorp Dimension’s Yield Curve Manager, and the latter is now also supported.

The inflation curve creation is enabled for all built-in index variants but is most relevant in practice for Mexican and Brazilian variants.

With the new functionality, you can create accurate inflation curves also in economies without a liquid ZCIS market. The accurate inflation curves lead to more consistent pricing and improved risk management of inflation-linked instruments.

Benefits

- Generate accurate valuation and risk analytics for inflation-linked instruments in Mexico and Brazil

- Full auditable transparency in curve generation via the ubiquitous Explain calculation functionality

- Automate inflation curve generation with scheduled jobs shared across all curve types

Subscription based licensing

N/A

Sales module dependency

N/A

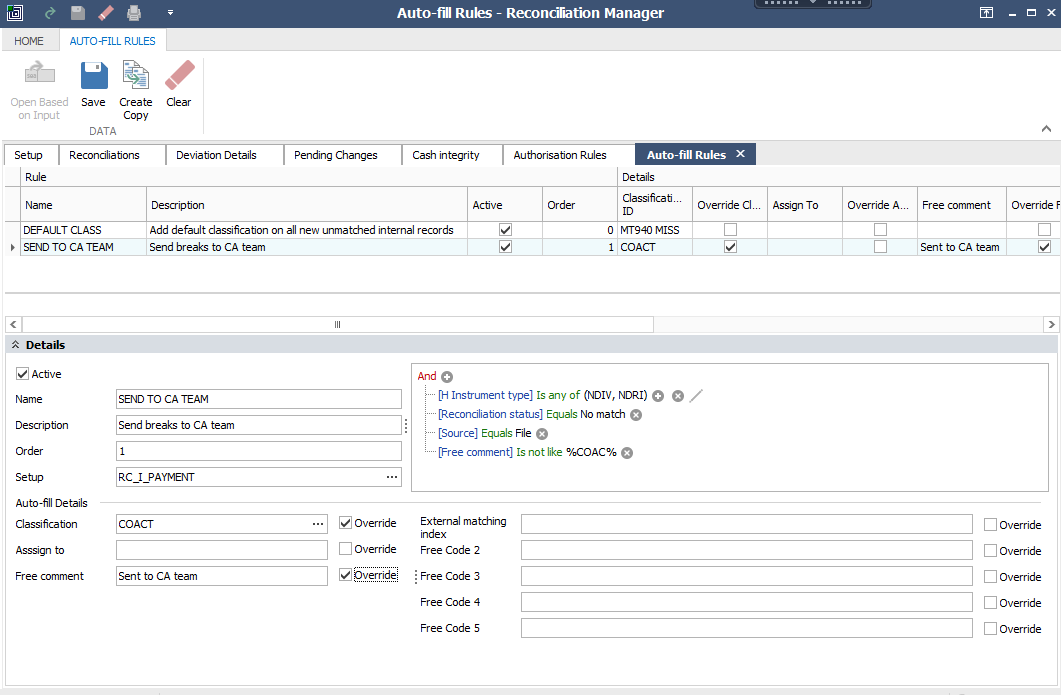

Auto-fill reconciliation fields based on predefined rules

Define rules based on the existing reconciliation results to automatically populate other reconciliation fields such as Classification, Free Comment, Reconciliation Free Codes, or Assign to fields. You can configure these rules in the new Auto-fill rules applet within the Reconciliation Manager. The rules will apply automatically during the reconciliation execution or can be executed ad hoc using a batch job.

Benefits

- Reduce tedious manual work and the risk of errors

- Streamline your reconciliation processes so you can focus on critical tasks

Multiple rules can be configured and executed in the specified order. In the image above, two rules will be applied during the execution: one rule adds a default classification to all new internal breaks, while the second rule sends external breaks on dividends to the COAC team by filling in the predefined classification value, COACT. This classification could also trigger an alert.

Subscription based licensing

IBOR Manager

Sales module dependency

Reconciliation Manager

More flexibility and a better control framework for one-side matching

You can now configure the one-side matching algorithm to apply exclusively to records from the external side, the internal side, or both sides. Previously, it would always apply to both sides.

Additionally, you can now set up authorization rules with the maximum possible granularity to control manual actions in the Reconciliation Manager and prevent human errors. Action types such as match, pay, force close, partial pay, etc., can now be combined with the type of record (internal or external) and the number of records (one-record or multiple).

These rules can now be highly customized depending on the specific action to be performed in the Reconciliation Manager.

Benefits

- Increased flexibility allows for better control over the matching process in the reconciliation application

- Enhanced security and risk of human errors by defining who can perform specific manual actions in the Reconciliation Manager and under which conditions

Define rules in the Authorization rules applet in Reconciliation Manager. The Total deviation field type has been enhanced to calculate the net amount for one-sided matching actions, while for both sides matching actions, it will check the difference between the amounts. Tolerances can also be set.

Subscription based licensing

IBOR Manager

Sales module dependency

Reconciliation Manager

Release 24.07 IBOR

![]()

Valuation of Mexican Inflation Linked Bonds

You can now use the full flow for Mexican inflation-linked bonds, known as MXN Udibonos. That includes the calculation of fair theoretical value and key ratios such as breakeven inflation rate, implied spread, money yield, real yield. This enhancement brings offers more precise and reliable valuations that align with the unique characteristics of the Mexican financial market.

In addition, you have the capability to build an Inflation Curve that predicts future MXN/UDI rates, leveraging market quotes from Mexican UDI/TIIE Swaps while considering peculiarities of the Mexican market.

Benefits

This enhancement offers support to investors in the Mexican capital market by enabling them to:

- Develop effective strategies to hedge against inflation.

- Evaluate risk exposures associated with Mexican Inflation bonds, utilizing metrics such as duration, convexity, and spread duration to assess interest rate risk, credit risk, and overall portfolio risk.

- Access the impact of various market scenarios on portfolio returns and risk measures.

- Analyse movements in the yield curve and their implications on portfolio positioning and strategy, including the Inflation Curve.

- Allocate and monitor performance of inflation-related attributions in FIPA flow.

Subscription based licensing

Inflation – Index Linked Bonds

Sales module dependency

N/A

Enrich/match reconciliation results using external sources

The new ‘Reconciliation results free codes 1’ to 5 fields enable you to enrich the reconciliation results with more information from the external file (using Data Forma Setup and only for external records), from other external sources (using dedicated APIs), or manually. Once the information is brought back into Reconciliation Manager, it can also be used to match records.

Note that in this version also Classifications can be inserted or updated from outside SimCorp Dimension via dedicated API endpoints.

Benefits

- Enrich reconciliation results and help solving breaks by leveraging external data sources

- Match records based on information enriched from outside SimCorp Dimension

- Manually insert and keep track of various information on breaks in text or date format

Subscription based licensing

IBOR Manager and Investment Operations API

Sales module dependency

Reconciliation Manager

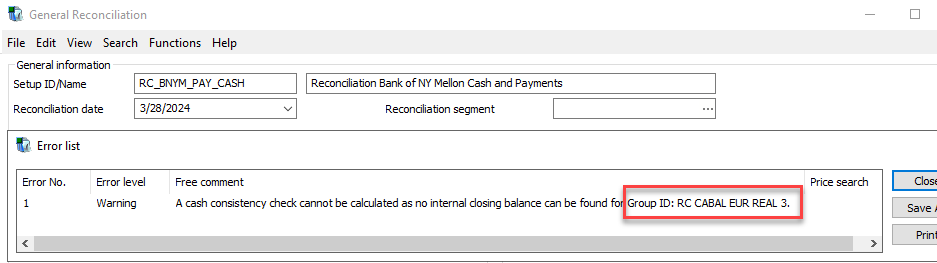

Enhancements to Cash Integrity check

The existing widget and form displaying the integrity check calculations will now include records for accounts where the calculation could not be executed due to various reasons, such as missing internal closing balance.

Benefits

- Gain a complete view of all accounts with their integrity checks, also when they fail

- Receive more informative warning messages when the integrity check cannot be calculated

Integrity check widget show records with warnings. Note the “Out of proof by” field which is empty in this case.

Existing warning message text shows information about the failed Group ID

Subscription based licensing

IBOR Managers

Sales module dependency

Reconciliation Manager

Trade Manager swaps with payment lags

The LIBOR reform was implemented by the end of 2021 for CHF, JPY, EUR and GBP LIBOR rates and by the end of June 2023 for USD LIBOR rates. The replacement rate was based on daily compounded O/N rates like SONIA, SOFR, ESTR etc.

For many OTC derivatives, like OIS swaps, a payment lag is applied to handle the calculation and confirmation of the compounded rate. For basis swaps the user may have to apply different payment lags of the two legs. This was only possible from 22.04 for the Trade Manager instrument “IR swap, OIS”. From 24.07, the user may also apply different payment lags for the following Trade Manager instruments:

- IR swap, OIS basis

- Cross currency swap, fixed/float

- Cross currency swap, basis

- Non-deliverable Cross currency swap, fixed/float

- Non-deliverable IR swap, fixed/float

- Asset swap

Benefits

- Enables users to correctly handle swaps in Trade Manager where the payment lag is different between the legs

- As an example, a EURIBOR vs ESTR basis swap may have a 0 day payment lag on the EURIBOR leg and a 2 day payment lag on the ESTR leg

Subscription based licensing

Trade Manager

Sales module dependency

Trade Manager

Trade Manager OIS manual payment date

The LIBOR reform was implemented by the end of 2021 for CHF, JPY, EUR and GBP LIBOR rates and by the end of June 2023 for USD LIBOR rates. The replacement rate was based on daily compounded O/N rates like SONIA, SOFR, ESTR etc.

In order to support the full flexibility required for the payment date structure the ability to enter manual payment dates is required. This functionality was previously introduced for Fixed and Floating interest rate types. This enhancement also the manual payment dates to be entered for all Trade Manager swap legs with a “Daily Fixings” Interest Rate Type. The instrument scope for this enhancement is:

- Asset swap

- Asset swap inflation

- Equity Swap

- Index Swap

- Bond Swap

- Bond swap, basket

- Equity swap, basket

- Cross-currency basis swap

- Cross-currency fixed/float

- IR swap, OIS

- IR swap, OIS basis

- Non-deliverable cross-currency fixed/float

- Non-deliverable IR swap fixed/float

Benefits

- Enables users to enter manual payment dates for OIS/Daily Fixings legs

Subscription based licensing

Trade Manager

Sales module dependency

Trade Manager

Trade Manager TRS Open the cash flow grid for manual Valuation dates (roll dates=Payment dates)

In a continuation of work to support irregular date structures for the TRS instrument in Trade Manager, from 24.07, users may now enter manual valuation dates on the following Trade Manager instruments when Roll Dates = ‘Payment Dates’

- Equity Swap

- Index Swap

- Bond Swap

- Bond swap, basket

- Equity swap, basket

Benefits

Enables users to enter manual valuation dates for Payment Dates rolls and enables more flexibility in the date structure.

Subscription based licensing

Trade Manager

Sales module dependency

Trade Manager

![]()

Enabled Collateral Optimization via Cassini Systems

This new module enables collateral optimization via third party Cassini Systems.

It enables users to send securities available for collateralization to Cassini Systems and receive optimized selection of assets to allocate thus ensuring the highest quality assets are available for the front office/treasure department for investment or financial purposes and increasing the profitability at a fund level.

Benefits

- Collateral Optimization via Cassini Systems is removing manual process that have been adopted from the front and middle office teams is choosing the lowest quality eligible asset to meet a collateral call.

Subscription based licensing

Collateral Manager

Sales module dependency

Margin Manager and Collateral Manager MarginSphere Adaptor

Release 24.04 IBOR

Ability to leverage the Counterparty SSIs from CTM ALERT database

New dedicated settlement fields on transactions make it possible now to capture the Counterparty’s settlement instructions from the ALERT database, on a trade-by-trade basis. The retrieval and updating of transactions can be done seamlessly during the trade confirmation process in Simcorp Dimension, or imported from external files. The new SSIs can then be used to generate Settlement instructions.

Moreover, it is possible to decide on Counterparty level whether they can be trusted with the SSIs from ALERT per instrument group, and use this decision actively when generating instructions.

Benefits

- Reduced risk of settlement failure due to wrong/outdated internal SSIs

- Reduced pressure on internal Counterparty SSIs maintenance

- Increased operational efficiency

Subscription based licensing

Settlement Manager

Sales module dependency

OMGEO Central Trade Manager - Adaptor

Overview of accounts and their Cash integrity

Cash and Payment reconciliation across multiple accounts pose a lot of complexities. One of them could be ensuring data accuracy and consistency. A new Integrity Check dashboard gives an aggregated view of all your accounts and their cash integrity, allowing for a more focused approach to solving breaks.

Benefits

- Unified view – all accounts and their integrity checks in one place

- Ability to prioritize solving breaks for accounts with integrity anomalies

- Ability to view the cash integrity calculations over several executions

- Ability to drill down to the reconciliation records associated with the account directly from the dashboard.

Subscription based licensing

Reconciliations Manager

Sales module dependency

Reconciliations Manager

Integration with YieldBook

YieldBook is a best of breed financial analytics platform that specialises on valuation of complex instruments including mortgage-backed securities (MBS) and asset-backed securities (ABS).

With the new interface, you can now seamlessly integrate SimCorp Dimension with YieldBook.

This enhancement utilizes the security-protected External Calculation framework and a new External Calculation Result Mapping window, enabling the retrieval of any MBS-specific key ratios. The streamlined process can connect to the YieldBook web API or XML API, unlocking enhanced capabilities for valuing a wider range of structured financial instruments within SimCorp Dimension, namely:

- ABS

- US MBS Pool

- TBA

- CMO

Benefits

This integration significantly improves efficiency and accuracy in valuing complex instruments such as ABSs, US MBS Pools, TBAs, and CMOs. Access to both end-of-day and intra-day analytics on demand eliminates delays and enhances decision-making agility in Front Office applications in an audit proof operation with mitigated operational efforts and risk.

Future Enhancements

The initial release focuses on retrieval of key ratios for MBSs across the SimCorp Dimension, with the potential future iterations concentrating on deeper integration:

- Introduction of Flexible Pricing Configuration.

- Activation of Key Rate Durations.

- Provision of User Defined Market Data.

- Integration of Scenario Analysis within the Risks Module.

- Support for YieldBook Dials.

- Retrieval of Cash Flow Information for ABS/CMOs.

Subscription based licensing

Yield Book/Basic

Sales module dependency

Various; Foundation plus "External Calculations" - Basic

Enable theoretical valuation of Australian Capital Indexed Bonds

You can now use the full flow for Australian Capital Indexed Bonds, including the calculation of fair theoretical value and key ratios such as breakeven inflation rate, implied spread, money yield, real yield.

In addition, you have the capability to build an Inflation Curve that predicts future Australian Consumer Price Indices, leveraging market quotes from Australian Zero-Coupon Inflation Swaps while considering peculiarities of the Australian market.

Benefits

This enhancement offers support to investors in the Australian capital market by enabling them to:

- Develop effective strategies to hedge against inflation.

- Evaluate risk exposures associated with Australian Capital Indexed Bonds utilizing metrics such as duration, convexity, and spread duration to assess interest rate risk, credit risk, and overall portfolio risk.

- Access the impact of various market scenarios on portfolio returns and risk measures.

- Analyse movements in the yield curve and their implications on portfolio positioning and strategy, including the Inflation Curve.

- Allocate and monitor performance of inflation-related attributions in FIPA flow.

Subscription based licensing

Various; Foundation

Sales module dependency

Various; Foundation

TM TRS Basket/Basic

You can now manage total return swap (TRS) baskets in the Trade Manager, including setting up Equity swap, basket and Bond swap basket, creating basket adjustments, handling payments and resets, and creating novation step-out or close transactions. This enhancement simplifies the process of exchanging the total returns of a basket of assets for periodic cash flows in the Trade Manager.

Key features:

- Capture TRS Baskets: You can now capture TRS baskets with either equities or bonds as the underlying assets in the Trade Manager. TRS basket in the Trade Manager includes the following instruments:

Benefits

- Enables clients to use Trade Manager to manage and create Bond Swap baskets and Equity Swap baskets

- Enables clients to create and save baskets in a one step process.

Subscription based licensing

TM TRS

Sales module dependency

TM TRS Basket/Basic

LIBOR Reform: support rounding rules on Trade Manager swaps

SimCorp Dimension now supports rounding rules that can be applied to the compounded rate used in Accrued Interest calculation on all Trade Manager swaps where one or both legs are linked to Overnight reference free rates, in this way the system will comply with the market standard dictated by the LIBOR reform.

Benefits

- Allows users to apply rounding rules on Trade Manager OIS legs and comply with the market standard;

- Enables calculation of rounded Accrued interest amounts upon entering a swap contract, or upon closing a swap contract or in the analytics applications in SimCorp Dimension.

Subscription based licensing

LIBOR Reform package

Sales module dependency

TM Overnight Index Swaps

TM TRS: support IBoxx

SimCorp Dimension now supports front-to-back solution for Standardized Total Return Swaps (TRS) on iBOXX bond indices. The IBOXX TRS trading conventions are embedded in the existing instrument type Index Swap in the Trade Manager so that the standard contract conventions are triggered under a particular configuration. As for any total return swap, a user can capture the IBOXX TRS trade in the Trade Manager, book total return swap resets payments, increase/unwind the position and mature the contract. Accrued Amount at the time of entering into a new trade or closing out a trade, as well as Performance amounts on TRS resets are calculated based on the IBOXX Standardized TRS Trading Convention Guide from the IHS Markit website.

Benefits

- Enables users to trade and manage a highly liquid standardized total return swap contract based on iBoxx bond indices;

- Allows users to simplify the trade capture and apply Iboxx standard conventions as defaults on the existing Index swap instrument upon a particular configuration.

Subscription based licensing

TM TRS

Sales module dependency

TM Index Swaps

LIBOR Reform: support rounding rules on TM swaps

SimCorp Dimension now supports rounding rules that can be applied to the compounded rate used in Accrued Interest calculation on all Trade Manager swaps where one or both legs are linked to Overnight reference free rates, in this way the system will comply with the market standard dictated by the LIBOR reform.

Benefits

- Allows users to apply rounding rules on TM OIS legs and comply with the market standard;

- Enables calculation of rounded Accrued interest amounts upon entering a swap contract, or upon closing a swap contract or in the analytics applications in SimCorp Dimension.

Subscription based licensing

LIBOR Reform package

Sales module dependency

TM Overnight Index Swaps

Consolidation of instrument modules

The following instruments will be removed, with adoption of the long standing Global Standard Solutions required for these models from release 24.10.

Benefits